Have the trade agreements ended the US manufacturing recession?

- New York and Philadelphia manufacturing indexes rise sharply in February.

- Nationwide factory PMI returned to expansion in January.

- Factory employment lags the overall improvement.

- US-China and USMCA pacts expected to boost American manufacturing.

The first signs are emerging that the US manufacturing recession may be at an end if the results of three recent business surveys recent pan out.

Reports from the Philadelphia and New York Federal Reserve districts indicate a much stronger recovery in February than expected and they follow on the national figures for January that moved into expansion for the first time since last August.

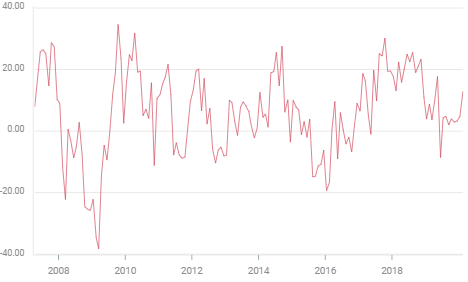

The New York Fed’s Empire State Manufacturing Survey jumped to 12.9 in February from 4.8 in January, nearly doubling the 7.9 forecast. It was the best reading for this index since May. New orders surged to 22.1, the best since September 2017 and shipments climbed to 18.9, the highest since November 2018.

New York Fed Manufacturing Survey

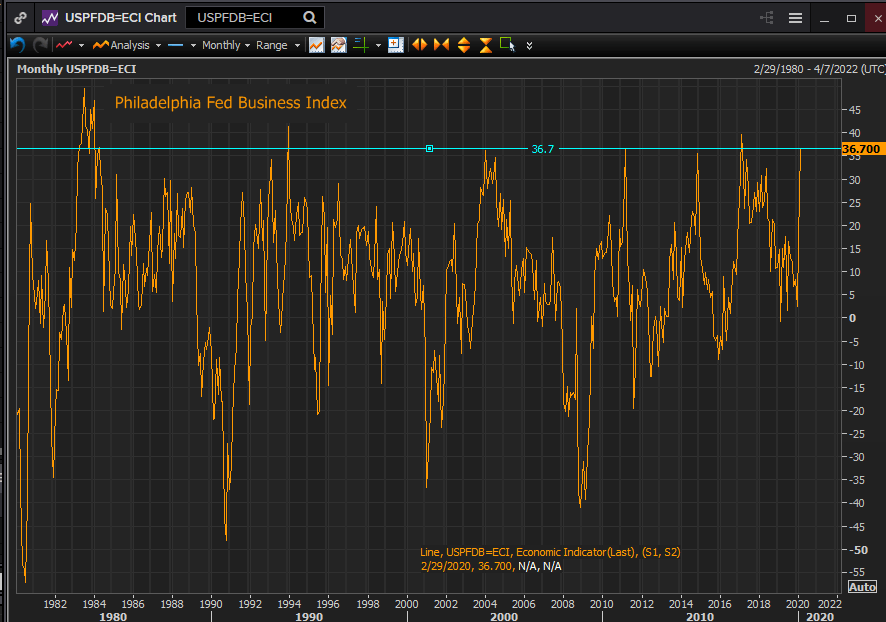

On Thursday the Philadelphia Fed Business Survey rocketed to 36.7 in February, well above both consensus prediction of 12 and the January score of 17. It was the highest for this gauge since February 2017 and the second best level in 27 years.

Reuters

The new orders index soared from 18.2 in January to 33.6 in February, its highest since May 2018. This measure has more than trippled in three months from 11.1 in December.

Reuters

In the first week of the month the nationwide purchasing managers’ index from the Institute for Supply Management registered 50.9 in January up from 47.8 the prior month, easily beating the 48.5 prediction. It was the first month over the 50 expansion-contraction demarcation since August. The new orders index lifted to 52 from 47.6, the first expansive month in six.

Employment indexes for the three surveys showed little change but with the overall labor market in fine shape and hiring stable factory work can be expected to follow the indexes higher in the months ahead. Manufacturing lost 12,000 jobs in January despite the addition of 225,000. In any recovery employment is generally the last to improve.

Manufacturing had slipped into contraction in the second half of 2019 as the US-China trade war reached its height damaging export orders, sentiment and employment prospects. The conflict also brought on concerns that the factory sector might point the way to a general recession.

Though manufacturing is only 12%-15% of US GDP, it has long been considered a leading indicator for the overall economic activity.

The US-China trade agreement signed on January 15th and the newly constituted United States, Mexico, Canada Agreement, (USMCA) have reduced the uncertainty of the trade outlook and are expected to return the US manufacturing sector to the growth it enjoyed in 2017 and 2018. One caveat is the still unknown extent of the impact on mainland growth of China’s health crisis.

The indexes are percentages of the companies expecting expansion or contraction in the specific areas questioned.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.