Powell delivers the message: Inflation is the top priority

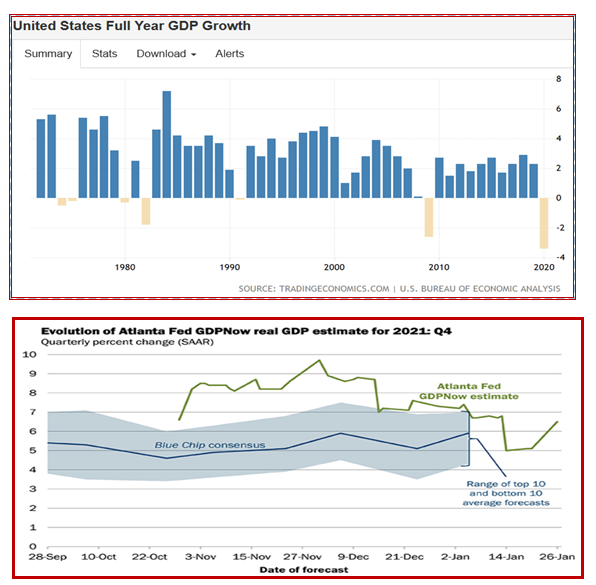

Outlook: Today we get the usual weekly unemployment report, probably a decline by 26,000 to a seasonally adjusted 260,000 for the latest week, according to a Reuters survey. Of more interest is the next Q4 GDP estimate, a wide range of 2.5% to 6.5% and even 7.5% (JP Morgan), according to Reuters, although forecasts were made before the giant inventory jump yesterday. The Atlanta Fed has 6.5% for Q4, from 5.1% in Jan 19, for the same reason. Golly, if inventories were so robust, imagine what they might have been without supply chain disruptions.

For the year 2021, GDP was probably 5.6%. This is the most in 25 years and in fact the most in 50 years, surpassed only by 1984. The Fed is on solid ground when it says robust growth allows for “flexibility” in policy. Without going too far into the weeds, the next issue is liquidity and whether marginal players can get any.

One of the most interesting things about what Powell says in the press conference is the wide variation in what people hear. We heard no decision on the first hike at the March meeting although the members “are of a mind” to do it. We heard supply chain problems not improving as expected and taking longer, meaning inflation will be higher and for longer. We heard balance sheet contraction will come after the first hike, and it’s complicated as to what, when and how much. Powell said the members need to discuss it at the next couple of meetings, meaning no action likely until after May.

All of this is disappointing to hawks and points to a roll-over instead of a sharp pivot from wildly accommodative to less accommodative/full-bore tightening. One analyst called it the wimpiest statement ever. We wouldn’t go that far but we like the Fed and even we thought the wording was weak.

But note that word “wording.” Powell was sedate and restrained, classy even, as a central bank gov should be. But don’t be fooled, like the disappointed hawks. Powell delivered the message–inflation is the top priority. The emphasis on inflation is a shift from an emphasis on the labor market. Powell all but throws labor under the bus to stress the Fed cares about inflation now. And while the balance sheet rearrangement may be deferred to May, we are sure to start seeing rearrangement starting almost immediately; it’s likely Powell wanted to defer focus on that because the liquidity watchers are already out in full force and as we have seen before, they are real trouble-makers.

To some extent, whether the message was sharply hawkish or only a little so depends on which asset class you are tracking. FX traders voted with their feet and returned to the dollar, bigtime, from the most traded currency (euro) to EM’s (yuan). Bond guys were mostly impressed, hence the rise in yields all along the curve (so much fun to watch on Bloomberg TV as Powell was speaking), but not to any lastingly wild levels, like 2% in the 10-year, and falling back already today. It’s the equity guys crying in their beer because the Fed has definitely taken away the punchbowl. The so-called “Fed put” whereby the Fed is intimidated by a tanking stock market is a fiction.

As noted above, remember those tables over the past few days showing rate hikes not correlated with stock market pullbacks? Ned Davis is cited by Bloomberg today: “Higher rates haven’t always snuffed out bull markets. The S&P 500 rose an average 5.3% in the 12 months following the first increase in 17 tightenings since 1946, according to a Ned Davis Research study on market returns and monetary policy. The pace of tightening, however, makes a stark difference: The equity benchmark fell 2.7% on average during faster rate hikes while rising 11% during slow ones.”

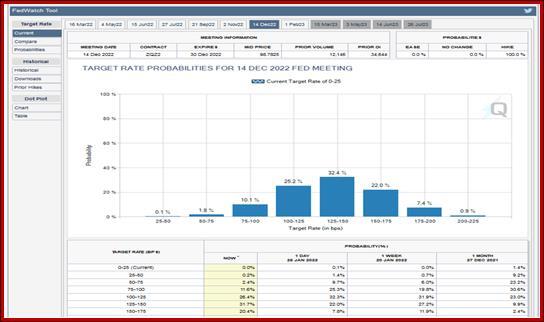

The stock market is buying the “faster hikes” story. If we believe the CME FedWatch tool, 32.4% now see six hikes by year-end, but to that you have to add the ones that see a lesser number (e.g., 24.8% that see four or five, so all together, a majority now see more hikes than ever before. Only 9.7% see the three hikes that was the starting point back in December when the Fed announced the policy shift and upsized inflation from transitory to something that has to be attacked lest it become persistent.

To deflate this somewhat, remember that Fed funds futures are not a reliable indicator of actual future Fed funds rates. The CME FedWatch tool is fun because it discloses sentiment, not because it’s accurate. And secondly, there is still a chance–granted, a diminishing one–that inflation fades a bit by (say) June or September. The number of hikes–the fast hike scenario–can be cut back. Powell did emphasize flexibility and that can cut both ways. We would be astonished if we got more than three hikes. Six or more is just ridiculous. We like to consult history for guidance on the present and near future, and the Fed has never raised rates six times in nine months.

Now to digest the GDP information and watch the yield curves. If the 10-year yield keeps rising and inflation starts falling, the real rate will be improving. That has to be dollar-positive.

Tidbit: The NYT had a cogently argued story about Russia and Europe’s gas problem. If the US and Nato countries apply sanctions, Putin’s retaliatory weapon is cutting off gas supplies to Europe (about one-third of total imports). That would risk offending Russia’s best customer in a failed-state economy, aka a two-edged knife.

Some of the problems is of Europe’s own making–they failed to store enough. Then Europe got lucky–the weather was not too cold. Finally, alternatively sourced supplies are arriving–from the US and the Middle East. The NYT reports “a single tanker can hold the equivalent of three times the current daily transit volumes from Russia through Ukraine. The surge has been significant: In January, flows of liquefied natural gas to Europe have actually exceeded those of Russian gas.” But a drawback: “Whether liquefied natural gas shipments could offset a complete shut-off of Russian gas to Europe is doubtful. Liquefied natural gas tankers require special terminals, and Europe probably does not have enough receiving terminals to match such enormous losses.”

Longer run, Russia becoming an unreliable energy supplier encourages renewables. Yeah, like the energy crisis in the US in the 1970’s did the same thing? The US became energy independent some 50 year later and not from going green, but rather from producing more itself, at high environmental cost.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat