Inflation might be in the way, but it's not here yet

Outlook:

We get jobless claims, the Empire State Fed survey, the Philly Fed and PPI today, plus industrial production and the home builders index. The Fed surveys are likely to show ongoing growth. We wonder if the capacity utilization component of the industrial production report will not get some attention. It should—it's one of the central variables the Fed looks at when contemplating the trajectory of inflation.

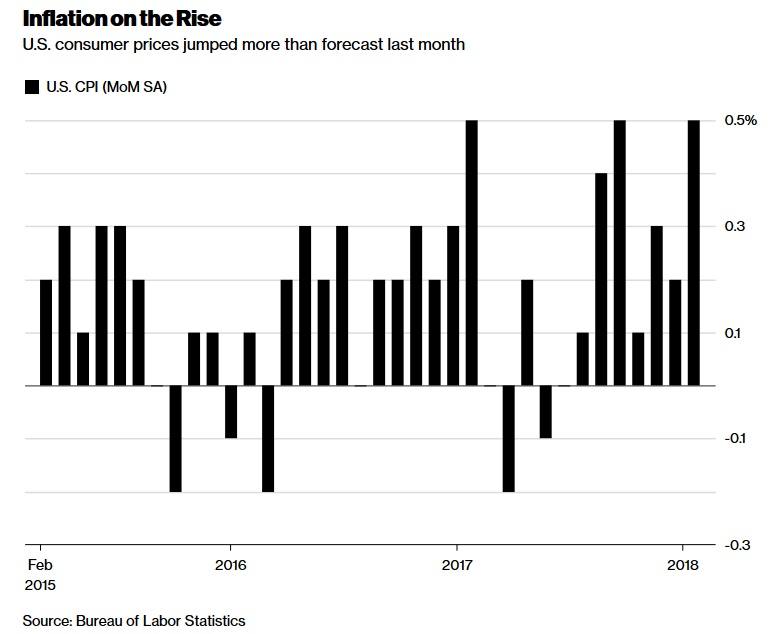

Bloomberg reports the outlook for inflation is perking up and bond traders are now betting on four hikes this year instead of three. Goldman Sachs Asset Management sees the 10-year yield hitting 3.5 percent within the next six months.

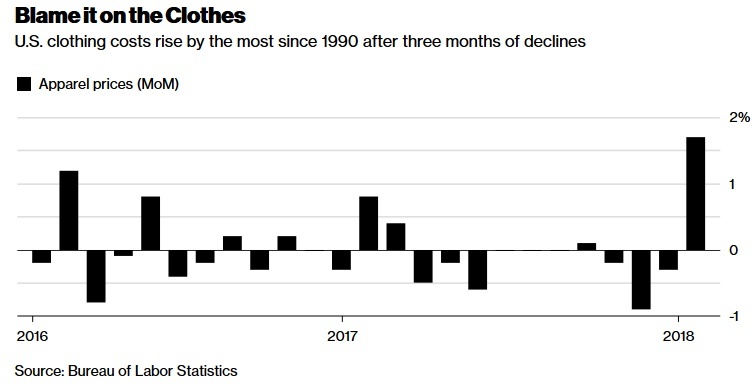

At a guess, this is another instance of overkill, although we have our own forecast of 3.25%. It's over-kill because for the Fed to go into full-blown hawkish mode, we will need more evidence. Just as we could debunk the hourly wages story with the weekly one, the CPI this time is flawed by... clothing. Apparel prices rose 1.7% m/m, the biggest one-month gain since 1990, with women's costs rising a record 3.4%.

Think about that for a minute. It's a record. Another word for record is aberration. Apparel accounts for well under 10% of household spending. Assuming female shoppers are rational, demand for apparel will fall and price normalize. Besides, apparel is only 3% of the CPI. And the retail sales report was pretty grim, showing sales fell in 7 of 13 categories. Both Morgan Stanley and JP Morgan told Bloomberg.

Without the boost from apparel, the core CPI would have advanced slightly less than 0.3 percent." In other words, apparel was the primary reason for the 0.5% reading. Without it, the overall would have been the same as the month before.

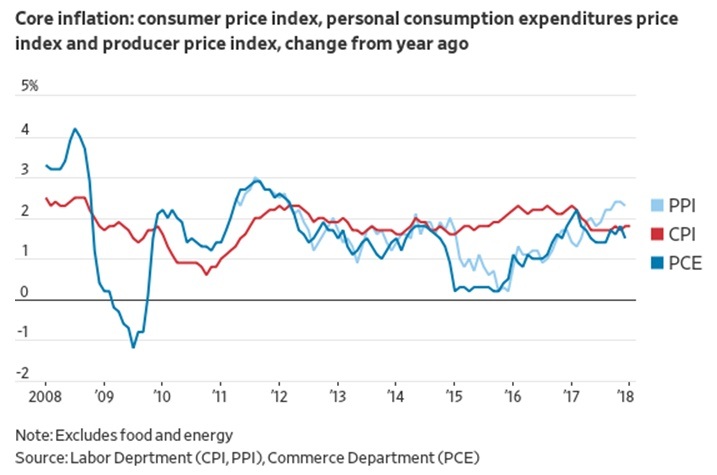

We may well be getting inflation, but it ain't here yet. The WSJ reports that PPI today "typically slips under the radar but it's worth watching as markets remain alert to signs the economy is overheating. Why? In part, because it feeds into the Fed's preferred inflation gauge, the price index for personal con-sumption expenditures. That's where the central bank targets 2%. So far, it looks like PCE is only inch-ing closer, with some forecasters expecting a roughly 1.5% year over year gain for core prices in Janu-ary (the actual numbers are due out March 1). If inflation advances at a manageable pace, Fed officials are less likely to have to deviate wildly from plans to raise rates three, or perhaps four, times this year."

That's more like it. See the chart. There is nothing here to set your hair on fire. And a little inflation is actually good news. It means the likelihood of recession is lower. It means the Fed is on the correct policy track and we don't have to accuse it of being behind the curve or too far ahead of it. A modicum of inflation is actually good for consumer as well as business sentiment, history tells us. We should be dancing in the streets instead of cowering in the corner.

We think inflation will remain lower for longer than both the rhetoric and the yields are now suggest-ing. If sentiment toward the dollar remains in the same negative territory, whether because of the twin deficits or the incompetent president or any other reason, a drop in inflation in coming periods could be even more dollar-negative.

Having said that, we need to worry about the dollar falling so much for so long. As some point that yield differential has to bite into negative sentiment, usually at around the same time trader positions are over-extended short. The WSJ reports the COT has it that dollar shorts are $13 billion. Even a par-tial reversal of that sum can move the market hard and fast.

A dollar bounce is not out of the question over the next week, when we will be out of the office. One analyst notes (WSJ) that the St. Louis Fed shows the dollar still overvalued by about 5% on a trade-weighted basis, even after last year's near-10% drop. We say traders hardly ever look at the St. Louis Fed. We favor a short dollar position anyway, but beware a hawkish statement from Fed chief Powell or some other Big Shot. The antidote may be another statement favoring a weak dollar from the clue-less Treasury Secretary or the president.

Political Tidbit: The current occupants of the White House are disclosed as liars, again, and not even good liars. Testimony from the FBI shows they knew perfectly well that the staff secretary was a wife beater last July and declined to boot him out. The White House pretends some imaginary staff security department was not through researching the issue. The chief of staff may be on the way out. The bigger issue is the dozens of Trump staffers who don't have and can't get a proper security clearance, includ-ing the president's daughter and son-in-law, who are unqualified to hold any job in government in the first place. The hypocrisy is stunning of a president who attacked Clinton for carelessness about secure emails.

The gutless Congress is doing nothing about it, and also doing nothing about the Executive failing to order any investigation or action into Russian meddling in US elections, including the midterms com-ing up in the fall. The FBI is beavering along on its own. The Trump White House is also not enforcing the last set of sanctions ordered by Congress and signed by Obama, basically giving Mr. Putin what he wanted. He didn't need Flynn or Manafort. One Trump supporter said on TV that Congress wrote the sanctions law badly, failing to include the measures that would have forced the Executive to imple-ment. The meanness is obscene. The lack of patriotism, too. It has come to this.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes. To see the full report and the traders’ advisories, sign up for a free trial now!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat