Pound set for weekly gain as FTSE slides

It’s been a fairly solid week for the pound on the whole with the currency appreciating against most of its peers despite a raft of worse than expected data from the UK. The sharpest move came on Monday when traders rushed to buy sterling after Nigel Farage announced that his Brexit party wouldn’t be contesting Tory seats from the last election. Even though the Brexit party have since refused to cede more ground and still plan to contest marginal Tory/Labour seats, it is clear that the market in the near-term currently favours developments that increase the prospect of a Conservative majority.

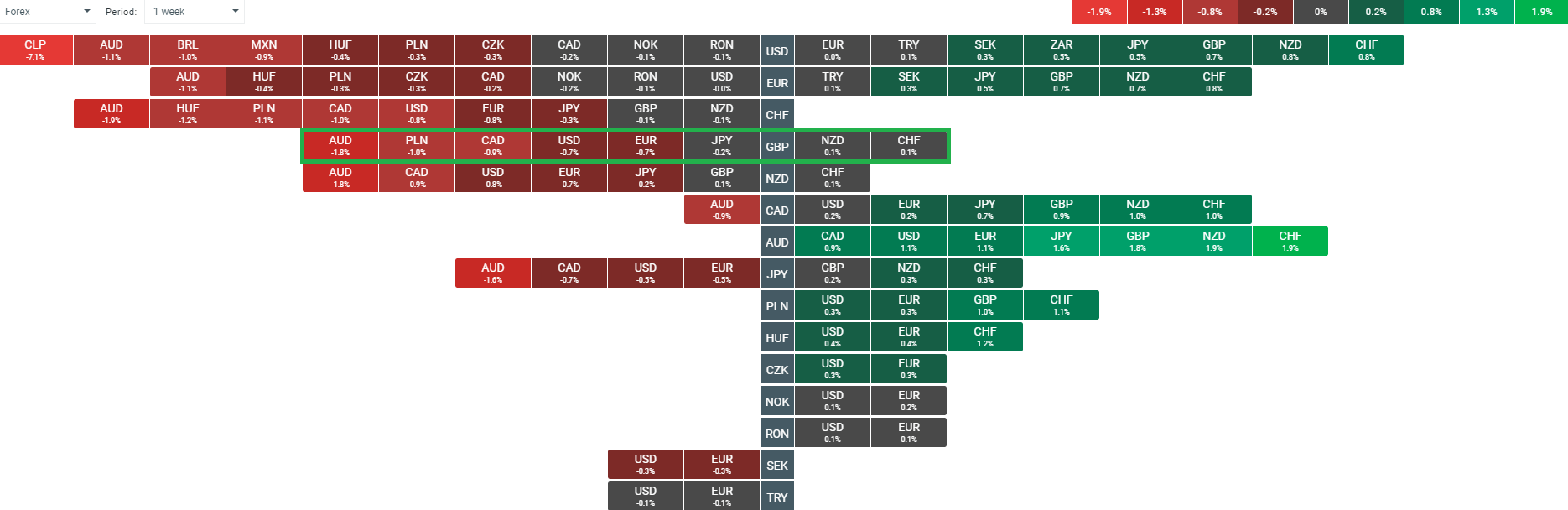

The pound is gaining on balance for the week with the largest gains seen against the Australian dollar with a weak employment report from down under and political tensions in China weighing on the Aussie.

Source: xStation

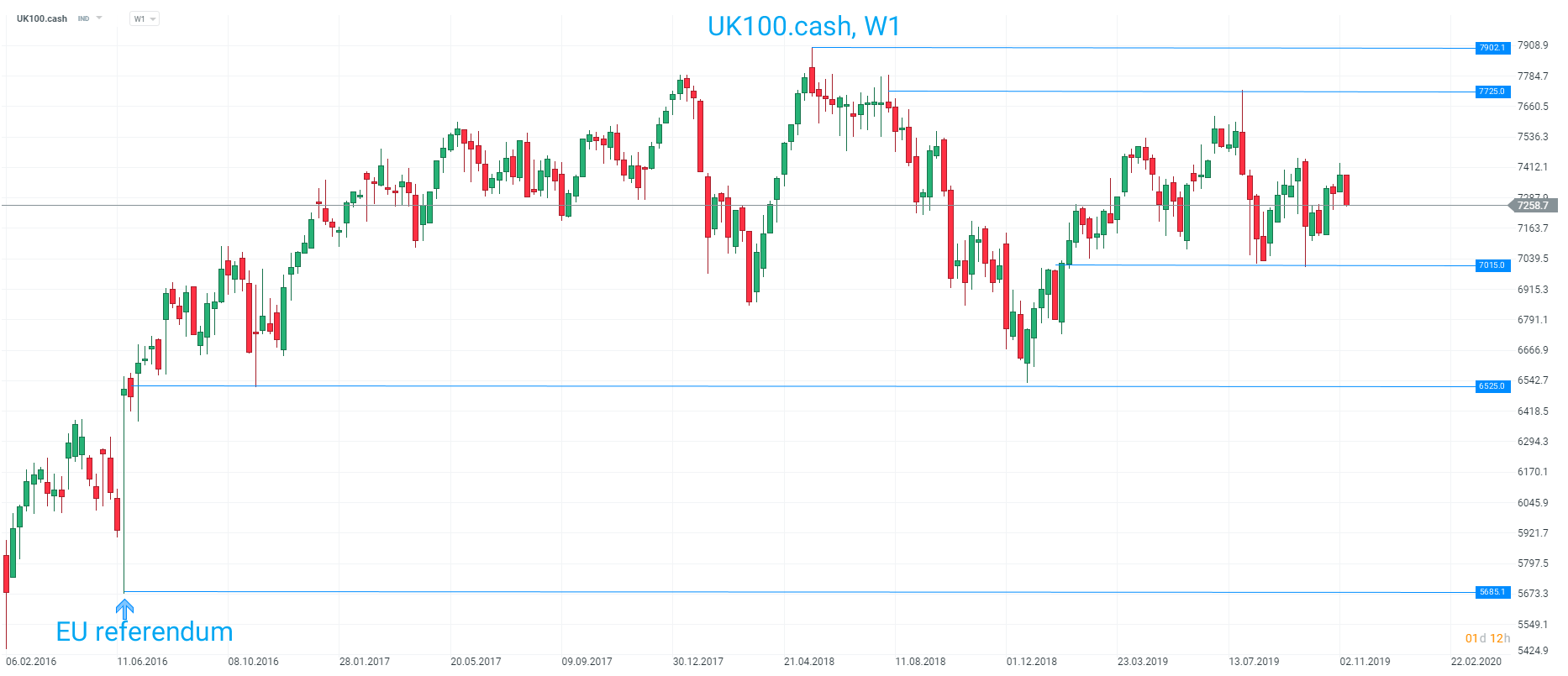

FTSE fades after recent gains

Those who hoped this would be the week that UK blue-chips would start to catch-up with stock markets gains on the continent and across the pond look set to be disappointed once more with the FTSE 100 failing to build on recent gains and on track for a weekly decline. After starting the week not too far from its highest level in over 3 months, the index has fallen back and is on track to finish this afternoon not too far from its weekly lows. The benchmark’s sensitivity to China has been a clear headwind as stocks in the far east have experienced some sizable declines after more civil unrest in Hong Kong. Local stock markets ended the week down by around 5% and this has weighed on shares in London with the miners hit with some selling and Antofagasta receiving a double whammy with the troubles in Chile also causing a headache for investors.

UK shares have been largely rangbound for the past 3 ½ years since the EU referendum. The range has been even more narrow in recent months with the market confined to a roughly 10% range since the start of February 2019.

Source: xStation

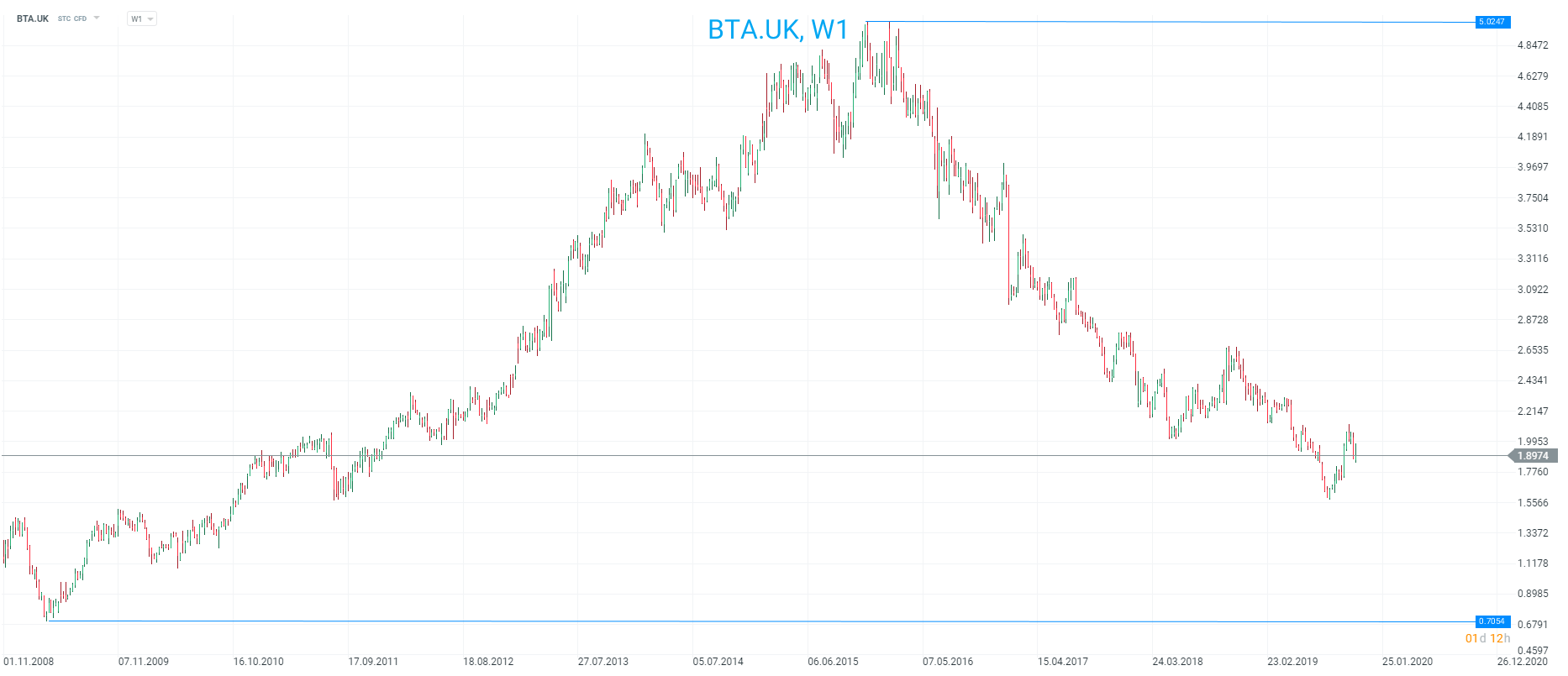

BT recovers after early dip

There was a fairly sharp move lower in shares of BT on the Friday open, with the stock tumbling over 4% after news that a Labour government would nationalise the firm’s Openreach network. This represents a step further from Labour in their plans for renationalisation, with leader Jeremy Corbyn already promising to take several utilities such as water, the railways and the National Grid back into public hands. After a soft start there’s been a strong bounce in BT shares with the stock recouping nearly all the losses to trade back nearly Thursday’s closing level before drifting lower again. This could be a reflection of investors’ views that Labour is unlikely to deliver on its pledge, or simply that the prospect of us ever finding out what a Labour government would do is seemingly still remote enough to not warrant too much concern amongst BT shareholders.

BT shares have been in a downtrend for nearly 4 years now after peaking just above the £5 mark around the turn of the year from 2015/16. The stock has lost over 60% of its value in that time.

Source: xStation

Author

David Cheetham

XTB UK