Macro Events & News

FX News Today

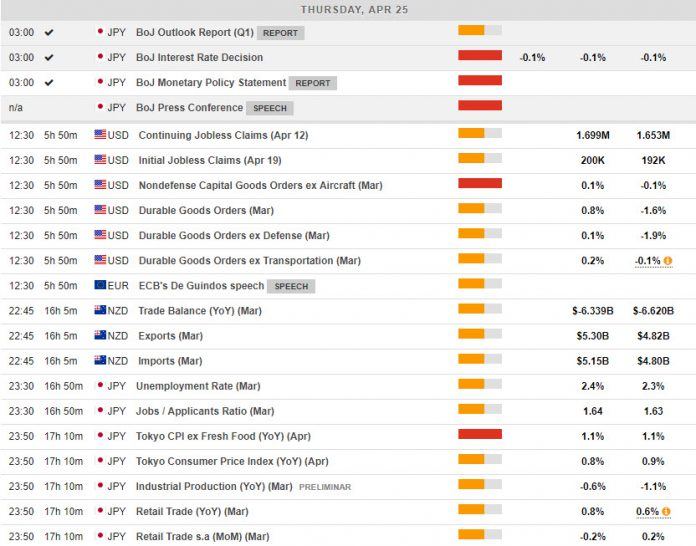

The BoJ left rates unchanged, but clarified its forward guidance, saying it will keep rates very low at least through to the spring of next year.

Also, they will expand the eligible collateral and also consider the introduction of an Exchange-Traded Fund (EFT) lending facility, that would allow to temporarily lend EFTs that the Bank holds to market participants.

Japanese stock markets outperformed going into the announcement, but mainland China indices were under pressure.

Stock futures are moving higher in Europe and the US. The weaker than expected Ifo reading yesterday and a negative GDP print from South Korea overnight added to concerns about the outlook for world growth, which will mean rates will stay low for longer.

The Swedish Riksbank is widely expected to keep monetary policy on hold today.

Tthe front end WTI future is trading at USD 65.91 per barrel.

Charts of the Day

Technician’s Corner

USDCHF is consolidating since last night within 1.01970-1.02190 range. However the pair still holds above 1.0200, suggesting the continuation of the uptrend, as the pair remains well above the medium term Support at 1.0123 level (6 month Resistance converted to Support. Intraday, however, and as momentum indicators have been flattened, consolidation mode could possibly hold within the day. A cross below 1.0200 could retest yesterday’s lows.

AUDUSD within the strong 3-year Support, 0.7000-0.7020. It could react as a retracement level for the asset. However the 3 black crows in the daily chart suggest that negative bias is increasing for AUDUSD.

Main Macro Events Today

Durable Goods (USD, GMT 12:30) – March durable goods orders are expected to rise 0.2%, following a 1.6% February decline. Shipments expected to fall 1.5% in March, after a 0.2% reading in February.

NZ Trade Balance (NZD, GMT 22:45) – The trade report is expected to show an improvement in the surplus to NZ$300 mln in March from NZ$12 mln in February.

Tokyo CPI and Production Data (JPY, GMT 23:30) – The country’s main leading indicator of inflation is expected to have remained at 1.1% y/y in April. Industrial Production is expected to have improved, growing by 0.6% m/m in March, compared to -1.1% m/m in February, while Retail Sales are expected to have increased by 1.2% y/y, compared to 0.6% in March.

Support and Resistance

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in