Macro Events & News

FX News Today

European Fixed Income Outlook: Stock markets mostly moved higher in Asia, after another positive close on Wall Street. China and Hong Kong alongside other markets were closed for Lunar New Year holidays, which muted trading, but the Nikkei gained 1.19%, while the ASX lost early gains and closed with a marginal loss of -0.08%. The yen continued to advance and 10-year JGB’s dipped -0.8 bp to 0.049%, as Kuroda was nominated to lead the BoJ for another five year term. 10-year Treasury yields declined -0.5 to 2.904% and oil prices picked up slightly, with the March Nymex future trading at USD 61.51 per barrel.Kuroda officially nominated for second term as BoJ governor. As widely expected Abe nominated Kuroda to stay another five years and reports that Waseda University professor Wakatabe, along with BoJ Executive Director Amamiya, will take the deputy governor roles were also confirmed. The nominations were sent to the steering committee of parliament’s lower house and will have to be confirmed by both houses of parliament. Wakatabe is known for advocating “bolder monetary easing” and Amamiya has worked closely with Kuroda. The move should ensure another five years of monetary stimulus from the BoJ and is likely to have underpinned the dip in 10-year BoJ yields today.

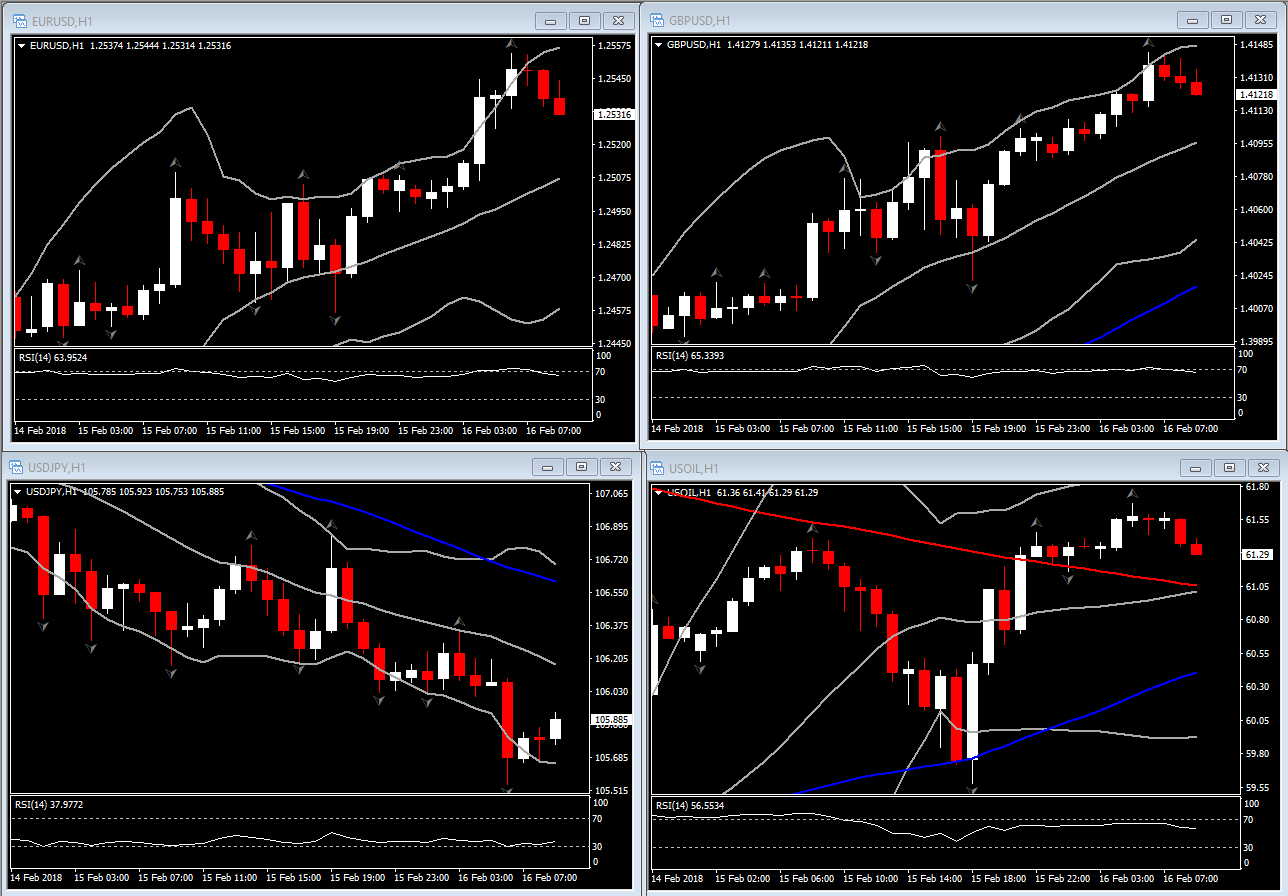

FX Update: Another day, another decline in the dollar, which logged a new 38-month low versus the euro, at 1.2554, and a 15-month low against the yen, at 105.54. The USD index (DXY) is down by 0.3%, 88.37, earlier clocking a 37-month low at 88.33. The greenback has also seen fresh lows against most newly developed and developing world currencies. Continued gains in global stock markets have continued to inspire dollar selling, as investors seek out higher yielding opportunities. USDJPY declines came despite the nomination of Kuroda for another term at the helm of the BoJ, along with nominations for the two deputy governor positions of inflationist candidates, Amamiya and Wakatabe.

Charts of the Day

Main Macro Events Today

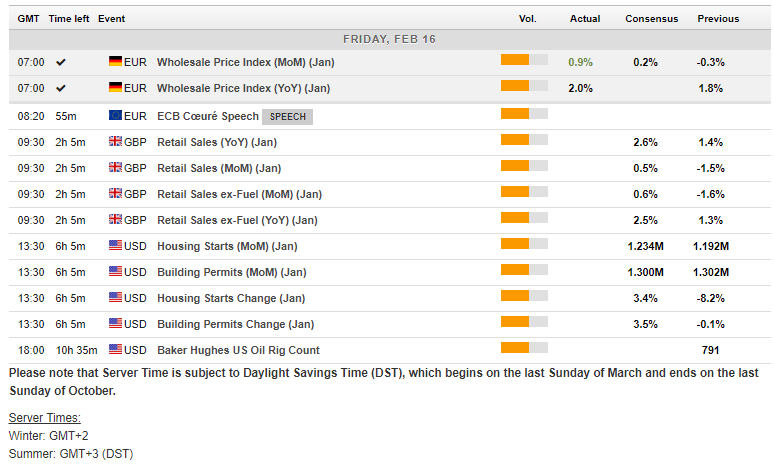

UK Retail Sales – a 0.5% m/m rebound is anticipated after the sharp, and at the time much weaker than expected, 1.5% contraction in December.

Canadian Manufacturing Sales– shipment values, are expected to reveal a 0.2% gain in December after the 3.4% surge in November. The projection is driven by 0.6% rise in export values during December that came on the heels of a 3.6% surge in November.

US Building Permits and housing Starts – January housing starts are expected to rise 0.6% to a 1.23 mln unit pace, while Building Permits are seen at 1.30mln.

US Prelim UoM Consumer Sentiment – is forecast to rise to 95.5 in February from 95.7.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in