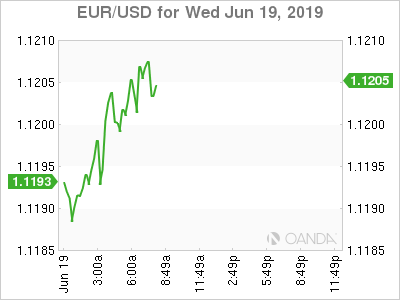

Markets Await Fed; dollar slightly softer on light volumes

The Fed’s current policy has lost effectiveness and at the end of what will be the longest US economic cycle in history, the FOMC is expected to announce the beginning of an easing cycle. US equity futures are hovering from a stone’s throw from fresh record high as the Fed concludes their two-day policy meeting. Bond yields are adjusting to expectations of fresh stimulus from all the major central banks. Germany sold 2046 bunds with a record low yield, following the Belgian auction who saw record lows with their auction on Monday. The low interest rate environment is likely to remain in place as the Fed begins an easing cycle and the ECB appears set to resume cutting interest rates. The dollar trades slightly softer ahead of the Fed decision.

Technology shares will come to focus today after the Nikkei reported that Apple is asking suppliers to consider moving 15-30% of its output from China to Southeast Asia. China is a critical hub for Apple’s business and some manufacturers have already pushed back. If we see US-China trade talks fall off a cliff, Apple suppliers, such as Hon Hai Precision Industry have contingency plans that could deliver iPhone production outside of China. In the event of an extended trade war, the main victim will be the consumer who will see higher costs.

Fed

The Federal Reserve will conclude its two-day policy meeting with economists expecting a confirmation of an easing bias in the second half of the year. Fed fund futures see a 22.9% chance that rates will be cut at today’s meeting, while the July 31st meeting have an 81.5% expectation for a rate cut. With inflation anchored below their target and the Fed’s first regional survey, Empire Manufacturing saw the worst decline on record, the FOMC should feel ready to embrace going full dove. Broad weakness has started to hit the US economy from trade uncertainty and that should still persist even if Trump and Xi deliver a de-escalation in tariff threats at the G20 summit at the end of the month. The Fed could try to hold out one more month before committing to rate cuts and note that the policy stance is appropriate right now. The dollar could rally if the Fed reiterates their patient stance, but the more likely scenario is for Powell to begin to adopt a dovish stance. How dovish of statement and how many rate cuts are shown in the dot plots will likely determine how far the dollar could fall.

Trump

President Trump officially launched his re-election bid on Tuesday at a rally in Orlando, Florida. Trump stuck to his favorite talking points which ranged from the strength of the economy, to Hillary Clinton, immigration, and Robert Mueller. Despite an overall strong economy that is at the tail of end or record long economic cycle, Trump is behind in most polls including one from Fox News over the weekend. With a potential 10-point deficit to Joe Biden and 9-point gap with Bernie Sanders, Trump appears set on keeping to the 2016 script that worked well for him during the last election.

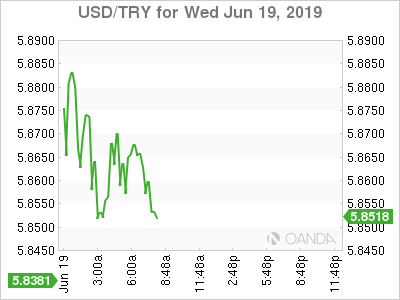

Lira

The US is weighing fresh sanctions on Turkey over the purchase of S-400 missile-defense systems from Russia. Severing Turkish companies from the US financial system would add further strain to an already weak Turkish economy. Trump and Erdogan will likely speak at the G20 summit, and the US administration will likely decide in early July if they should move forward with the sanctions. The lira fell 0.5% to the dollar after falling over 1.5%.

Author

Ed Moya

MarketPulse

With more than 20 years’ trading experience, Ed Moya is a market analyst with OANDA, producing up-to-the-minute fundamental analysis of geo-political events and monetary policies in the US, Europe, the Middle East and North Africa.