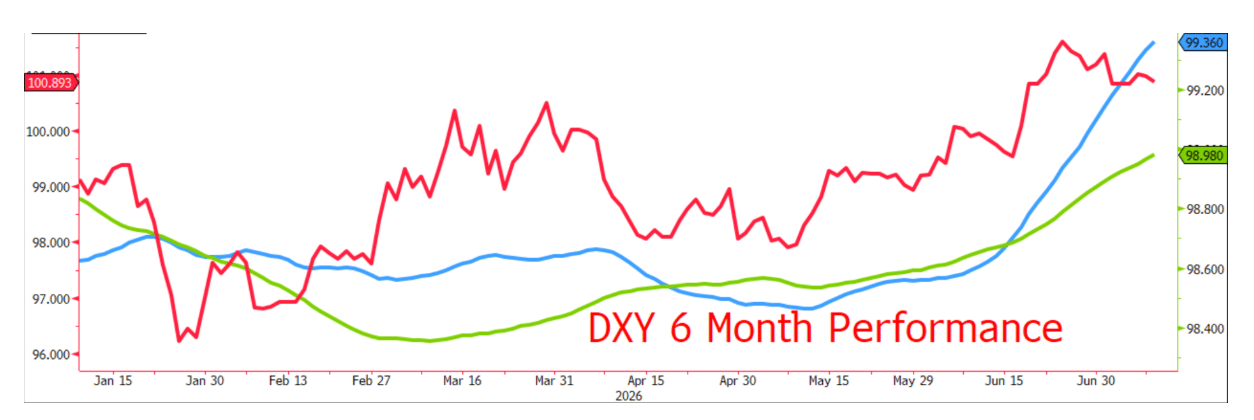

FOMC minutes dent DXY rally

Yesterday’s release of the meeting minutes for the June 17th FOMC were not what Dollar bulls will have been hoping for. Despite the firmly hawkish tone taken by Warsh in the press conference on the day, the assumption that the majority of his peers felt the same, that it was a close call as to whether to hike or hold, has proven false.

The minutes record that “few” FOMC members supported a hike in June but that the majority, whilst recognising the case for an early response to the intensifying energy inflation, did not see the immediate need to hike. The removal of the easing bias from the statement was made much of, although was very predictable considering CPI had risen to 4.2% in its last reading. Not removing that bias would have risked total confusion in messaging, with the market caught between a hawkish-sounding Chairman and a statement stressing the need for upcoming cuts.

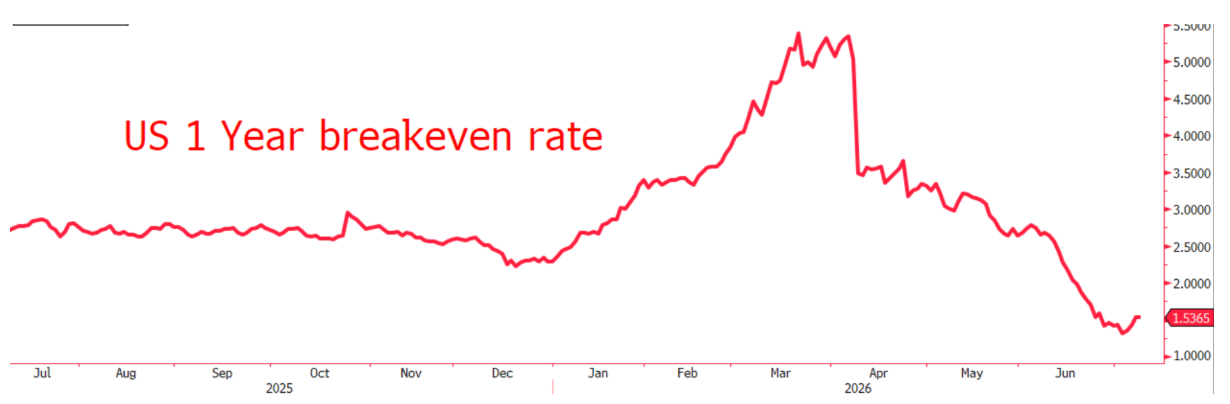

Moreover, the situation has moved quickly since June 15th; the above chart of the US 1-year breakeven rate shows investors' inflation expectations spiking in March before sliding below even pre-conflict levels. Surveyed US consumer inflation expectations from the NY Fed are up from 3.0% in February to 3.67% now, although given actual CPI is already higher than these expectations, it's not so alarming a situation yet.

I mention both breakeven and expectations as the FOMC highlighted the danger of keeping rates stationary whilst expectations ran away, threatening that the Fed could find itself behind the curve by the time they act. Gasoline prices have a disproportionately large impact on consumers' inflation expectations because of the visible and frequently purchased nature of the commodity. The last expectations survey taken at the start of June was when the average price for a US gallon of Gas was at $5.00, now $4.45, which is likely to have a constraining, perhaps even contractionary, impact on future CPI expectations.

Technicals suggest that the DXY could still sustain this rally, with the 100- and 200-day MA’s still firmly bullish, although fundamentals are starting to fail. A slightly soft NFP last week and now the revelation that the FOMC remains resistant to hikes, a feeling likely only reinforced by recent movements in data, are at least starting to sap the rally of life, if not reverse it. Perhaps a resumption of conflict in the Gulf could be the new motivation for a higher DXY, although given the sluggish movement in Oil over the past two days, this seems unlikely.

Author

David Stritch

Caxton

Working as an FX Analyst at London-based payments provider Caxton since 2022, David has deftly guided clients through the immediate post-Liz Truss volatility, the 2020 and 2024 US elections and innumerable other crises and events.