Inflation takes its toll

The Day So Far…

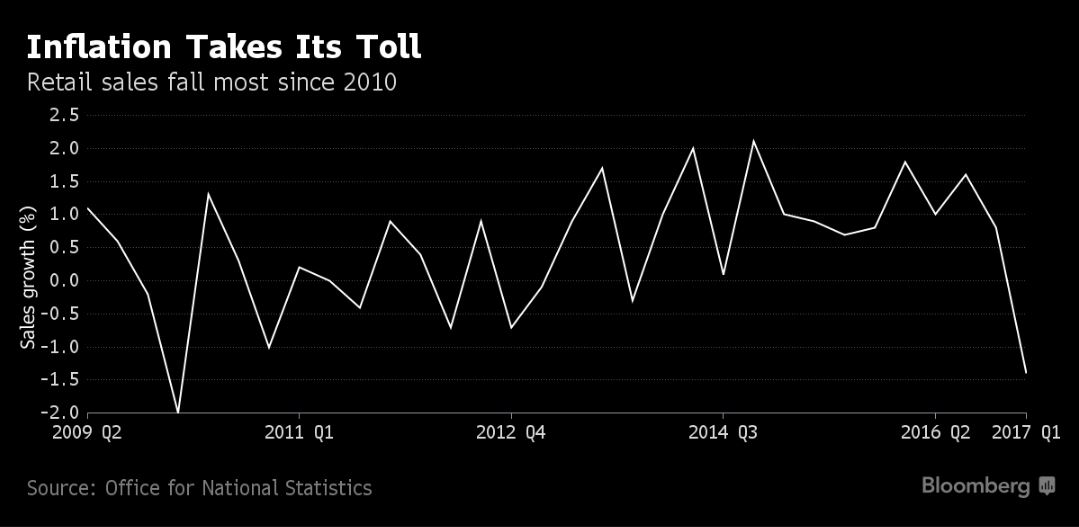

Divergence in economic data has been apparent this morning and despite the looming French election business activity in France remains solid at a fresh six-year high. This comes in comparison to a large miss in UK retail sales for the month of March which marked the biggest quarterly drop since early 2010. The UK numbers continue to reflect a theme we have often spoken about which is household incomes being further squeezed by a gradual but persistent rise in inflation. More worrying on this front is that the ONS said “it seems to be a consequence of price increases across a whole range of sectors”. In a broader context the timing of Theresa May’s call for a snap election seems all the more acute with the election likely to front run the higher bound of impending inflation, how quickly the average consumer starts to feel the pain may well be telling come the vote on the 8th of June.

Looking elsewhere, the market is now in wait-and-see mode for the results of the French election with results due on Sunday evening. I shall be delivering a full preview for the event later this afternoon at 3.30pm on Trading-Live.com so stay tuned for more.

The Day Ahead…

Something that has become increasingly apparent to me is that it is not only central bankers but also politicians that now seem to be fully aware of the ramifications their comments have on underlying market prices. None more so than from our friends across the pond, and after Wall Street failed to deliver its infamous late rally into the closing bell on Wednesday, it didn’t take long for the US Treasury Secretary Mnuchin to reverse tact from his weekend FT interview by now stating that the Trump administration is aiming to complete the biggest overhaul of the tax code since President Reagan by the end of 2017. This was also accompanied by some further noises on Capitol Hill on voting again on the repeal of Obamacare, while Fed member Jerome Powell hinted towards watering down of some financial regulations that were introduced post financial crisis. It is this combination of factors that keep me confident that buying the dips remains the more astute play in equities despite reports that fund mangers are increasingly seeing valuations as becoming ever more overstretched. Meanwhile, oil at the current level does not look particularly interesting but should the price break the triple bottom formed over the last three days then $50 looks enticing to re-enter a long position given the added protection that OPEC and non-OPEC names are likely to become more vocal on further productions cuts the lower the price becomes.

Author

Amplify Trading Team

Amplify

Amplify Trading is a proprietary trading company specialising in the development of new trading talent offering direct experience in financial markets.