Markets are awfully slow to recognize a serious problem

Outlook: Today we get the usual weekly jobless claims. April existing home sales, the Philly Fed, and for the policy wonks, the ECB policy meeting minutes from the April meeting.

The elephant in the room is the S&P down over 4% in the worst rout since June 2020, just when everyone got the message the Covid pandemic was a Big Deal and worthy of the panic that had started a few months before. Ironically, in 2020 the Q1 GDP was down 9.1% and Q2, not yet released when the S&P tanked that time, was a whole lot less bad at -2.9%.

The implication is that markets are awfully slow to recognize a serious problem, but that flies in the face of the old attribution of the S&P being a leading indicator of economic health. We say the hysteria yesterday was unwarranted and that will be seen when facts get unspooled. The problem with hysterical panic is that it spreads like wildfire and disregards offsetting information. This is the classic behavior of crowds.

Reuters has a headline “Which earnings to the rescue?” but then the story goes nowhere and doesn’t name anything. So how does a bear market get halted? One silly idea is that some market leaders with deep pockets start acknowledging that the carnage created some buying opportunities. How does this differ from bottom-fishing? The holding period is longer and return-motivated, not knee-jerk opportunistic short-term gain, but we can know that only after some time.

All this is supposedly caused by a sudden new acknowledgement of inflation. Poppycock. We have been talking about inflation for over six months. But there might be a tiny push from (of all places) Switzerland. Yesterday Swiss National Bank chief Jordan (such a Swiss name) said “the SNB will take care to maintain price stability” and sees the risk of second-round effects. This got quite a lot of attention because the SNB has been silent so far about inflation, unlike all the others. Gittler at BDWiss points out “Jordan didn’t say what the SNB would do in response, but the last time inflation in Switzerland was this high the policy rate was around 2.75%, not -0.75%, the lowest in recorded history. They could raise rates or they could let the currency appreciate further, which would lower the cost of imported goods, especially energy.” Yikes.

Stock Market Rant: The stock market rout was caused by retailers releasing lousy earnings due to inflation—nothing to do with management, mind you. It’s a little unclear how this happens. Had they underpaid for goods sold that now cost more and can be sold for more? In general, retail sales are up. These losers just didn’t have their price of that action. We just had rising retail sales for the 4th month in a row. If sales are up and earnings are down, why do we not blame management?

Bloomberg notes that about Target, where this all started, “Yesterday the stock got absolutely clobbered, with its worst one-day loss since 1987. That came a day after Walmart also had its worst day since 1987. But if you read the Target earnings call, you see the issue was not actually some unexpected plunge in consumer demand. The issue they cited over and over again was the speed of the consumption mix, which caught them flat-footed and over-inventoried.

“Here's CEO Brian Cornell answering a question about US consumer behavior in the face of high inflation: ‘….. We can tell you what we saw during the quarter and the start of May, where we just continue to see a resilient consumer. Our traffic numbers are up to start the second quarter. They're shopping multiple categories.’”

Bloomberg goes on: “Then after the bell yesterday we got Cisco earnings, which sent the stock lower. But it was really all about Chinese supply chain disruptions. Actual demand seems to be robust. Here's Cisco CEO Chuck Robbins: ‘If you combine enterprise and commercial together, we grew 9%, but without the Russia impact, we actually grew 12% and on a trailing 12 months basis it grew 28%. So we are still comfortable with the demand signals that we're seeing and our customers aren't telling us anything differently right now.’"

Some retailers took losses in the quarter. Is that really the calamity of the century? No, not in its own right--unless it triggers a wider sense of conditions out of control, which can help send at least some conditions out of control that otherwise would be stable.

The WSJ has a nifty piece on the risk of recession not actually priced in yet, even though the pullback is substantial. “One example: Microsoft has dropped from 34 times estimated 12-month forward earnings to 24 times since the start of the year—even as predicted earnings have risen. Something similar has happened to the S&P 500 as a whole, where the forward price-to-earnings ratio is down from 22 to 18, while Wall Street has lifted its forecasts for earnings.” (See below.)

So, can you have stock prices falling while earnings, broadly, go up? The WSJ writer ends with this: “The risk of recession has clearly risen, with the European economy heading down, China in a Covid panic, the Fed tightening fast and consumer confidence slumping.

“Even so, I suspect recession is still a ways off if it hits at all, because the jobs market is strong and the Fed has barely begun lifting rates, which are still stupidly low. The trouble is that this view is broadly reflected in markets, while the risk of being wrong is rising.” For what it’s worth, the title fo the piece is “Recession Looms, but Markets Haven’t Got the Message.” Wait a minute—he ends with doubts that a recession is imminent, “if it happens at all.” So it must have been the headline writer who came up with “recession looms.” Ah, but headlines sell newspapers.

More or less at the same time, Bloomberg reported Goldman Sachs CEO Solomon “said clients are preparing for slowing growth and a decline in asset prices thanks to high inflation. But while he says he sees a chance of recession, he added he’s not overly concerned about the risk.” He also named the same 30% probability that got former CEO Blankfein headlined as a stunner only a few days before.

This implies even the smartest and savviest of Wall Streeters don’t see the risk of recession not properly priced in yet. Really? (And Bloomberg is no innocent when it comes to incendiary headlines.) Just two days earlier, former Goldman CEO Blankfein said the risk of recession is rising but still about 30%.

The lesson here is that crowds can easily be made to go nuts when uncertainty is high. Say a thing enough times, and it becomes real. That’s why oft-repeated lies somehow come to be true, as famous liar Trump knows all too well.

Talk of recession has been the obsession for almost six months now. Just for kicks, we sought out the St. Louis Fed’s “recession probability” reading. It doesn’t make the chart this time (updated May 2). Maybe it will, but it’s not there yet. For the cheap-seat explanation, the probability is a function of “a dynamic-factor markov-switching model applied to four monthly coincident variables: non-farm payroll employment, the index of industrial production, real personal income excluding transfer payments, and real manufacturing and trade sales.” (Got that?)

To be fair, the indicator seems to show up only after the recession has started, which is not what we want in a “probability” predictor, but never mind. Its virtue is it doesn’t signal a recession falsely except once.

Note that in the Russian default story below, the WSJ adds “Ms. Yellen says she doesn’t think the war in Ukraine risks pushing the U.S. into a recession.” Europe, maybe.

For the Fed to be raising rates multiple times and an expected 100 bp by the July meeting has nothing to do with the performance of most companies that do not have a high proportion of expenses devoted to debt service. A hefty 20%-plus of small and medium sized companies have no debt, according to Statistica. Various publications like Kiplingers and Barrons periodically list big companies with no debt. Smart big companies already moved their debt into long-term bond issuance at super-low rates. Granted, banks are getting a wider spread between deposit costs and lending rates (which is why Buffett just bought Citibank), but if those borrowers hadn’t figure out their borrowing costs were about to shoot the moon by now, they don’t deserve to be in business. That’s good management under capitalism, red in tooth and claw.

Bottom line: The stock market panic is hysteria. If the price-to-forward earnings of the S&P 500 is now 18, compare to Shiller’s version, which over decades averages 15-17. Shiller uses actual, not forward, earnings, but this is not a time to quibble. The point is that the majority of S&P names see rising earnings and the current P/E’s are not terribly out of line (as they were at the start of 2020 at about 37).

That doesn’t mean bottom-fishing and a bubbly return to higher levels for the indices. It does mean this is an irrational crowd we don’t want to join. Ah, but the stock market panic drove the dollar back up in a swift reversal of what looked like a serious corrective pushback. That implies that if the stock gang does recover it senses and takes the indices back up, the dollar can fall again. Well, yes.

Tidbit: The WSJ features a front-page story on the US finally shutting down Russia’s ability to pay bondholders in dollars. TreasSec Yellen says it won’t make much difference because Russia is already shut out from global capital markets. World Bank economist Rinehart is not so sure—remember where the 1998 Long Term Credit crash started. And Russian bonds prices (due 2047) are already down to about 18 cents from 25 cents a few weeks ago.

Russia wants to pay in rubles but most bonds specify dollars as a matter of course, “including in some coming $100 million in payments due to bondholders on May 27. Payments made to unlicensed accounts in Russia would likely constitute an event of default as well. Additionally, if sanctions preclude banks from processing payments made by the Kremlin, it is possible investors won’t receive any funds at all.” After the 90-day grace period, that means default—and bringing in the lawyers.

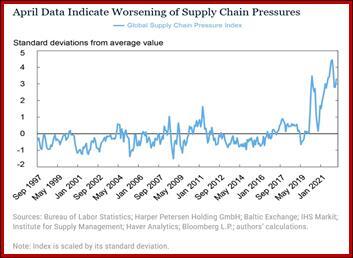

Supply Chain Update: The NY Fed is going to offer monthly update to its Global Supply Chain Pressure Index (GSCPI), “a parsimonious global measure designed to capture supply chain disruptions using a range of indicators. Today we are launching the GSCPI as a standalone product, with new readings to be published each month. In this post, we review GSCPI readings through April 2022 and briefly discuss the drivers of recent moves in the index.” We bet it’s because of massive demand.

“Between December 2021 and March 2022, the index registered an easing of global supply chain pressures, though they remained at very high levels historically. However, the April 2022 reading suggests a worsening of conditions as renewed strains emerge in global supply chains.”

Looking at components, the new disappointment arises from exactly where you’d expect it to—China and Europe as a result of the war. “…. the worsening of global supply chain pressures in April was predominantly driven by the Chinese ‘delivery times’ component, the increase in airfreight costs from the United States to Asia, and the euro area ‘delivery times’ component, as other components have eased over the month. These developments could be associated with the stringent COVID-19-related lockdown measures adopted in China, as well as the consequences of the Ukraine-Russia conflict for supply chains in Europe.” Funny, the US “delivery times” component is not at fault.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat