Macro Events & News

FX News Today

Asian Market Wrap: Stock markets continued to rally during the Asian session after a record close on Wall Street yesterday. Risk appetite is back after robust US data yesterday added to hopes that the fallout from the latest round of US-China tariffs can be contained and that there will eventually be deals on trade and Brexit, despite little progress at the informal EU summit yesterday. Improvements in emerging market assets have also helped to underpin confidence with investors buying back into the rout. 10-year Treasury yields moved up 1.3 bp to 3.076%, 10 year JGB yields jumped 1.6 bp to 0.125% and 30-year yields rose 4.4 bp as BoJ cut bond purchases. Topix and Nikkei are up 1.01% and 1.06% respectively underpinned by a weaker Yen, the Hang Seng has gained 1.13% so far and the CSI 300 is up 1.80%. US stock futures are equally broadly higher, Oil prices are slightly lower and the November WTI future is trading at USD 70.25 per barrel. Today’s calendar includes Eurozone PMI readings as well as public finance data for the UK.

FX Action: USDJPY has lifted to a fresh two-month high at 112.80 amid a backdrop of a coursing risk-on theme in global markets. The USA30 and USA500 hit record highs yesterday, and Asian stocks have rallied robustly across the board. JP225 hit a 4-month high, and the Shanghai Composite a two-week high, with both showing gains of 1% or more. Expectations for China to turn the fiscal stimulus tap, among other measures, have been helping underpin sentiment in Asia, while the unexpectedly low starting tariff rate of 10% in Trump’s latest move on Chinese imports this week, along with tech sector exemptions, have helped buoy sentiment Global fundamentals are otherwise solid, despite the threat from the trade war escalation (with Beijing not expected to negotiate until after the mid-term elections in the US).

Charts of the Day

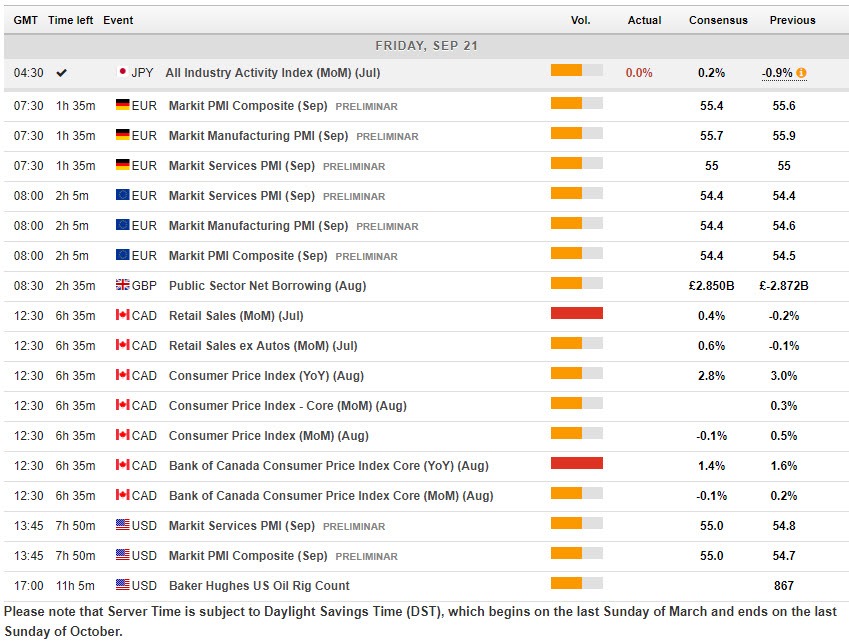

Main Macro Events Today

Eurozone Sep. PMI – Expectations – The Eurozone manufacturing PMI is expected at 54.5, down from 54.6 in the previous month, and expect the services reading to improve slightly to 54.5, which should leave the composite unchanged from August at 54.5. This still suggests ongoing expansion, but would also confirm the decelerating trend.

Canada CPI & Retail Sales – Expectations – CPI is expected to hold steady in August after the 0.5% surge in July. The CPI is projected to grow at a 2.9% y/y pace in August, easing slightly from the 3.0% pace in July that was the top of BoC’s 1-3% target range. Canada retail sales values are expected to rise 0.5% in July after the 0.2% drop in June.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in