New inflation methodology, same-ish result

We want to flag a few methodology changes that are being made to the Fed’s preferred measure of inflation, the PCE price index. The changes will be rolled out in the BEA’s annual update on September 30 and will impact data from 2021 onward.

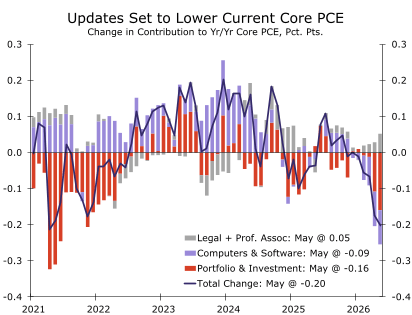

As the chart below shows, we expect the changes will shave only about 0.2 percentage points off the current y/y run-rate of core PCE. So the impact on actual inflation looks to be modest, but the changes are welcome just the same.

Despite the softer spot reading, note that these changes will not consistently deliver lower inflation. Said differently, we have no reason to believe these changes will generate a structural downward bias to inflation. In some periods, such as early 2024, this new methodology would have had core inflation running 0.1-0.2 pct. pts. hotter than the currently reported data. So while these changes are likely to put current inflation a little closer to the Fed’s target, that’s not likely to always be the case.

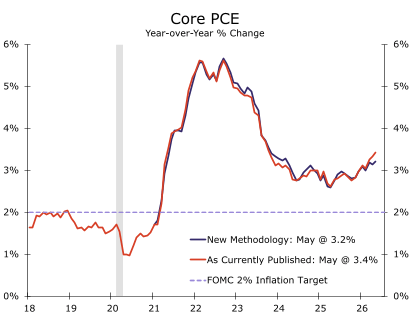

And while a two-tenths reduction is large in the scope of the typical size of revisions, it is small in the context of the Fed’s current inflation troubles. As our next chart shows, the new measurements won’t change the fact that inflation is still roughly a full percentage point above target.

Now what exactly is changing? Below are highlights from each component but for those that want even more detail feel free to ping us.

- Portfolio management & investment advice services: Currently, the BEA uses the PPI of the same name as the source data for this component of the PCE price index. Under the new methodology, the BEA will deflate nominal spending by extracting the quantity of services consumed using aggregate hours worked in the industry, with the difference in the rate of nominal spending and hours of services consumed yielding the “price” change.

Using this new approach, inflation in this component has still been hot over the past year (13% by our estimates) but it is not quite as steamy as the 22% rise currently reported by the PCE price index. - Computer software & accessories: The BEA will expand the source data currently used to deflate this series. The new BEA composite index will still include the CPI for computer software & accessories but will also now incorporate the PPI for game software publishing and the PPI for hosting, active service pages & other IT infrastructure provisioning.

Price increases for both PPI series have trailed that of the current CPI source data over the past 12 months, so their addition will lower current inflation for this category. While details on the composite weightings are not available, a simple average of the three series would cut the May yr/yr rate of the PCE for computer software & accessories by roughly half (from 14.5% to 6.8%). - Legal services: The BEA is swapping its source data from the CPI to a composite index of select PPI legal series consumed by households. This change will also apply to the PCE for professional association dues.

Although details on the composition of the new index have not been offered, the overall PPI for legal series points to less volatility from the legal services component going forward. But the PPI for legal services has also been running faster than the PCE measure over the past year and will thus generate a modest boost to current inflation.

As a final note, the methodology changes are likely to make mapping monthly PCE estimates after the CPI and PPI are published slightly more difficult since the weightings of the new BEA composite indexes won’t be published and the “price” index for portfolio management & investment advice will no longer be observable from the monthly PPI report. That could lead to a few more surprises on PCE day, but with these components comprising <4% of the index, we doubt there will be many times when such surprises materially alter the inflation picture.

Author

Wells Fargo Research Team

Wells Fargo