It is generally assumed that ECB is ready to defend it’s no-tightening stance

Outlook: The calendar has many entries but the biggie is Friday’s nonfarm payrolls (and before that, the ADP private-sector forecast). On Dec, the US added only 199,000 jobs, the least of any month in that year. The whole job picture is confusing and we are sure to get more information about the Great Retirement. It’s a little interesting that CNN commentator Smerconish asked his viewers on Saturday whether it was changed in the economy’s structure or laziness/government handouts driving the labor shortage. The vast majority voted for structure.

About those rate hike projections: one summary has it that Barclays and UBS foresee three hikes. JP Morgan, Deutsche Bank, Wells Fargo and Goldman Sachs project five. BNP Paribas has six. Bank of America has seven, meaning one at every FOMC meeting plus four more in 2023, taking fed funds to 3.00% at the end of 2023. Nothing affirms that Fed funds futures are just guesses (or wishes) than numbers like these. Also out in fairyland–Atlanta Fed Bostic said yes, the March hike could be 50 bp, and Bloomberg reports it now has a roughly one in five chance. Bostic told the FT that three hikes is not all that much considering the economy and it should go without saying the Fed won’t plunge the economy into recession.

Before we get to US payrolls, the ECB meets on Thursday and is generally assumed to be ready to defend it’s no-tightening stance. Inflation numbers are coming in, with the eurozone composited expected at 3.5-5%. Meanwhile, Q4 GDP is up 0.3% y/y and 4.6% year-over-year.

The Fed insists that it is flexible enough to engineer a soft landing. This is defined roughly as bringing inflation to heel without getting a recession as a consequence. The Fed faces more than one opponent in this quest–not only a flaky equity market and liquidity issues that accompany contracting the balance sheet, but the hard inflation stuff itself, most of which is outside its sphere of influence. Like commodities, including oil. See the chart and table from Trading Economics. The rise in commodity prices is immune to anyone’s interest rates (and a great mystery to those trading the commodity currencies).

Then there’s the supply chain problem, which as even Powell admitted is worse than we knew and not likely to get fixed within a few months. You don’t have to be a grumpy pessimist to imagine that the five rate hikes projected by the big banks ae not so nuts in that face of inflation becoming not only persistent but entrenched. If this viewpoint becomes general, it removes a great deal of the dollar’s moxie.

Unpacking Friday’s Data: Personal income rose 0.3% after 0.5% in November, while spending fell by more, percentage-wise, 0.6% (and November revised down, too) for a rise in the savings rate to 7.9% (from 7.2%). This returns the savings rate to the pre-pandemic level and you can discuss what that means all night. Are we through with Covid and not scared anymore? We overspent in 2021 and need to replenish savings?

Headline PCE inflation rose 0.45% after 0.42% the month before for a year-over-year rate of 5.8% from 5.7%, as expected. Core PCE inflation rose 0.5% (from 0.46%) on the month for 4.9% y/y.

The Q4 employment cost index for Q4 failed to meet expectations and rose only 1% q/q from 1.3% in Q3. Trading Economics notes that on an unadjusted basis, costs rose 4.0%, the most since 2001 and far more than 2.5% in 2020. “In 2021, wages and salaries rose 4.5 percent while benefits were up 2.8 percent.” Was the jump in Q3 an aberration? It’s a critical question given the labor shortage and all those voluntary quits/retirements that imply a rising labor cost basis reaching far out into the future.

The combination of inflation and a shrinking workforce is a toxic combination for future growth. At the lower wage levels, the workforce is recalcitrant and grumpy. It feels undervalued. You cannot live (or accumulate savings) at $15/hour or $31,200/year. Many websites offer data, by state, on what constitutes a “living wage.” The data is (oddly) mostly outdated but boils down to about $60,000 year. In other words, lower-wage level employees are making about half of what they need.

And on the other side of the job equation, employers report that labor costs are about 60% of total output costs (nonfarm). This means keeping wages down, whether workers can live on them or not. Hence the contentious labor union talks and numerous settlements of unfair labor practices suits at places like Amazon, which had to capitulate late last year and now pays $18/hour in starting wages. Multiplying, that’s $37,440, still short of the living wage. And Amazon may well be the leading edge–it did it once and it’s not doing it again.

Solutions include more immigration, the guaranteed basic minimum income, or some other state-sponsored handout. Neither is palatable in the current or foreseeable political environment (although the basic minimum income has some intriguing aspects). Another solution that is somehow managing to escape notice–flexibility. Plenty of people would take even low-paying jobs if they could tailor their hours to school hours and other personal issues. Employers don’t like flexibility–it complicates their spreadsheets. But the labor shortage could well get fixed to a great degree by flexibility. Maybe the government can give a tax credit to companies offering flexible hours.

Bundling all this together, we are hard-pressed to see inflation rising to 10% or more this year, as some scare-mongers project. One even has 15% (Saxo Bank). If that were to happen, it would be due to supply issues, not labor costs. And Apple has shown that intelligent planning and nimble logistics staff can overcome supply issues. That supermarket shelves are empty speaks to lousy management as much or more than to supply chain issues. If we assume supply chain issues get reduced by year-end–extended from the original June forecast–and labor markets do not get wild new wages so that labor costs are stable or at least not growing madly–then the basis for higher inflation fades away.

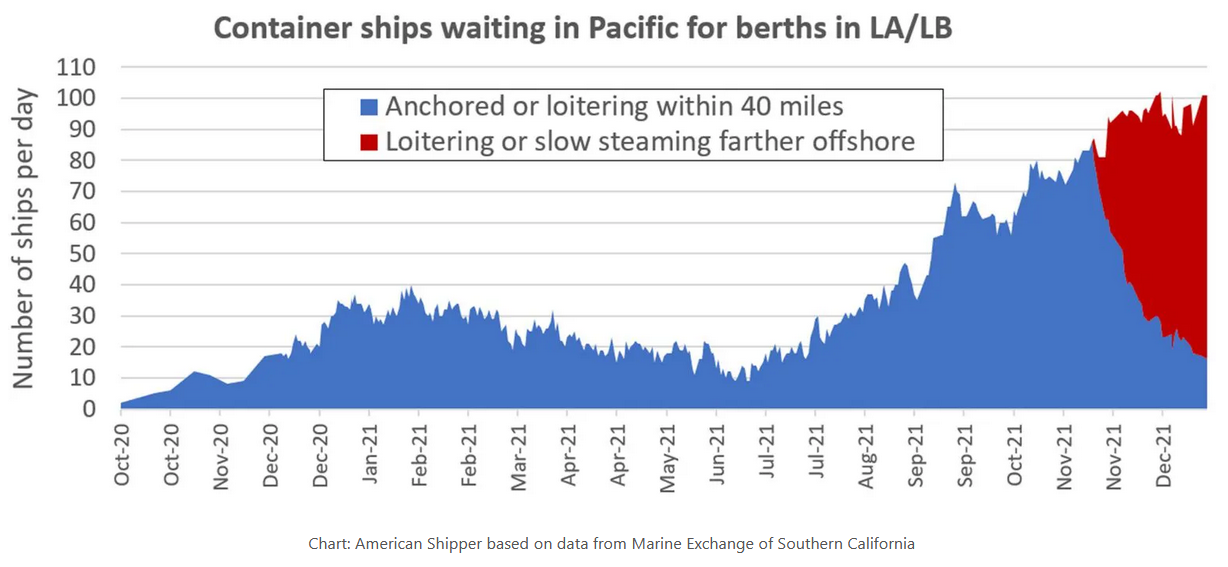

Okay, so if we can set inflation from labor costs aside, what about the supply constraints? Bloomberg comes to the rescue with multiple stories. On Friday, it offered a slew of data about the Port of Los Angeles, with import cargoes down 16% y/y in Dec and down 18% from Dec the year before. Exports were worse–down 41% y/y, the lowest since Oct 2002. Long Beach is almost as bad, with import volume down 12% y/y. These two ports handle 40% of the US’ inbound containers.

Bloomberg notes that the White House releases data twice a month but “always featured year-to-date changes, which in practice hide more recent monthly setbacks behind earlier gains. Combined import data from LA/LB confirm that last year’s record results were entirely driven by outperformance in the first half.”

Bloomberg directs the reader to the American Shipper website which contains data and charts from the NY Fed, which launched a new index on Jan 5. The charts will curl your hair. One we like affirms that the metric of ships waiting to unload has fallen dramatically because they moved farther offshore. This has been widely reported but see the chart!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat