November payrolls boost Fed’s economic case for the December 11 FOMC

- Non-farm payrolls soar 307,000 including revisions to September and October.

- Yields, equities and the dollar move higher on the unexpectedly strong report.

- Economic performance supports Fed neutral rate policy.

November’s stellar employment report highlights the record US labor market and makes the Federal Reserve’s final meeting of the year next week likely to be an extension of its positive economic views from October.

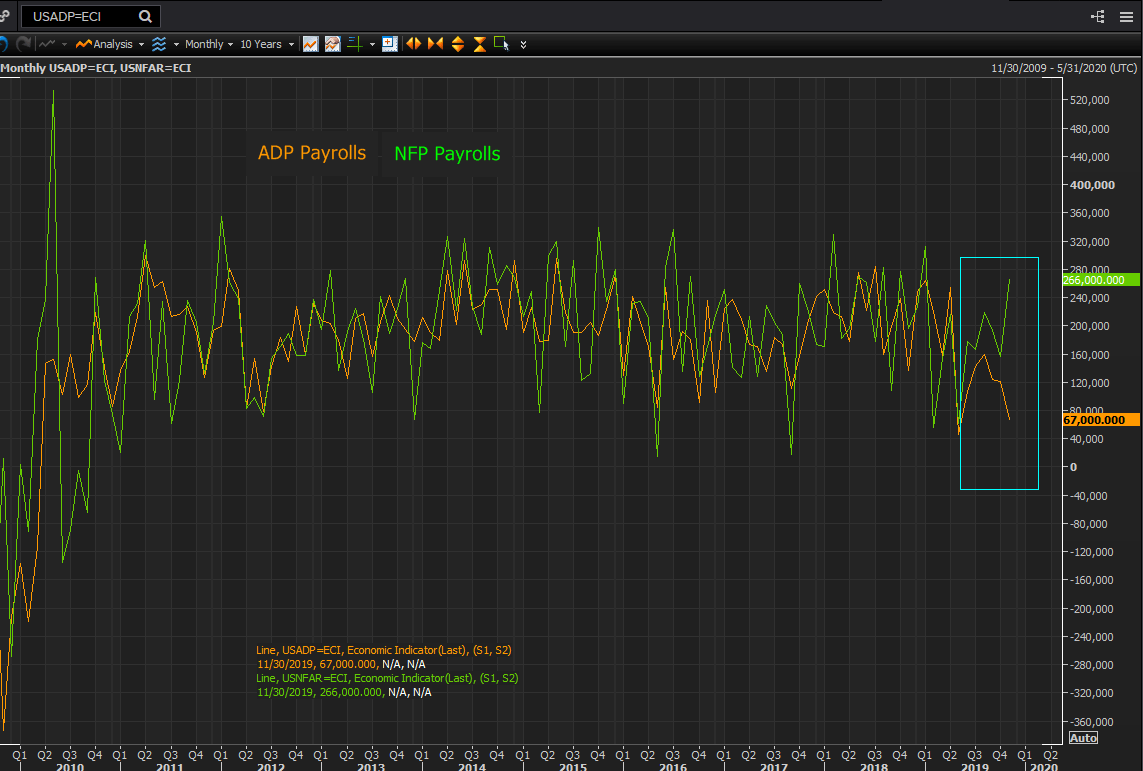

American firms added 266,000 new positions in November far ahead of the 180,000 forecast and revisions to the September and October totals tacked on another 41,000. It was the highest single month since last December’s 311,000.

Non-Farm Payrolls

The unemployment rate dropped 0.1% to 3.5% equal to the 50 year low. Annual wages rose 3.1% in November and a revised 3.2% in October, bringing the string of 3% and higher gains to 16 months.

Job growth has improved in the second half of the year. Payrolls have averaged 205,000 over the last three month and while that is down from 245,000 in January and 223,000 in 2018 it is 18% better than the 174,000 average in the first quarter, 35% higher than the second quarter average of 152,000, and a 6% improvement on the third quarter’s 193,000.

The November performance also ended the concern that the ADP private payroll total of 67,000 was an indicator for the nationwide NFP number.

In the last three months the two series have gone in sharply different directions, an unusual divergence for statistics that are a part and the whole of the national job picture. The ADP three month moving average has gone from 136,000 in August to 104,000 in November and the NFP average has moved from 187,000 in August to 205,000 this month.

The central bank called a halt to its rate reductions after enacting its third 0.25% cut at the October 30th meeting citing the improved global outlook and the resilient US economy. Third quarter growth was revised from 1.9% to 2.1% by the Bureau of Economic Analysis in its second release and the Atlanta Fed increased its GDPNow program estimate for the fourth quarter to 2.0% after Friday’s payroll numbers from 1.5% on December 6th.

Excellent job growth and unemployment will enter into the Fed’s own economic projections scheduled to be released next Wednesday December 11th with the rate decision. The September estimates envisioned 2.2% growth this year and 2.0% in 2020. Incorporating the GDPNow Q4 estimate of 2.0% GDP has expanded at a 2.3% this year. In September’s Projection Materials the fed funds rate was predicted to be 1.9% through the end of 2020. The target range is now 1.5% to 1.75%.

A strike at automaker General Motors during last month’s survey period cut about 40,000 strikers from the October payrolls with 41,300 positions added in November as they returned to work. Manufacturing overall gained 54,000 workers.

Equities stormed higher on the report with the Dow gaining 337.27 point, 1.22% to 28015.056 and the S&P 500 adding 0.91%, 28.48 points to 31545.91. The dollar rose against all the majors but benefited the least versus the British pound which has risen 7.7% against the dollar over the last three weeks boosted by projections that the Conservatives and Prime Minister Boris Johnson will win an outright majority in Commons in the December 12th national election.

Bond yields curbed their initial gains with the 2-year Treasury adding 2 points to 1.61% and the 10-year rising 3 point to 1.84%.

In addition to the Fed meeting on Wednesday markets will focus on the US-China trade talks which are running into the Sunday December 15th deadline when President Trump has said he will impose tariffs on the reaming uncharged Chinese imports mostly consumer goods if no deal has been reached.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.