One worry beyond the cost of goods is the cost of labor

Outlook: The US calendar is tight for potentially market-moving news. First up is the US inflation update, forecast at 3.6% y/y from 2.6% y/y in March and with plenty of detail to chew on. Right afterward, Fed Vice Chair Clarida will address the National Association for Business Economics and will not be able to avoid questions about inflation. So far he and the other Feds are sticking to the script—inflation will be higher but not by a lot and will be transitory. Then at 1 pm, the Treasury offers $41 billion in 10-years. Recall that in Feb we got the taper tantrum on a 7-year auction, but that came out of the blue. This time we have the inflation report in close proximity.

Both the WSJ and Bloomberg have a forecast for CPI of 3.6% y/y, which will be the highest 12-month level since mid-2011. On the m/m basis, though, it’s only 0.2%. Now consider the base effect. In April last year, prices fell 0.7%, and over last summer, the monthlies were around 0.5%, so the seemingly high y/y will fade in the next month and stay down all summer. Another idea is to annualize the monthly, a really bad idea that any novice statistician would frown on, but this is stockbroker economics, so go with it. The outcome, according to some arithmetic we don’t understand, is 4.5%. It may remove the base effect but is still a bad and indubitably inaccurate number.

All the same, we are getting inflation. The WSJ notes a survey by something named the National Federation of Independent Business shows “36% of small businesses indicated that they had raised selling prices in April, the highest share since 1981.” Still, the WSJ’s own economist panel expects the inflation bump to be temporary—a rise to 3% in June but falling to 2.6% by December. This is pretty much what TreasSec Yellen said.

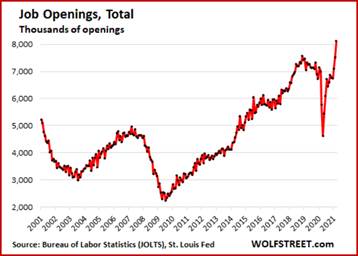

One worry beyond the cost of goods is the cost of labor, which is running at a decent pace and reflects the tight labor market and shortage of skilled workers. Job recoveries are still 8 million short, but 16.2 million are getting unemployment benefits. In other words, the potential exists to get full recovery in jobs to the pre-pandemic level but it’s not clear the job can get done (due to skills, immobility, etc.). A key number in the Jolts reported is job openings in the better-paying manufacturing sector spiking by a record 134,00 jobs over the month before to a record 706,000.

Wolf Street says “Compare the job openings to the number of people currently working in manufacturing – the jobs that manufacturers could actually fill — which dipped in April to 12.2 million people, according to the BLS jobs report. Compared to February 2020, the last month of the Good Times, this was down by 515,000 workers. And yet there are 706,000 unfilled jobs, which, if they were all filled, would push manufacturing employment to highs not seen since 2008.”

Trading Economics reports that “job openings rose by 597 thousand from the previous month to 8.123 million in March 2021, the highest level since the series began in December 2000 and well above market expectations of 7.5 million. Jobs were created in a number of industries led by accommodation and food services (+185,000); state and local government education (+155,000); and arts, entertainment, and recreation (+81,000). Meanwhile, the number of job openings decreased in health care and social assistance (-218,000). The number of job openings increased in the Northeast and Midwest regions. Meanwhile, the number of hires rose by 215 thousand to 6.009 million, while total separations including quits, layoffs and discharges, and other separations dropped by 107 thousand to 5.322 million.”

So, inflation fear today depends on a fair amount on how seriously the markets take the Jolts report from yesterday. Jolts would have us believe that not only recovery to pre-pandemic levels is possible before Christmas, we could also have net gains. This is what the Fed is prioritizing and if achieved, loosens up the forecast from 2024 for the first-rate hike to a far earlier timeframe. If wages are on the rise at the same time, to improve the match between labor supply and demand, then the Fed would have another incentive. The problem, of course, is that tight labor markets are due in part to a workforce that in big on illiteracy and low education, drug addiction, bad work habits, immobility, and a slew of other problems that have plagued the tight labor market for several years. And don’t forget that Europe, the UK, and Asian countries do not have such a sloppy workforce.

Tidbit direct from Bloomberg: “The U.S. Securities and Exchange Commission warned investors in mutual funds that hold Bitcoin futures to beware of the risks in the “highly speculative” asset. A Bitcoin ETF seems to be as far away as ever after recent comments from SEC Chair Gary Gensler seemed to pour cold water on the idea. There is, however, no shortage of speculation in the space, with the amazing performance of the crypto called “Internet Computer” a case in point. The token was launched on Monday and was worth $45 billion by Tuesday.”

We don’t like it. We don’t understand it except as a case of tulip-mania. We don’t want any part of it! But sure, we might take a tiny position in an ETF if run by somebody respectable. Goldman, maybe.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat