Italy's and Europe's Confounding Elections

The political consensus that has dominated Europe since the Second World War and driven unification from the six nations of the Coal and Steel Community of 1951 to today's 28 member European Union and 19 country monetary union is fraying after five straight electoral disappointments and is headed for a sixth in Italy, yet markets have not registered more than a tremor.

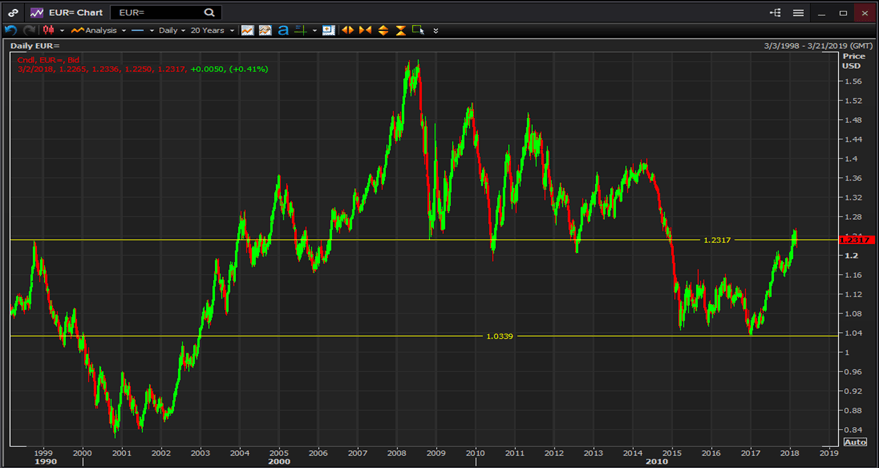

The euro is at a three year high against the dollar, European equities are full participants in the 10-year bull market and most sovereign interest rates have climbed from their nadir of a year ago.

Why hasn’t the political turmoil in the U.K. and the European Union affected the financial markets?

In the aftermath of the British vote to leave the European Union in June 2016 the euro fell to a fifteen year low against the dollar and sovereign rates dropped into a historical trough as the European Central Bank sought to counter concerns that the skeptical sentiments of the U.K. vote would manifest themselves, even triumph, in the Dutch, French and German national elections in 2017 and in the simmering Catalonia independence movement.

-636555798363972161.png)

The first post-Brexit vote in Holland on March 15th set the pattern for what was to follow. Established parties whether of the center-left or right, long the arbiters of European politics, lost heavily to the right wing and a slew of smaller parties of both stripes.

In the Dutch election, Geert Wilders' nationalist and Euro-skeptic Party for Freedom (PVV) won 20 seats, gaining 5, making it the second largest party in the House of Representatives.

However, the result fell short of its own expectations and media fears. Prime Minister Mark Rutte with 33 seats for his People's Party for Freedom and Democracy (VVD) lost 8 places but was able to form a coalition with three smaller parties, though it took a record amount of time to October, and continue in office.

The Labour Party, Rutte's previous coalition partner, the second-ranking party after the 2012 election and a post-war mainstay of Dutch politics was shredded, plunging 29 seats to seventh place in the 150 member house.

Two months later the French presidential vote provided a similar comeuppance for the post-war establishment. Emmanuel Macron a former economics minister who had never run for elected office before, and had formed his own party, En Marche, a year before, decisively defeated Marine Le Pen of the National Front. The 26 percent combined share of the traditional right and left parties, the Republicans and the Socialists, neither made it to the second round, was the lowest in French history.

Though the National Front lost a 2 to 1 vote (66.1 percent to 33.9 percent) it nonetheless doubled its percentage from its previous appearance in a national election under party founder and Marine Le Pen's father Jean-Marie in 2002 when it garnered 17.8 percent.

The German election in late September continued the dissolution of standard politics. The Christian Democratic Union (CDU) of Chancellor Angela Merkel won just 33 percent of the vote, shedding 9 points and 65 Bundestag seats to its weakest showing since 1949. The Social Democrats (SPD), Merkel's coalition partner heading into the vote, came in second place at 26 percent, losing 40 seats.

In the biggest shock to the German establishment, Alternative for Germany (AfD), a right-wing party founded in April 2013 scored 12.6 percent of the vote making it the third-ranking party in the legislature. Described variously as nationalist and populist, Euro-skeptic and anti-immigration, it is the first appearance of an avowedly right-wing party in the Bundestag in post-war history.

Initially, Martin Schultz the leader the SPD said that his party would not enter another coalition with the CDU. But in the five months since the election, Ms Merkel has been unable to form a government with any of the smaller parties after ruling out any association with the AfD. It has been the longest government interregnum in German parliamentary history.

As of this writing (3/2/18) SPD members are considering the party's second coalition agreement with Merkel's CDU. If approved it would bring the Chancellor her fourth term. Failure will almost certainly lead to new elections.

The non-binding Catalan independence referendum held on October 1st despite the opposition of the national government of Prime Minister Mariano Rajoy claimed a 92 percent approval. But with the regional Catalan administration immediately suspended by Madrid, its leader Carles Puigdemont in Belgian exile and the independence movement without European or EU support, its potential to upset Spanish or EU governance is fading rapidly.

In the period after the Brexit vote in June 2016 the possibility that one or more of the elections in the coming year would mimic the British result weighed heavily on the euro. The decision to leave the European Union clearly represented European wide sentiments. The questions were how strong was the discontent and how successful would its political representatives be?

Weak economic growth, a distant and unresponsive EU bureaucracy in Brussels, insular ruling classes, immigration problems that seemed both immediate and beyond national control and the supplanting of domestic sovereignty were issues that were present in a greater or lesser degree in all of last year's European elections.

But despite the fears and the growing electoral strength of the politicians who banked on these issues none of them reached power. Geert Wilders in Holland, Marine Le Pen in France and Alice Weidel and Alexander Gauland in German had to settle for their best showings in history but they remained in opposition. European voters were not ready to endorse the drastic solutions proposed by these candidates.

The steady rise of the euro in the first three quarters of 2017 reflected the limitations of the challenge to the ruling European political and economic orthodoxy. As the threat faded the euro steadily gained ground in spite of the diverging interest monetary policies of the European Central Bank and the U.S. Federal Reserve which increased rates three times in the year.

Italy's election this Sunday is the latest in this season of European discontent. The 5 Star Movement, the populist party founded by former comedian Beppe Grillo is leading in polls, slightly ahead of the current ruling Democratic Party headed by former Prime Minister Matteo Renzi, and former Prime Minister Silvio Berlusconi's Forza Italia, and trailed by two smaller parties.

5 Star is a particular Italian strain of European populism, more a revolt against Italy's entrenched political class than an economic complaint, though growth has been stagnant on the peninsula for 15 years. Its eclectic program takes ideas from across the political spectrum and technological development. Its views on immigration are essentially centrist and while it once favored leaving the Eurozone, it leaders now say that time has passed.

In one aspect the Italian election may be singular. 5 Star may receive enough votes so that it would almost have to be included in any coalition. Mr. Grillo has rejected that possibility, saying that unless the party wins an outright majority it should remain in opposition.

If no party or coalition wins a parliamentary majority, Italy's president may ask parties to form a cross-party coalition, but the chance of a stable government in Italy's fractious political system is remote. If that fails he could call fresh elections, but with the electorate divided and no political or economic development on hand to change the balance another ballot would be unlikely to produce anything more than a temporary result.

Whatever the outcome of Sunday's election the actual political change in Italy, as it was in Holland, France and Germany, is likely to be minimal. Markets have barely registered the election, a clear sign that nothing untoward is expected.

Europe is restive but not yet rebellious. It will take much greater political and economic upheavals to make abandonment of the euro and the EU into a winning political agenda. But that does not mean the unified future is secure. Demographics and economics are not on the continent's side. Unless Europe’s current rulers can find the will and political capital to correct current trends these recent elections will simply be the forerunners of far more dangerous and threatening politics in the future.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.