How will the Fed react to the US CPI release?

Outlook:

We await the inflation numbers at 8:30 am ET to determine whether yields and the dollar go up and the stock market down on a hot print, or the financial world returns to sanity on a normal set of numbers, in this case lower than the month before, which is the consensus forecast.

Jan core inflation is expected to come in at 0.2% or 1.7% y/y, less than December, meaning the Fed is on the same track as before the inflation hype began. The hype began when hourly wages came in at 2.9%, inspiring the exaggerated equity market response. As we wrote at the time, the hourly wages number embodied a false narrative. On the weekly basis, wages rose 2¢.

The key to the exaggerated response is an assumption about the Fed's behavior. Even if inflation were to rise a little, that doesn't mean the Fed will have a panic attack and start hiking rates willy-nilly, like 50 bp in March instead of 25 bp or a faster pace of hikes this year or four instead of three hikes. Those promoting a frightening rise in inflation (and what is their self-interest in doing so?) are making unwar-ranted assumptions about how central banks behave when faced with strong data. What would be the core CPI have to be to incite the Fed to 50 bp in March, or any of the other scare-scenarios? Whatever it is, it's improbable in the extreme.

That doesn't mean we are not in for inflation and hikes this year. The Fed itself projects three hikes starting at the March meeting, and perhaps four if the economy heats up. Inflation may rise from higher consumer and capital spending because of tax cuts, and perhaps a little pressure against capacity if in-frastructure spending ever does come to pass.

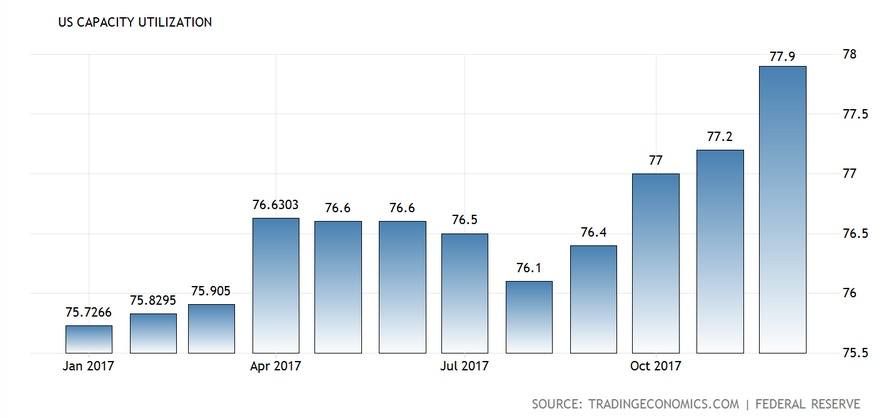

It's not enough to know that capacity utilization is on the rise. We would need to know how much spare capacity there is in sectors like building material, cement and rebar. See the chart from tradingec-onomics.com, which reports capacity utilization in the United States jumped to 77.90% in December from 77.20 percent in November. The average is 80.31% from 1967 to 2017, with the all-time high at 89.40% in Jan 1967 and a record low of 66.70 percent in June of 2009.

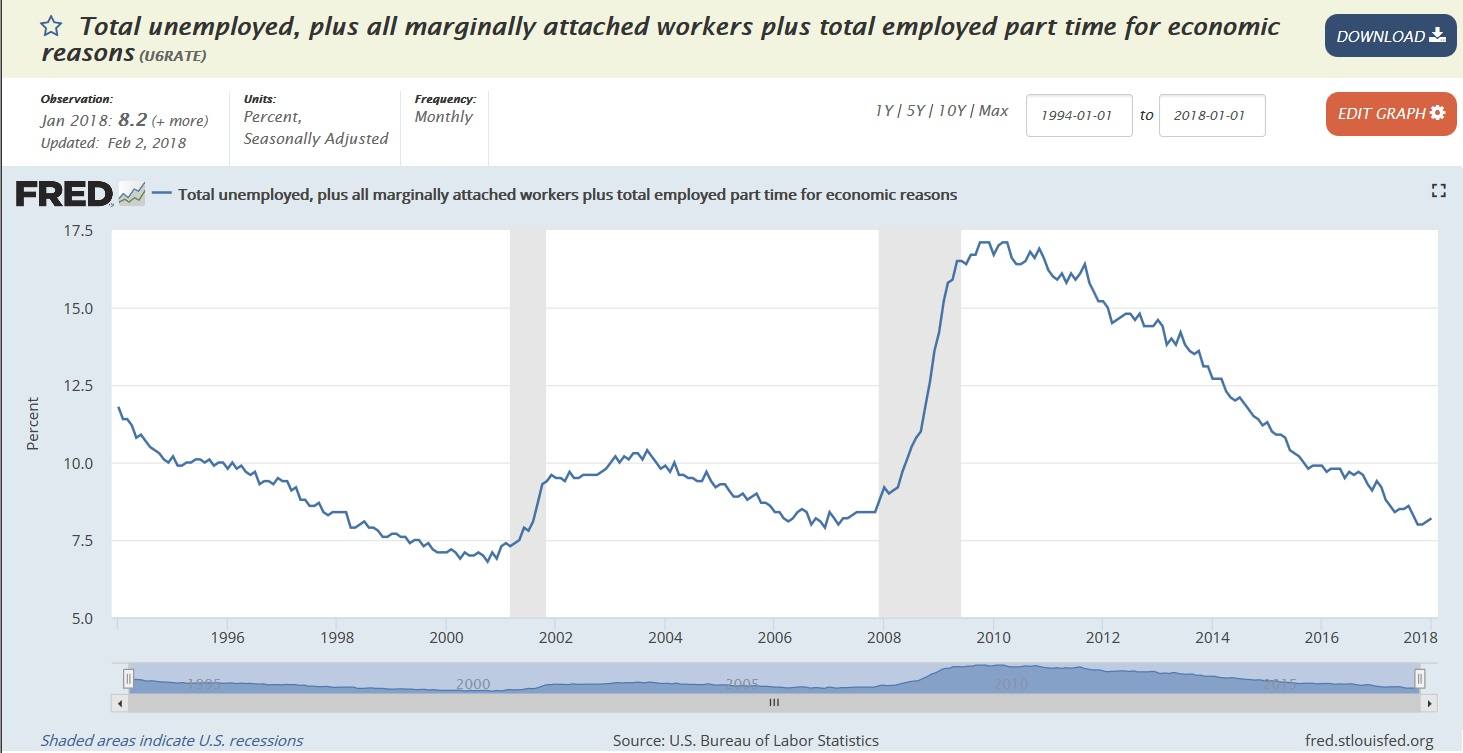

As for there not being enough construction workers to renovate airports and bridges, bah. We don't believe the unemployment rate at under 5% for a minute. The supply of labor that can be induced to return to the workforce numbers of the millions. The U6 unemployment rate at 8.2% is better than be-fore, but still leaves millions available, if only conditions, including wages, were attractive. The process of getting labor back to work is stop-and-start, though. If bosses think acting like Trump is a successful strategy, we will indeed get a "labor shortage" that would take exceptional wage gains to overcome. People do not work for money alone.

So, if it's not inflation that should worry the Fed, at least not yet, what does it means that yesterday new Fed chief Powell said "the Fed is on alert to any risks to financial stability"? We guess it does NOT mean that if VIX goes through the roof and the stock market rout resumes that the Fed would cut rates. It may mean that in its role as regulator, the Fed is scanning financial institutions for any signs of the risk of failure a la Lehman and Bear Stearns.

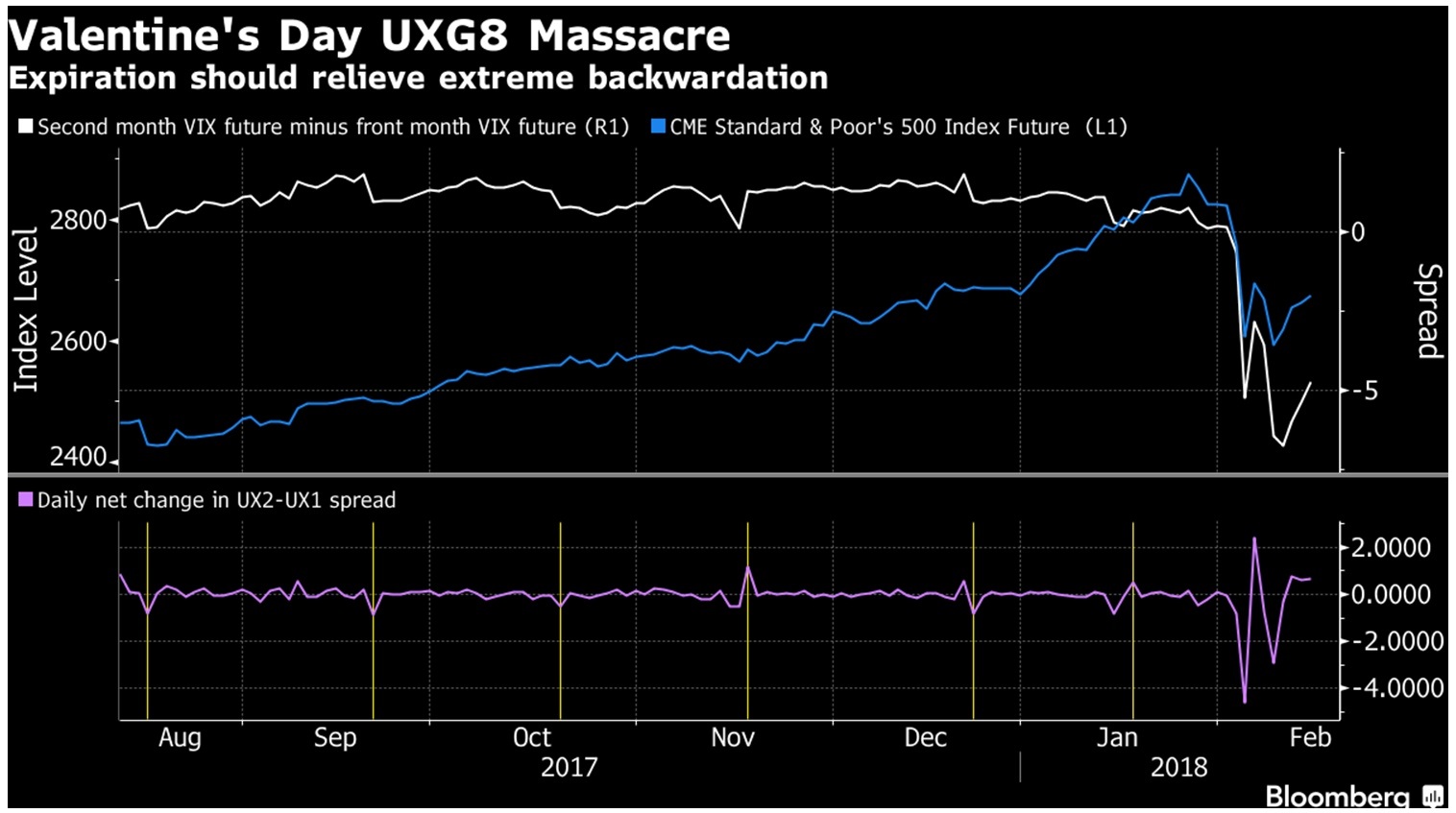

Or the Fed might be worried about abnormal behavior in the market itself. Bloomberg has a story about weird goings-on in the VIX futures contracts. The Feb contract expires this morning and March be-comes the front-month. Futures contract converge with the underlying at or near expiration, as we see in FX futures every quarter. This time, the spread between the Feb and March contracts is an abnormal-ly big 5 points (March to April is a normal <1 point). "But there's little to think the easing in the ex-treme backwardation will be matched by an improvement in stock prices. In other words, there's good reason to believe the fairly tight relationship between the S&P 500 active contract and the spread be-tween the front two-month VIX futures (the top panel in the chart) will expire along with UXG8. Any narrative that the tail is wagging the dog should also reach its best-before date today, as well."

We can only dimly grasp what Bloomberg is talking about, but if we have it right, traders in the VIX futures contract had a nervous breakdown. This implies they are amateurs or easily frightened. The Bloomberg reporters thinks it will all be over today after the Feb futures contract expires, but we are not so sure. Once bitten, twice shy. So then the question becomes whether this contract should be more tightly regulated with higher margins, or something. The point is probably that the tail wagging the dog is actually quite common in all aspects of trading life and if a gaggle of market participants has already shown a propensity to panic, we might be foolish to think they don't do it again.

The WSJ reports "The Cboe Volatility Index, known as the VIX, is derived from S&P 500 options pric-es. The Financial Industry Regulatory Authority is scrutinizing whether traders placed bets on S&P 500 options to influence prices for VIX futures, according to people familiar with the matter. Earlier in the week, a letter from a law firm representing an unidentified client urged U.S. regulators to investigate VIX manipulation, claiming it has cost investors hundreds of millions of dollars in losses each month. A probe would be another setback for Cboe Global Markets, which owns the VIX index. The resur-gence of volatility last week triggered a spike in the VIX and the collapse of a widely traded ETP that buys and sells VIX futures, sending Cboe's shares sliding."

We should care about volatility because now that we have had a "crash," the propensity to additional panics and crashes is baked in to the mentality of market players and not just in one futures contract, but across a broad spectrum of securities. The linchpin is the degree of surprise of the actual vs. the forecast, just as we see in the response to the nonfarm payrolls report. Eeek. Those spikey responses are abnormal and arise ONLY in response to that one data set. No other economic variable has the same juice. But as we see in the payrolls response, spikes, aka volatility, can arise from a positive surprise or a negative surprise equally. This time, in the case of inflation, let's assume the numbers are as forecast and Jan shows less inflation than Dec. The scaredy-cats can assume inflation is still lurking in the bush-es and will appear next time, or the time after that.

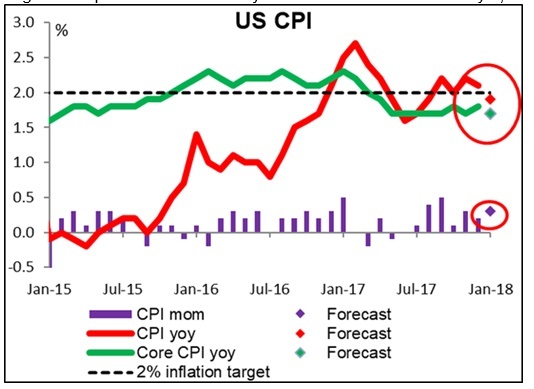

The inflation chart is from ACLS. Never mind that actuals are near the 2% Fed target line. Market players can behave as though the big rise in the year-over-year CPI (red line) will resume—and resume it probably will as the dip during 2017 gets reflected in the upcoming year-over-year. Lies, damned lies and statistics. We must take great care to keep our wits about us as fresh inflation data starts coming in. A market prone to panic can always find an excuse, even if the excuse is based on a bad understanding of statistics. And this nonsense can and will spill over to increased volatility in the FX market, which is good news for fast-finger scalpers but bad news for trend followers.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes. To see the full report and the traders’ advisories, sign up for a free trial now!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat