Key events in developed markets and EMEA next week

In the US, retail sales data may show solid growth for December as consumer confidence was buoyed by rising equity markets. In the UK, sticky services inflation will be in focus, as this could delay a Bank of England rate cut until the summer. And in Poland, we forecast the initial estimate of December CPI inflation to be confirmed at 6.1% .

US: Retail sales are likely to have grown solidly in December

Even though the December jobs and inflation numbers came in somewhat hotter than expected, financial markets continue to gun for rate cuts, with 150bp priced for the end of 2024. We expect reasonably firm data again this coming week, but the focus is likely to be on whether Federal Reserve officials look to push back against what the market believes.

US retail sales are likely to have grown solidly in December, with consumer confidence buoyed by rising equity markets. We know that auto volumes rose 3% to an annualised 15.8m units while weekly credit card spending numbers held up well, with prices rising 0.3% month-on-month, according to CPI data – remember this is a dollar value figure report. Industrial production won’t be as robust though, expanding perhaps 0.1%, with manufacturing set to be close to flat on the month given the ISM manufacturing report has been in contraction territory since October 2022. Autos may be a bright spot as output continues to recover from earlier strike action, but weak order books are an issue for most other sub-sectors. Utilities output will be a drag given warm weather implies less heating demand while oil and gas extraction may have been helped by those warmer weather conditions.

Housing starts and existing home sales data will also be published. Housing starts surged 14.8% in November and a substantial correction lower is expected for December in what has become quite a volatile series. There is a lack of existing homes for sale and this is supporting new home construction, but means that existing home sales are likely to continue to languish. Mortgage applications for home purchases remain close to 30-year lows and home sales are likely to remain at the levels seen at the bottom of the housing crash during the Global Financial Crisis.

Also watch out for the Federal Reserve’s Beige Book. This anecdotal survey on the state of the economy often contains valuable insights on what is happening in the economy that don't get reflected in some of the official data until much later. The Fed also places a lot of significance on this report.

UK: Sticky services inflation to delay BoE rate cut until the summer

UK services inflation looks set to come in at 6.1% next week, well below where the Bank of England had forecast it back in its November policy report. Along with wage growth, which has also finally started to moderate, these are the key metrics upon which the Bank has signalled it will base its rate cut decisions. For now though, 6%+ services CPI is still too high and it’s likely to stay in this region into the first couple of months of 2024. But things will start to change as we head towards summer. Thanks to moderating food and consumer goods inflation, as well as lower petrol prices, headline inflation is set to fall to 1.6% in May on our current forecasts. Services inflation should be down to 4% by the summer too. Assuming we get a fiscal boost in March – we forecast the Chancellor’s £13bn headroom will double at the next budget, enabling tax cuts – the Bank of England may be tempted to wait a little longer before cutting rates. We’re forecasting an August cut, though faster-than-expected declines in services CPI and/or wage growth could conceivably see that date come forward.

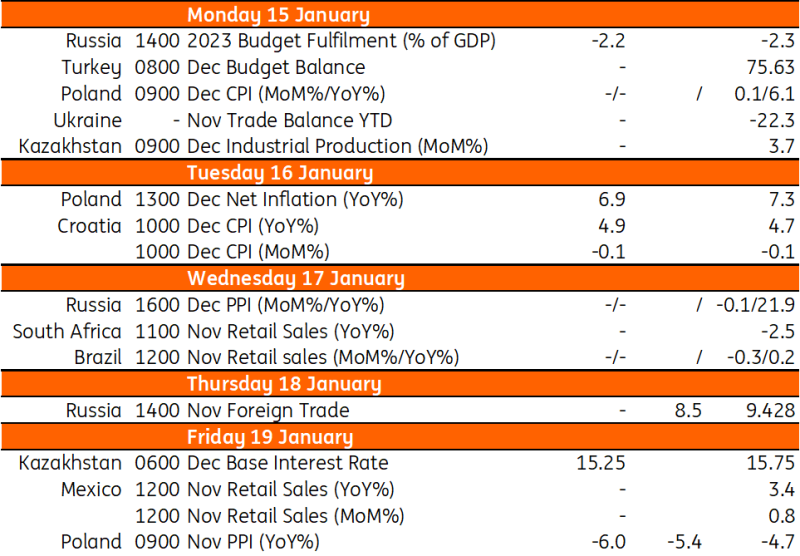

Poland: We expect the initial estimate of December CPI inflation to be 6.1% YoY

CPI (December): 6.1% YoY

We expect the initial estimate of December CPI inflation to be confirmed at 6.1% year-on-year. Food price growth fell short of our forecast and the decline in monthly gasoline prices turned out to be smaller than we expected. According to our estimates, core inflation excluding food and energy prices continued to moderate, reaching around 6.9% year-on-year vs. 7.3% YoY in November.

PPI (December): -6.0% YoY

Following a temporary pause in late 3Q23, the level of producer prices started to head south, contributing to continued deflation in YoY terms. We forecast that in December, PPI fell by 6.0% YoY following a 4.7% YoY drop in November. The MoM prices fell in all the main areas (manufacturing, mining, energy production) with the exception of water supply. PPI deflation may be continued until mid-2024.

Key events in developed markets next week

Source: Refinitiv, ING

Source: Refinitiv, ING

Read the original analysis: Key events in developed markets and EMEA next week

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.