Hard Brexit will not end well for the United Kingdom

Outlook:

Yesterday's CPI is described variously as "upbeat," "modest" or "tepid." The lack of consensus is reflected in various outcomes. Note yields fell and the dollar along with them, but gold is higher. Bottom line, nobody knows what the data means, if anything. The CPI failed to tweak the CME rate hike probability chart, which may be the key.

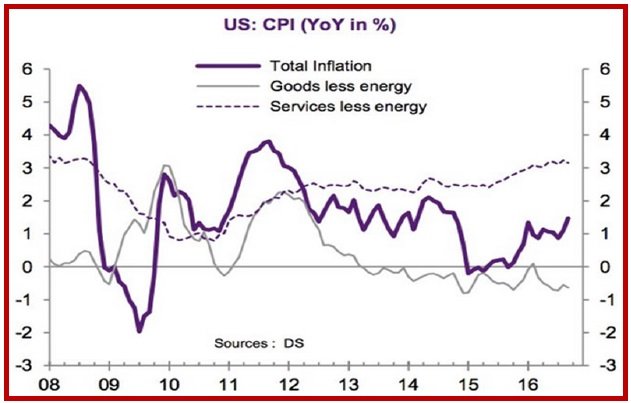

CPI was 1.5% y/y, the highest since Oct 2014 after 1.1% in Aug. Inflation was led by gasoline and rents, two things the Fed doesn't care about too much. There is some controversy over how to interpret the CPI—it's accelerating at the fastest pace in nearly two years but still well under the Fed's 2% target, and besides, the Fed doesn't look at CPI. The PCE version is likes is up 1% and the core, 1.9%. Maybe it's core CPI disappointing at 2.21% when 2.3% was forecast. The Daily Shot notes the inflation in services prices is outpacing inflation elsewhere. See the chart.

Talk of inflation being the shiny new thing—buy commodities!—is premature. Except in the UK. We can expect nothing but worsening inflation and the usual fall-out from it across the pond. As noted yes-terday, the press is dressing up the disconnect between sterling and bonds as a function of something unaccustomed—political risk. The prospect of a hard Brexit, in which the UK gets no trade concessions from the EU in exchange for sovereign control over immigration, is thought to be the May government's preferred stance.

May has made comments along those lines but in practice, we don't actually know the government's stance. It has never been disclosed and indeed, we have to get over the court case first. No one ventures a guess on when the court will rule. For all we know, speaking of hard Brexit is a ploy to whip the pub-lic into line for a less draconian deal or to confuse the opposition—in other words, a bluff.

All the same, it's rare for the currency and note yield to fall in lockstep. Analysts are competing with one another for the scariest FX forecast scenario. The WSJ notes the BNP Paribas model shows ster-ling undervalued and oversold-–so-called fair value would be about $1.40. But yesterday Goldman Sachs said Brexit is a "structural break" and can fall another 40%, which we reckon would take it to 0.7380 off this morning's 6:15 am ET quote. Brown Brothers' Chandler doesn't rule out parity on the "existential crisis."

We are always leery of a so-called "paradigm shift." The rules of finance don't vanish in a puff of smoke because of a seemingly new factor. There will come a time, after the dust has settled, when the currency and yields will return to normal behavior. A drop in the currency on inflation expectations will be offset, at least somewhat, by a rise in yields. A hard Brexit will indeed lower UK growth for such a long time that it may as well be considered permanent, and that weighs on the currency, too. The problem is that we lack a model. Brexit is literally a one-off Event. We had political risk in the eu-ro during the Grexit crisis and it did force European yields upward, but the euro was remarkably resili-ent. We recall complaining about it. See the chart showing the euro/dollar against the 2-year and 10-year yield differential. The euro started falling on the financial crisis in 2008 and actually rose in 2011, led by the 2-year, before resuming the decline. It rose in 2013 and 2014 despite yields continuing to fall.

But that was political risk without a specific economic variable involvement. The strict (if not obses-sive) anti-inflation ECB stance never wavered. The rules of fiscal austerity wavered but only a little and only in a few cases. Spain, faced with a loss of sovereignty that was the price of a bailout, decided it could do austerity, after all. At the time, uncertainty over Grexit spawned a number of issues, including what authority the ECB had or didn't have, pan-European banking supervision, and a bunch of other things we have now forgotten.

The Brexit case has its own mind-numbing ramifications and implications, but is actually simpler, hark-ing back to Econ 101. If the UK fails to get trade concessions and special consideration for the financial sector, the UK economy will shrink. The loss of confidence in the May government and in the BoE's anti-inflation mood will push sterling down further in what some are calling a Big Short. The BoE is willing to take 2.5% inflation but private forecasters are seeing 3.5%. It's not at all clear that the gov-ernment has Plan B and Plan C, let alone Plan A.

The probability is high that this will not end well for the UK. We get the odd comment or two from the edges of the summit but life is too short to parse them all. Suffice it to say, preventing any other country from exiting the EU is working quite well as motivation for Europeans to take a hard line. The combination of worsening economic data sure to come, especially inflation, and the government's unwillingness to spill the beans, spells a one-way street for sterling. The current corrective upmove has one leg—the pound had been oversold. One leg doesn't hold up the stool.

We have a similar amount of uncertainty about the dollar, albeit with less world-shattering implications. The market is still not sure of the Dec hike. Inflation is on the rise but not enough to set your pants on fire. The election offers political risk of a staggering amount. China is almost certainly lying about its data and can still blow up. And in whom does the world have some actual confidence? One guy—Draghi. If confidence in institutions were the only factor out there, you'd have to bet on the euro.

US Politics: The third and last presidential debate is being held tonight. It will be an ordeal to watch. Trump is likely to stick to insults and charges of rigging rather than the few policy ideas he actu-ally has, some of which would have broad appeal (tax reform, immigration reform, and the latest, lob-bying reform). All Clinton has to do is get under his skin to set him off on his usual incoherence.

The press has done a fine job of rebutting Trump's assertion that the election is rigged—historically, fewer than 40 proven cases in over a billion votes cast. But the nitwits who support Trump persist in accepting his lies as truth, as well as physically attacking reporters at Trump events because of their so-called bias. Funny, Trump is biting the hand that feeds him—he got over $3 billion in free media cover-age. Yesterday Pres Obama told him to stop blaming others for not winning and go out and get votes.

Trump has yet to say he will accept the outcome of the vote, a basic requirement. Trumpian thugs will be "monitoring" polling places (of which there are over 6000), another word for intimidation. Maddow had a hilarious if scary piece on two Black Panthers at a polling place in 2008 for a single hour being blown up way out of proportion as "vote rigging" by Trumpies in places like Alaska (no Black Panthers to be found there).

And Ecuador temporarily suspended Wikileak' internet access in the London embassy to avoid being charged with interfering in the electoral process in the US (over the leak of hacked emails of the Clinton campaign manager Podesta). The statement says "The government of Ecuador respects the principle of nonintervention in the affairs of other countries," it said in a statement, "and it does not interfere in the electoral processes in support of any candidate in particular." But Ecuador is not evicting Assange, either. Heaven only knows what "proportionate" retaliation the US is taking against Russia, the source of the email leaks. VP Biden told an interviewer the public will likely never find out what it is. As of this morning, the most-respected pollster, 538, has Clinton with a 87.4% probability of winning and Trump with 12.6%. But don't break out the champagne until Nov 9.

| Current | Signal | Signal | Signal | |||

| Currency | Spot | Position | Strength | Date | Rate | Gain/Loss |

| USD/JPY | 103.31 | LONG USD | WEAK | 10/06/16 | 103.50 | -0.18% |

| GBP/USD | 1.2295 | SHORT GBP | STRONG | 09/10/16 | 1.3041 | 5.72% |

| EUR/USD | 1.0999 | SHORT EUR | STRONG | 09/19/16 | 1.1168 | 5.72% |

| EUR/JPY | 113.63 | LONG EURO | WEAK | 10/06/16 | 115.78 | -1.86% |

| EUR/GBP | 0.8945 | LONG EURO | WEAK | 09/19/16 | 0.8564 | 4.45% |

| USD/CHF | 0.9881 | LONG USD | STRONG | 09/19/16 | 0.9804 | 0.79% |

| USD/CAD | 1.3090 | LONG USD | STRONG | 09/15/16 | 1.3203 | -0.86% |

| NZD/USD | 0.7208 | SHORT NZD | STRONG | 09/19/16 | 0.7305 | 1.33% |

| AUD/USD | 0.7682 | SHORT AUD | STRONG | 09/24/16 | 0.7618 | -0.84% |

| AUD/JPY | 79.37 | LONG AUD | STRONG | 10/06/16 | 78.48 | 1.13% |

| USD/MXN | 18.6176 | LONG USD | STRONG | 05/06/16 | 17.9418 | 3.77% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat