Markets – Political risks become noticeable

-

Eurozone – Industry sentiment expected to remain around its currently high levels

-

US - Rate hike in March remains unlikely

-

Markets – Political risks become noticeable

Eurozone – Industry sentiment should remain strong in February

Next week (February 21), the first flash estimate for February's industry PMI data will be released for the Eurozone, Germany and France. In January, industry sentiment climbed, against all expectations, to a 51/2- year high of 55.2 index points. Geographically, sentiment in January was encouraging in all important countries, with Austria exhibiting the highest reading among Eurozone countries, with 57.3 index points. Sentiment benefited from higher volumes of total new business and new export orders (3-year high). The surveyed companies attributed the growth to both the recent depreciation of the euro and to signs of improving global market demand.

In light of the very high index level in January, we expect a slight depreciation of Eurozone industry sentiment in February. However, industrial production in the Eurozone should continue growing in 1Q17. Due to the freezing temperatures across Europe in January, the main contribution to growth should stem from energy production in 1Q17. In general, this confirms our current very positive assessment of the Eurozone economy; we expect slight acceleration of growth of +1.8 to +1.9% y/y in 1Q17.

Yellen and macro data increase yields and dollar only temporary, political risks gain in importance

The center of the market's attention was Fed Chair Yellen's statement in front of committees of the US House of Representatives and the US Senate this week. Through her statements, Yellen triggered immediate yield increases. From our perspective, the testimonies did not contain any significant changes and merely confirmed the current course of slow rate hikes, as was signaled at the last FOMC meetings. 'At our upcoming meetings the Committee will evaluate whether employment and inflation are continuing to evolve with these expectations (labor market strengthening and inflation moving up to 2%), in which case a further adjustment of the federal funds rate would likely be appropriate,' said Yellen. In our view, this wording indicates no accelerated course of action on the part of the FOMC. The FOMC remains on course for its forecast of three interest rate hikes this year and it is hardly a surprise to expect the first rate hike before mid-year, which is what Yellen signaled.

We consider an interest rate hike in March as unlikely and assume April or June to be more probable. The data published this week (consumer prices, retail sales) did not change our view either. They admittedly increased the risks for a rate hike in March, but should not be sufficient to convince the FOMC of the immediate need of a rate hike.

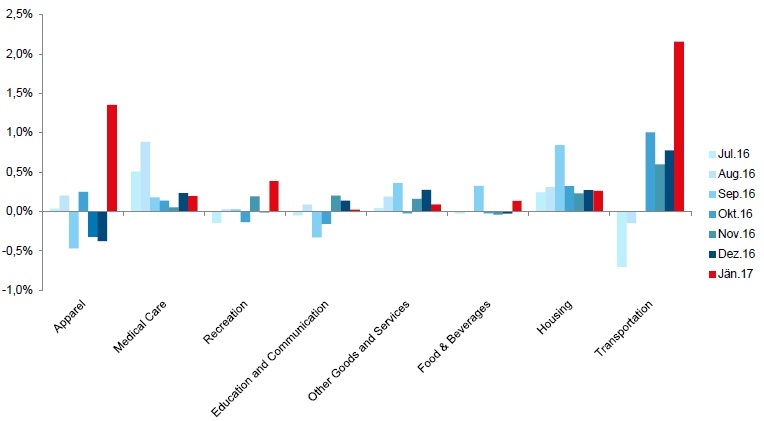

The reported rise of consumer prices for January was 2.5%, slightly above market expectations of 2.4%. Core inflation rose to 2.3%; the market expectation was at 2.1%. While it was foreseeable that increased oil prices would lead to an acceleration of inflation, the rise of core inflation was a surprise. However, the reported data did not contain any indication of a general acceleration of inflation. The acceleration in prices in January was not widely spread, but stemmed from only two product categories. Prices for Apparel skyrocketed in January and prices for recreational activities (Recreation) accelerated to a lesser extent. The other categories showed continuing trends. It is unknown why apparel prices rose that sharply. However, it appears evident to us that this will not change the FOMC's inflation forecast significantly and consequently will not lead to an accelerated course of action.

Consumer Price Increases, m/m in %

Retail sales also surpassed expectations in January and displayed an acceleration of consumer demand. Not only did the January data indicate a good start to 2017, but rather the revised data for December improved the outcome for the last quarter of 2016. By levelling the data and looking at the yearly growth rates, an acceleration over the last several months becomes apparent. However, this starts from relatively low levels and therefore only returned growth rates to the levels of the first half of 2015. From our view, these are not growth rates that would put any pressure on the Fed to take immediate action.

Our assessment of the recent data does not change the fact that we see the risks for rising inflation due to the tightening labor market and growing wages in the US and generally view the FOMC's current monetary stance as too loose. However, the crucial point is that the recently issued data should not be sufficient to change the Fed's current stance. We consequently maintain our expectation of three rate hikes this year. The risks are tilted to the upside, but have not materialized so far.

The impact of these events on markets was not lasting, at least for bond and currency markets. Towards the end of the week, yields declined again and returned to levels seen before Yellen's first speech, while the dollar was even significantly weaker. We attribute this development to increasing political risks. President Trump not only lost his national security advisor and nominee for labor secretary this week, but in America's Congress, calls for an investigation into the ties of the new administration to Russia are intensifying - also from the Republican side.

Such an investigation would likely bring the ability of the new administration regarding any political measures (tax cuts) to a standstill. But the outlook for tax cuts was decisive for the markets' reaction to the election of Trump. Should the uncertainty over their realization increase, bond markets could profit at least temporarily, while the dollar would suffer.

Author

Erste Bank Research Team

Erste Bank

At Erste Group we greatly value transparency. Our Investor Relations team strives to provide comprehensive information with frequent updates to ensure that the details on these pages are always current.