Is the US already in recession?

- US economy will slow from the virus impact, how much is unknown.

- Very little March data has been released.

- China's return to production offers the best clues to recovery.

The answer, of course, is no if you use the traditional quarterly measurement. The Atlanta Fed GDPNow model for the first quarter, which as they say pointedly on their website, does not include data from after the viral outbreak, was running at 3.1% on March 18.

The real question is how has the economic trajectory changed since the Coronavirus became an acknowledged threat to the US and its economy?

Post-Corona economic statistics

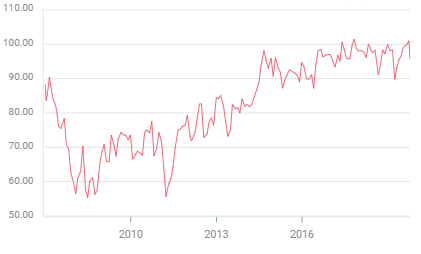

Very little data from this month has been released. The preliminary Michigan consumer sentiment index dropped to a historically healthy level of 95.9 from 101 in February.

Michigan Consumer centiment

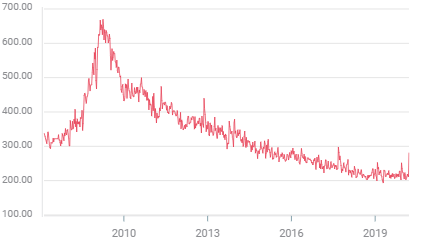

The initial jobless claims for the second week of the month soared to 281,000 from 211,000. It was the highest weekly total since early September 2017 and the largest one week jump since November 15th 2012. Initial claims numbers are released every Thursday at 8:30 am EDT for the previous week and will be watched closely.

Initial jobless claims

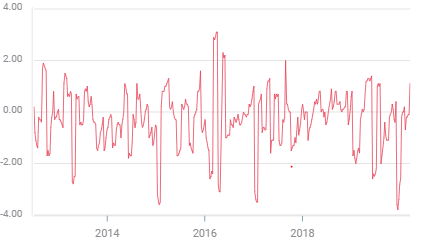

The Redbook Index which does a weekly track of year-over-year same store sales of large US general merchandise retailers representing about 80% of the retail sales figure from the Commerce Department, rose 1.1% in the week of March 13th after falling 0.1% the prior week. Could that be the early Corona stockpiling? Perhaps. The index for the week of March 20th is out on Tuesday the 24th and then on March 31st for the week of the 27th and so forth.

Redbook index

US economic data for March

Most March economic data will not be released until April. Here is a list of the most relevant for the current situation, all for March unless noted:

Tuesday March 24-- Richmond Fed manufacturing index, February -2, expected 9

Thursday March 26--Kansas Fed manufacturing activity index for March, February 8

Tuesday March 31-Chicago PMI, tracks business conditions in Illinois, Indians and Michigan, 49 in February; Conference Board consumer confidence for March

Wednesday April 1-ADP employment change, February 183,000; ISM manufacturing PMI, 50.1 in February, employment index 46.9, new orders 49.8

Thursday April 2—Challenger jobs cuts, February 56,660; initial jobless claims as above.

Friday April 3—Non-farm payrolls, February 273,000, Average hourly earnings y/y 3.0%, unemployment rate 3.5%, average weekly hours 34.4; ISM non-manufacturing PMI February 57.3, new orders 63.1, employment 55.6

Thursday April 9—Michigan consumer sentiment preliminary reading for April

Friday April 10—CPI, February 2.3%, core 2.4%

Wednesday April 15—Retail sales, February -0.5%, ex-autos -0.4%, control group 0%; industrial production February 0.6%; Fed Beige Book for conditions since the cancelled March 18th FOMC.

Tuesday April 16—Building permits, February -5.5%, housing starts February -1.5%; Philadelphia Fed Manufacturing Index for April

Thursday April 23-- Kansas Fed Manufacturing Activity for April

Friday April 24—Durable goods orders and capital goods for April

Wednesday April 29—Q1 preliminary GDP; FOMC meeting

Thursday April 30—Personal income, personal spending, PCE price index

By the end of next month markets will have a very good idea of the economic cost of the viral outbreak and a much better idea of the course of the infection itself.

Until the hard data on March begins we can make some sensible suppositions based on anecdotal information readily available.

Employment Impact

The widespread closures of many public venues, including restaurants and the abandonment of most travel plans has already led to reported layoffs and if the trend continues, many more will follow.

Some firms are hiring to meet increased demand, Amazon has announced it wants 100,000 new workers and shipping companies will likely follow, but these will not equal the job losses nor will they be geographically compatible.

Most furloughed workers will collect unemployment insurance which in the majority of states lasts for six months. Washington seems ready to supplement that with $1,000 to individuals and more for households.

Jobless benefits and government payments will not replace lost income and when unemployed the natural and understandable reaction is to curtail spending. If a good portion of the nation ends sheltering at home for a few weeks that will further erode consumption, particularly of big ticket items like automobiles which still tend to be bought in person.

Demand shock

Thought the extent and duration may be conjecture, it is plain that the consumer economy will suffer a substantial contraction. As US economic activity is about 70% consumption derived, that will certainly detract from the 3.1% pace the Atlanta Fed saw before the virus.

The longer the viral slowdown, the wider will be the layoffs and as more people lose their first-line income, the weaker aggregate consumer spending will become. It is this feedback loop that threatens business cash flow.

Business impact

Businesses large and small are preparing for the worst. Part of the collapse in equities and the briefer fall in bond prices was due to firms selling liquid assets in order to stockpile cash. With revenues for most companies certain to decline cash and credit lines will but necessary for continuing operations and fixed expenses.

A Wall Street Journal editorial on Thursday said that the largest economic concern is business liquidity, that is, cash flow and how to tide companies over until something like normality returns. In this they are right because whatever financial means are available to laid-off workers, consumption will decline, perhaps sharply and many firms will see a serious reduction in sales and income.

The government has already mentioned bailouts and loans for some of the hardest hit industries, airlines and travel, but much wider damage is likely to be incurred if the spending slowdown lasts more than a few weeks. Some form of small-business help will probably be needed as well.

Conclusion

An economic slowdown in the US and around the globe seems to be a certainty but its depth and length are highly speculative. It is not however speculation to say that the longer the Coronavirus reorders normal life the deeper the slowdown and the more difficult the recovery.

The speed and success with which China returns to economic life will provide the best clues for the rest of the world.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.