Labor is the key word

Outlook

Today we get the service sector PMI from S&P and ISM, along with Q2 labor costs and productivity. Labor is the key word. We get the ADP private sector job creations and the usual weekly unemployment.

The Beige Book was pretty dark. Only 4 regions reported modest growth, meaning the other 8 were flat or down. The word “tariffs” appeared 69 times vs. 40 in the July Book. A few points: every regions saw price increases. Consumer spending is soft because wages are not keeping up with rising prices.

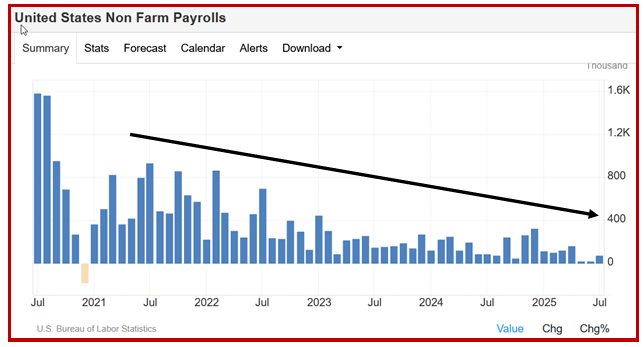

As for payrolls, JOLTS gave a boost to the rate cut idea that ADP will not likely negate but instead push. Mr. Powell is worried about jobs and he is getting the ammunition he needs for the rate cut in Sept.

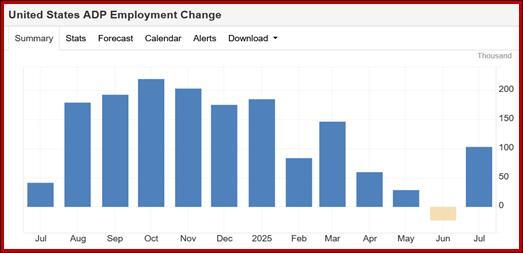

ADP private sector payrolls today arrives in the context of 104,000 new jobs in July, the best gain since March and more than forecast. Services led with 74 k and goods production had 31 k. Trading Economics reports “The survey also showed that year-over-year pay growth remained solid in July, at 4.4% for job-stayers and 7.0% for job-changers—unchanged for the fourth consecutive month.” In other words, not too bad. See the chart. The current consensus forecast is for a gain by 65,000 new jobs. Gee, sounds like last time—maybe not hard to beat.

We are left with the same pinball effect of a rate cut at the same time inflation is almost certainly not going to be a single, one-time thing. Companies are rearranging their supply lines and taking about one third of the new cost, while probably another third is accommodation by exporters, leaving one final third for the consumer. At least this is what the Fed hopes for. But whatever the breakout, it’s not one-time, as we saw from the Richmond Fed survey earlier—companies expect to raise prices in Q4 and 2026.

Bloomberg writes “Positioning in stock, bond and gold markets suggests that investors are preparing for a potential rise in inflation.” Gee, d’you think?

Forecast

We are newly encouraged by the yield crisis yesterday resolving itself into calmer waters. Yields fell back everywhere but US yields in particular fell back, with the 2-year hitting a 4-month low and the 10-year returning to where it was at the beginning of August. The 30-year retreated 10 points from 5%.

Apparently the JOLTS report gets most of the credit, which is fairly rare. Today’s ADP jobs and unemployment claims and tomorrow’s monthly payrolls should seal the deal—a rate cut is justified. The market is already there with a 97.6% probability on the CME FedWatch.

Payrolls are forecast at about 75,000 (Bloomberg survey consensus) and that’s not enough to keep the economy trundling along at about 3% (the last Atlanta Fed GDPNow for Q3).

We get another Atlanta Fed forecast today. Let’s assume it’s not much different. Since payrolls are expected to be sub-par, can we get a headline move? Yes, at least a small one, especially if the number is far under the 75,000. Say it’s 35-40,000. What happens? The idea of stagflation, if not recession, come out from behind the curtains where it has been biding its time. Economists say told-you-so. But what about that Atlanta Fed estimate? Now everyone is totally confused.

Still, a bad series of payrolls numbers is dollar-negative. If we get an upside euro breakout, the target would be 1.1775, the most recent highest high from July 23.

Tidbit: The top two cases going to the Supreme Court are the tariffs and deportations, each based on a wrong interpretation of presidential powers, according to Constitutional experts. Bloomberg writes the Supreme Court will have to stop dodging Trump and decide if they support a strict reading or are willing to go along with their weird judgment that everything a president does in office is okay. Bloomberg shows it does have a way out.

We may think the tariff case is relevant to financial markets and the deportation case not so much, but the central point remains whether there is a Constitutional check on Trump’s quest for total power. And this the world is watching. It’s a little strange that the average citizen in the UK, Switzerland and Japan knows as much about this issue as Americans, maybe more.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat