Bye, forward guidance: How to trade when central banks choose silence

Central banks have spent years telling markets what might come next. Now, traders face the possibility that they say a lot less. From the Federal Reserve to the European Central Bank and the Bank of England, policymakers are pushing back against forward guidance, arguing that the current world demands more flexibility. For traders, this shift is important because less guidance means greater dependence on data and, very likely, more market volatility.

For over two decades, global central banks have been using forward-looking guidance on the monetary policy outlook as a tool to support households and businesses in making decisions regarding spending and investments, respectively. And markets took this guidance as a useful tool too when deciding where to invest.

The significance of forward guidance from central banks remained vital in 2004, when inflationary pressures were accelerating globally due to increased capital expenditure on infrastructure, and in 2008 and 2020, when the subprime crisis and the pandemic, respectively, hit the global economy badly.

Forward guidance from central banks has also worked favorably in easing uncertainty regarding bond yields. However, the tool that has helped households to manage their spending and businesses to organize their investment plans is now becoming a bone in the throat for some central bankers.

Policymakers say no to forward-looking monetary policy guidance

Recent remarks from various central banks have signaled that officials are no longer interested in providing cues regarding forward monetary policy decisions.

In the rapidly changing geopolitical environment, forward guidance is constraining central bank officials from adjusting monetary policy decisions. Commitments by policymakers are limiting their flexibility to adapt and change their decision when needed.

Federal Reserve’s (Fed) first monetary policy meeting under new Chair Kevin Warsh ended with the message that market participants should stop expecting forward guidance from the central bank.

In the monetary policy press conference, Kevin Warsh said that policymakers agreed that forward guidance is “not well suited to the current policy conjuncture” and announced the formation of five task forces about Fed communications, the Fed’s balance sheet, use and reliance on existing data sources, productivity and jobs in an era of transformation, and last, the Fed’s inflation framework. All these are central to the broad conduct of monetary policy.

The sudden shift in how the new chief at the US central bank understands communication to markets has found some unexpected support in Europe. The latest remarks from European Central Bank (ECB) President Christine Lagarde at the ECB Forum in Sintra have also signaled that she doesn’t like delivering remarks on the interest rate outlook. “Forward guidance is not in the cards,” Lagarde said, adding, “If I have one regret is that I was bound by forward guidance in the past.”

ECB officials have also stated in the monetary policy statement that interest rate decisions will be made on a meeting-by-meeting basis and will be data-dependent. Officials have also touted several times that there will be no preset rate path in their considerations. Still, at least until now, there was almost always a media leak that would guide markets about what would be done in the following meeting.

Over the weekend, European Central Bank (ECB) Governing Council member and Bank of France Governor Emmanuel Moulin also refrained from providing cues regarding the central bank’s decision in July: “We are not doing forward guidance so I won’t say what we will do.”

BoE Governor Andrew Bailey also jumped on the bandwagon, noting that forward guidance becomes “quite problematic” as it is "much easier to put in place than it is to take it away".

Of course, every policymaker decides how vocal they want to be, but it looks like central bankers are leaning more towards silence.

All eyes on economic data

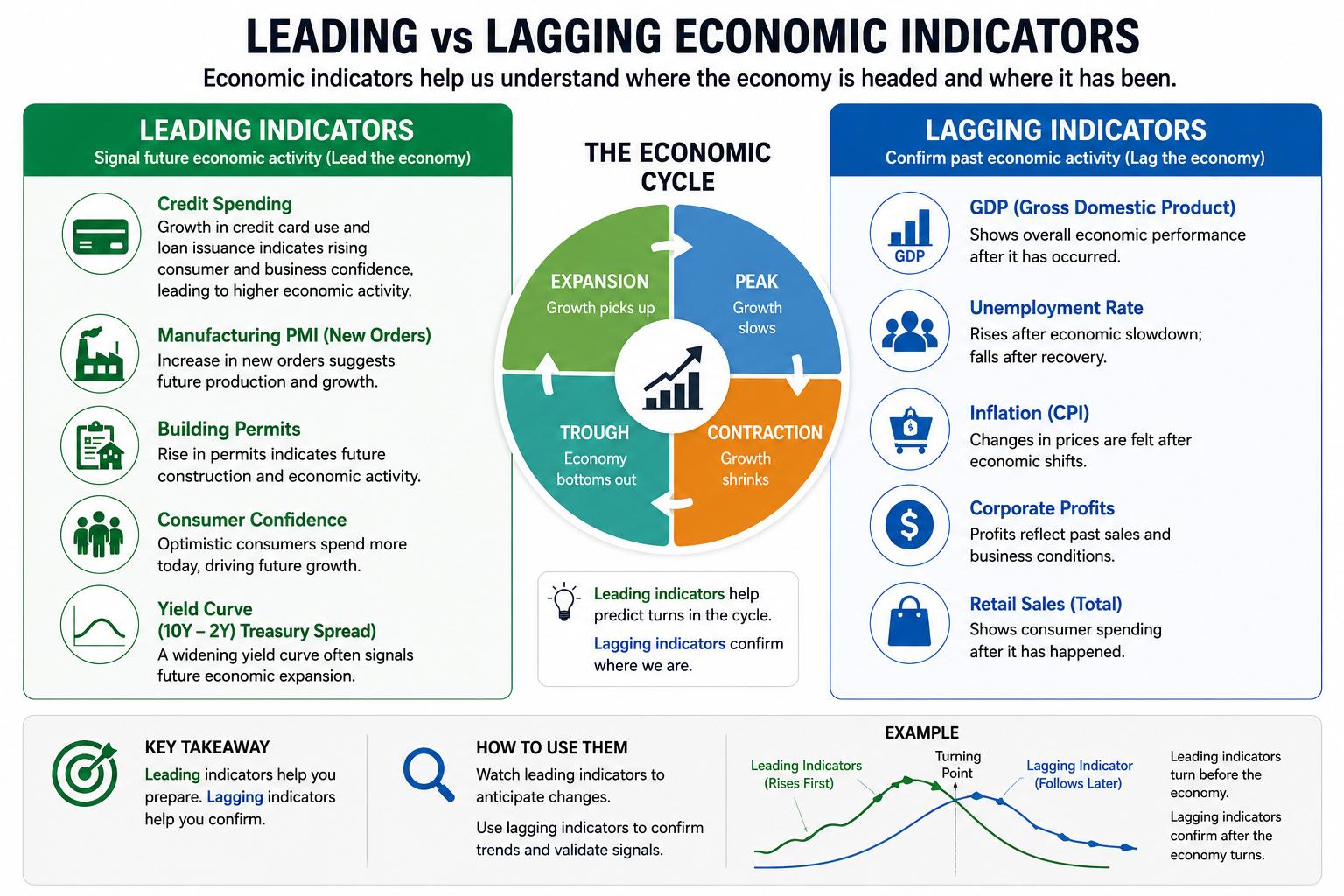

In the absence of forward guidance from central banks on monetary policy, the weight of economic data in guiding financial market participants on interest rate decisions increases.

Not only will the impact of lagging economic indicators such as employment and inflation on interest rate expectations be more significant, but the influence of leading indicators such as wage growth, credit card spending, yield curve, fresh business orders, and households’ expectations will also increase.

Starting with wage growth, the data can help investors understand the likely increase in individuals’ purchasing power. Higher purchasing power often leads to higher inflationary pressures. Similarly, credit card spending reflects overall demand among individuals and businesses, which significantly influences price pressures.

The spread between long-term and short-term interest rates indicates investors' expectations for future monetary policy decisions, inflation, and economic growth. An inverted yield curve indicates that short-term yields are higher than long-term yields, which can point to an economic downturn in the near future, increasing the likelihood of lower interest rates. On the contrary, a normal yield curve reflects an economic expansion, which calls for tighter monetary conditions.

New orders in both manufacturing and the service industry indicate the demand ahead and thus can be a bellwether for employment and growth.

Investors should pay close attention to these economic data to spot shifts in labor demand, households’ spending and productivity.

This also indicates that investors should be prepared for more volatile action by currencies on their regional economic data releases. Markets may no longer get a clear roadmap from central banks, but they will still get clues. Traders will need to pay more attention to find them.

Author

Sagar Dua

FXStreet

Sagar Dua is associated with the financial markets from his college days. Along with pursuing post-graduation in Commerce in 2014, he started his markets training with chart analysis.