Increased speed makes a soft landing more difficult

We still expect the economy to expand, albeit slowly, over the next two years. While a recession is not in our baseline forecast, the odds of a sustained economic downturn by the end of next year have climbed to roughly 40% in our estimation.

There is little good news on the inflation front. The recent surge in energy prices puts gasoline prices at record highs, and we have taken up our near-term inflation numbers accordingly.

It has been clear for months that monetary policy would be less accommodative, but as inflation in recent months has soared to levels not seen in 40+ years, so too have expectations about the intensity of the needed response from FOMC policymakers to get prices in check.

Specifically, we expect the Fed to raise the federal funds rate by 50 bps at each of the June, July and September FOMC meetings. We then expect five more 25 bps rate hikes over the course of the next two years, with the fed funds rate rising to 3.50%-3.75% in Q2-2023.

Consumer spending has picked up speed in each of the past two quarters, and we suspect Q2 will see yet another increase in the pace of personal outlays. But because of higher inflation and some unsustainable drivers behind recent consumer resilience, we see a sharp slowing in consumer spending toward year-end.

While a sharp downturn cannot be dismissed out-of-hand, it is difficult for the economy to slip into recession when more than 96% of the people who want a job have one. We expect the unemployment rate to fall to 3.4% by Q4-2022. A slower pace of job growth and increased labor force participation are likely to lead the unemployment rate to rise slightly in the back half of 2023.

The outlook for capital spending remains a relative bright spot. We look for business investment to expand 5.3% in 2022 and 4.0% in 2023.

One area where the Fed’s rate increases have already had a meaningful impact is in the housing market. The sharp pullback in both new and existing home sales has led us to reduce our residential investment forecast to an 8.5% decline in Q2-2022 and another decline in Q3.

Seats in the upright and locked position

It is a time of superlatives. A student of financial markets would usually have to wait decades to witness the highs and lows seen in recent weeks and months. Start with inflation and employment, which are paramount for policymakers at the Federal Reserve. As of this writing, the urgency to address inflation is underscored by the price of a gallon of unleaded gasoline in the United States costing $4.92/gallon, an all-time high. Even after excluding volatile food and energy prices, the core PCE deflator rose to 5.2% on a year-over-year basis in March, the fastest inflation rate for the Federal Reserve’s preferred inflation gauge since 1982. The core PCE deflator cooled slightly to come in at 4.9% in April. While it may be true that core inflation has cooled, the peak in headline inflation no longer looks like it is behind us. In light of the higher prices for energy and energy services, we have lifted the profile of our inflation forecast such that headline measures of inflation like the PCE deflator and the Consumer Price Index now both peak in the third quarter of this year. We expect headline inflation to fall in 2023 as this year’s energy prices set up a tough base for year-over-year measures. Yet, we suspect that even by the end of our forecast period in Q4-2023, the core rate of inflation will still be at 2.9%, which is above the Fed’s 2.0% target (Figure 1).

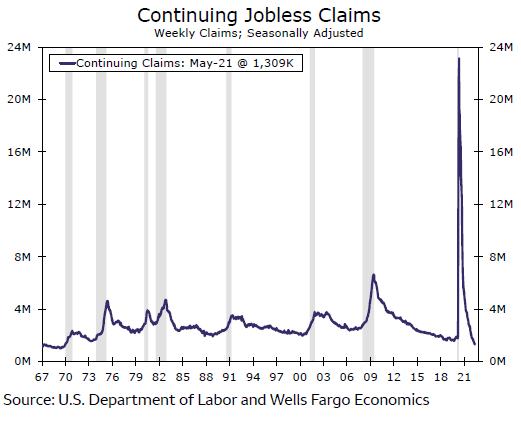

Turning now to the other side of the Fed’s dual mandate, we find that the unemployment rate at 3.6% is just a tick away from 3.5%, which would be the lowest on record going back more than 50 years to the late 1960s. The strength of the job market has pulled people off the unemployment line to a degree not seen in more than a half century. In the most current data available for the week of May 21, continuing claims for unemployment insurance fell to their lowest level since the 1960s (Figure 2). These numbers corroborate survey data in recent months, which showed a record share of consumers seeing jobs as being plentiful and a record-high share of small businesses which report that open positions are hard to fill.

The historically strong labor market is an anchor to the windward for our call that the economy can avoid recession over the next year and a half. Unfortunately, the downside of a strong labor market is that the FOMC can proceed with its widely telegraphed plans for rate hikes and balance sheet normalization to get inflation in check. That helps explain the negative reaction in financial markets to a better-than-expected May jobs report last week.

In terms of specifics for the Fed outlook, we look for the FOMC to hike the fed funds rate by 50 bps at each of its meetings in June, July and September. After that, we anticipate five more 25 bps rate hikes, with the target range for the fed funds rate reaching 3.50%-3.75% in Q2-2023 and remaining at that level throughout the rest of next year.

Author

Wells Fargo Research Team

Wells Fargo