Macro Events & News

FX News

European Outlook: Asian stock markets are mixed, with Japan outperforming and the Nikkei up more than 1%, after the S&P 500 rose to a fresh record high and Fed’s Dudley said that U.S. expansion has “a long way to go”. Hang Seng and CSI were little changed in cautious trade ahead of the MSCI decision on the inclusion of Chinese shares in the index. The ASX meanwhile was weighed down by property shares. U.K. and U.S. stock futures are also moving higher, suggesting that yesterday’s rally will be extended today. The DAX is starting to eye the 12900 marks again and the FTSE 100 is firmly above 7500. With stock markets eying new highs core yields are likely to continue to nudge higher, while? Eurozone peripheral bond markets should continue to benefit from the improvement in sentiment. Yesterday’s first official meeting of Brexit negotiators brought a conciliatory tone, but little detail apart from a time table and the confirmation that there won’t be talks on a post-Brexit trade deal alongside the divorce agreements. The calendar today remains quiet, with only Eurozone current account and BoP data.

EU and U.K. agree timetable for Brexit talks, with initial negotiating groups tackling first Citizens’ rights, financial settlement and finally other separation issues. An additional dialogue on Ireland/Northern Ireland has been launched, but there was no mention of a post-Brexit trade deal which the U.K. initially wanted to negotiate alongside the divorce terms. Nothing further really happened yesterday at the first talks between chief negotiators Barnier and Davis and the next round of talks will start on July 17, with further rounds scheduled for the weeks starting August 28, September 18 and October 9. There reportedly wasn’t an offer from the U.K. yet on the rights for the EU citizens in the U.K.

Canada U.S. lumber dispute simmers, underpinning export uncertainty: a Bloomberg article from yesterday summarizes the viewpoints of the two sides in the dispute, with the U.S. upbeat for a quick resolution while Canada is cautious. The lumber dispute is among a variety of trade issues between the two nations, but is the most prominent and dates back to the Obama administration. Other industries remain at risk of increased tariffs, with Globeandmail.com reporting that the U.S. could add steel pipe makers to its target list of Canadian industries. The ongoing jockeying for tariff protections by various U.S. industries is a timely reminder of one of the key uncertainties facing Canada’s growth outlook. Wilkins, in her speech last week that shook up the BoC policy outlook, acknowledged the political uncertainty surrounding the Trump administration. That uncertainty shows few signs of diminishing, which we suspect will help keep the current monetary policy rate intact for a while longer.

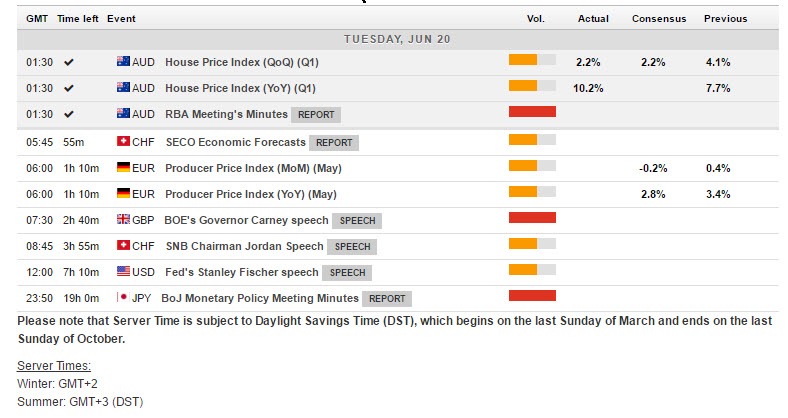

Germany: The Producer Price inflation falls back to 2.8% y/y in April from 3.4% y/y in the previous month. This is a tad lower than anticipated, with the decline in oil prices from the highs earlier in the year one of the factors bringing both producer and import price inflation down again. The ECB has already cut back its inflation projections due to a revised oil price forecast. so the data doesn’t change the ECB outlook.

Main Macro Events Today

CAD Wholesale trade – Canada’s calendar has wholesale trade, with shipment values expected to expand 0.5% m/m in April after the 0.9% bounce in March.

US Current Account – The Q1 current account deficit is expected to widen to -$124 bln. As a percentage of nominal GDP, the gap is expected to widen to -2.6% from -2.4%.

SNB Jordan Speech – SNB Governing Board Chairman Thomas Jordan will be at the opening of Swiss International Finance Forum, in Bern, in which it will also be involved in a panel titled “Moving away from the expansive monetary policy: what are the effects on financial markets and the real economy?”.

Fedspeak – VC Fischer and non-voter Rosengren will be at the podium at a conference on macro-prudential policy at the Riksbank. Also, the moderate hawkish voter Kaplan discusses monetary policy and the economy at a Commonwealth Club event. Governor Powell testifies on fostering economic growth before the Senate Banking Committee.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in