Market Brief: AU Unemployment Lifts AUD, DUP Weighs on GBP

FX Brief:

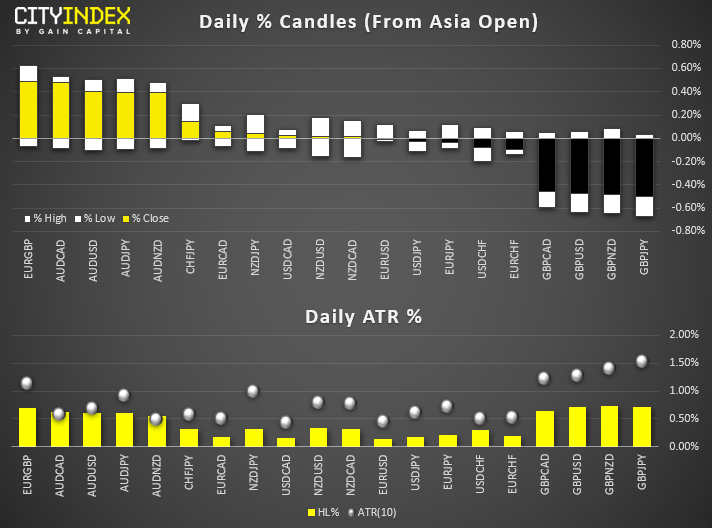

AUD is the strongest major after AUD unemployment fell unexpectedly to 5.2%, which will be a relief for RBA. AUD/USD temporarily hit a 4-day high before paring gains, AUD/JPY broke out of compression, and AUD/NZD broke out of its bullish flag. AUD/CAD and AUD/NZD are the only pairs to meet or exceed their typical daily ranges, making them less appealing for an extended move. AUD/USD reached 88% of its typical ATR, so for extended gain we’d need to see a catalyst for a weaker USD.

The pound dropped and is the weakest major after DUP said they cannot support the Brexit deal as it stands. With GBP looking stretched on the daily charts and only hitting about 50% of its typical daily range following comments from DUP, traders could keep an eye for some bearish follow through on GBP crosses.

Negotiations are underway to nail down phase 1 trade deal between US and China, according to Steven Mnuchin, who added he’s willing to go to Beijing for more meetings if necessary.

Singapore’s exports fell -9.5% YoY, making it the 7th consecutive month of declines.

BoE’s Mark Carney doesn’t see negative rates as part of the central bank’s toolkit.

EUR/USD remains just off yesterday’s 1-month high, USD/JPY continues to consolidate around 108.70, above 108.47 support. USD/CNH remains steady around 7.10.

Equity Brief:

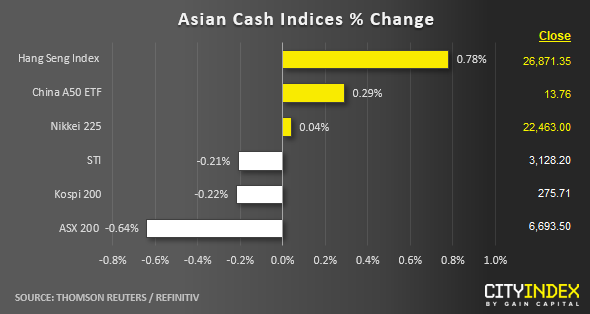

Asian stock markets are trading in a mixed fashion so far in today’s Asia mid-session after 3-days of gains.

Hong Kong’s Hang Seng Index has continued to extend its up move after 2-days of consolidation where it has rallied by 0.78% despite rising political tension between U.S. and China over Hong Kong. Leading U.S. senators have voiced support on a bill that backs the Hong Kong’s pro-democracy movement and wants Senate to start the voting process quickly. China has continued to issue “retaliatory” remarks over the bill.

Also, the Hong Kong SAR government has announced one of the boldest housing polices to address rising home prices by taking back large tracts of land held by major developers and create more public housing. Other measures include public-private partnership scheme to build housing and relaxing the property value cap for mortgages where such measures have boasted the shares prices of Hong Kong property developers that is leading the on-going rally in the Hang Seng Index. New Word Development, Sun Hung Kai Properties and Henderson have rallied between 3% to 5%.

Over at the other end of the spectrum, Australia’s ASX 200 has underperformed where it has declined by -0.64% led by key mining stocks over concerns on plunging iron ore prices. The price of iron ore has tumbled by more than 3% to hit a 6-week low yesterday after China’s top steelmaking city of Tangshan issued a smog alert that requires mills to further limit operations. Share prices of BHP and Rio Tinto have declined by -2.5% and -2.1% respectively.

The S&P 500 E-Min futures is almost unchanged in today’s Asian session as it has traded in a tight range of 7 points, holding above yesterday’s low of 2984.

Up Next

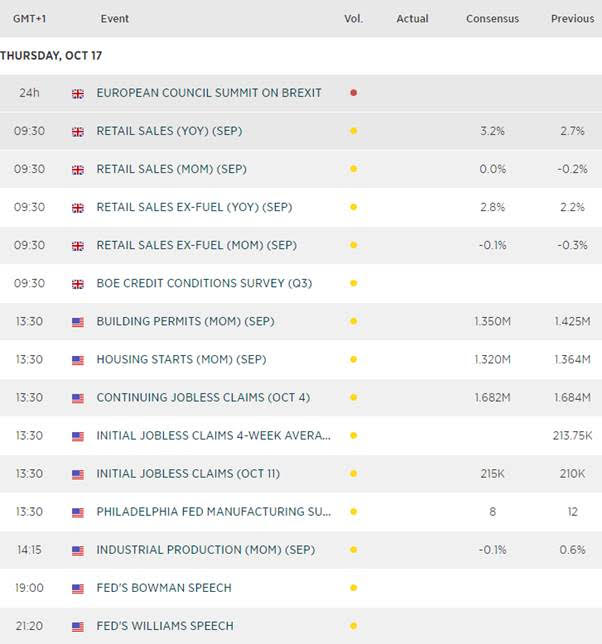

UK retail sales is expected to recover to 3.2% YoY after falling to 2.7% last month on weaker online sales. Monthly retail sales are expected to dip -0.1% versus -0.3% previous. Naturally, Brexit headlines are going to be the bigger driver for GBP crosses, although worth noting that cable did fall 80 pips following a slew of weak data yesterday, where CPI, PPI and retail prices. Whilst we may not see the same reaction with a miss today, it would add further weight to the weaker data.

US building have surged since the Fed cut rates (up 15.5% YoY) and is considered a leading indicator to the broader economy, given it feeds into construction, mortgages and therefor consumer sentiment. It may not be a huge market mover, but something to consider as markets are heavily expecting further cuts from a Fed who don’t sound overly dovish.

Author

Matt Simpson, CFTe, MSTA

CityIndex

Matt Simpson is a certified technical analyst who combines charts and fundamentals to generate trading themes.