Market Brief: FTSE roars higher for second straight session

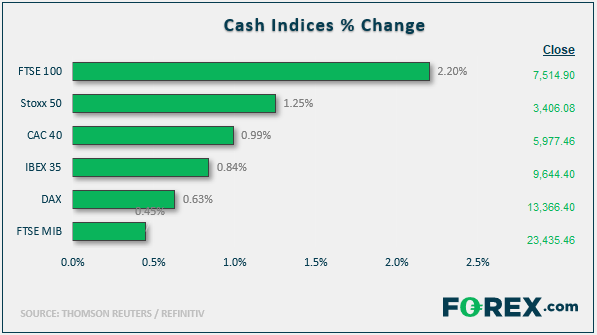

Market Brief: FTSE roars higher for second straight session Market update at just after midday in London: In FX, CAD lead commodity dollars higher while JPY and USD were the weakest. Stocks were higher in Europe, led by the FTSE, after a lacklustre session in Asia overnight and a flat close on Wall Street on Friday. Oil was higher, so too were copper and silver prices. Gold was flat as a weaker dollar and ongoing "risk-on" trade provided conflicting forces.

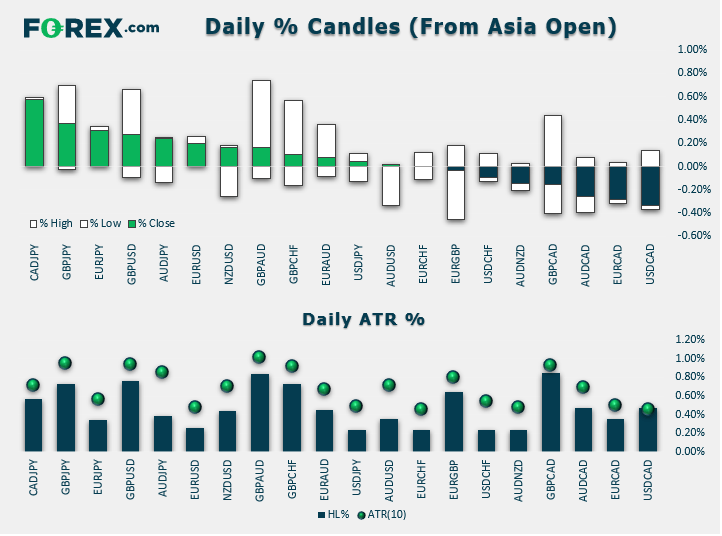

View our guide on how to interpret the FX Dashboard

Sentiment towards risk assets remained positive after the US and China managed to strike a phase one trade deal and as voters in the UK delivered a surprisingly large support for PM Boris Johnson's Conservatives - this has likely paved the way for the Brexit Withdrawal Agreement to be finally passed through parliament, ending months of uncertainty.

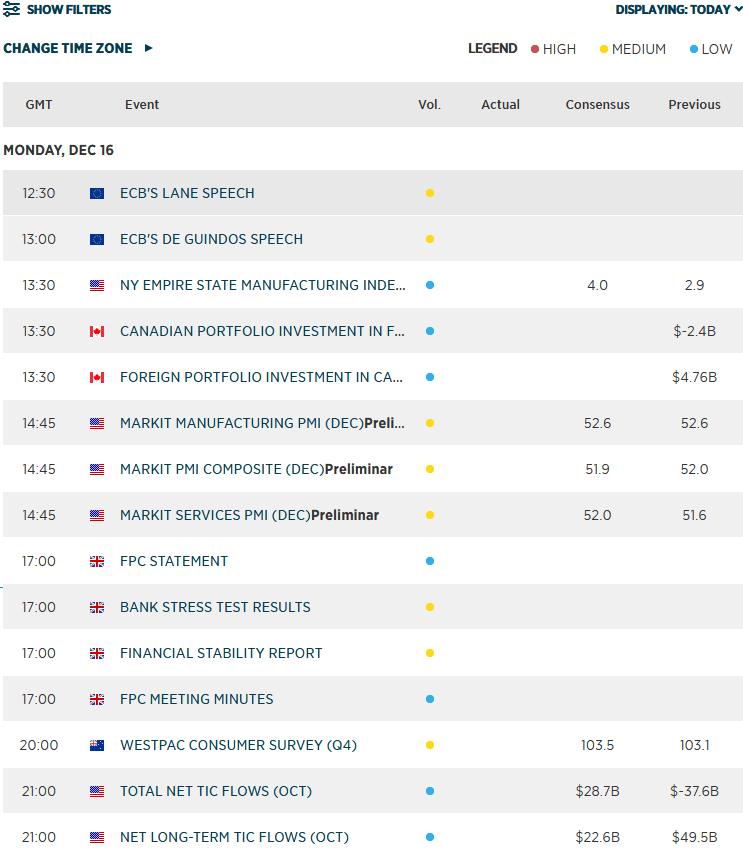

Data recap: Today's economic data releases show a mixed real economy. China' retail sales (+8% y/y) and industrial production (+6.2% y/y) both topped expectations, while surveyed purchasing managers among manufacturers in UK (47.4), France (50.3), Germany (43.4), and Eurozone (45.9) reported deteriorating economic activity in the sector. However, these were offset by better than expected services PMIs from France (52.4), Germany (52.0) and Eurozone (52.4), although the UK PMI (49.0) was weaker.

GBP: Despite the soft UK PMI data, the pound refused to give back any meaningful chunk of its election-linked gains. Investors realise the PMI data reflects sentiment before the outcome of the election was announced. UK data may well improve in the months ahead given the clearing of the dark Brexit clouds that had brought a gloomy feeling among businesses and households.

Stocks: UK markets have jumped higher for the second session. This comes after Boris Johnson's big election victory alleviating some Brexit-related uncertainty. It looks like we are not the only ones bullish on the FTSE as outlined in the Week Ahead report on Friday. Goldman Sachs said it was particularly bullish on UK homebuilders and banks that have struggled recently. "Clarity on the UK's terms of exit from the EU should unlock pent-up business investment; the reversal of a decade of fiscal consolidation should provide a fillip to domestic demand; and a pick-up in global growth should underpin a recovery in net exports," the bank said in a note.

Coming up:

Author

Fawad Razaqzada

TradingCandles.com

Experience Fawad is an experienced analyst and economist having been involved in the financial markets since 2010 working for leading global FX, CFD and Spread Betting brokerages, most recently at FOREX.com and City Index.