Greenback slightly weaker after the data

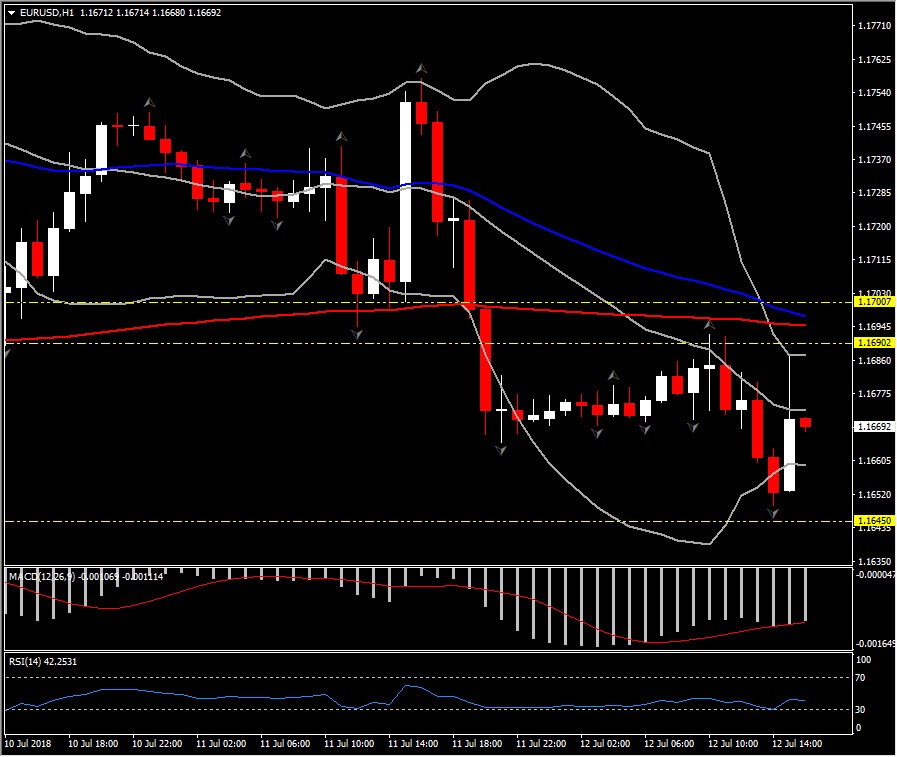

EURUSD,H1

The Dollar moved slightly lower after the cooler headline CPI and lower jobless claims results. EURUSD rallied to 1.1688 from near 1.1660 as USDJPY slipped to 112.39 from 112.48. Equity Futures continue to indicate a higher Wall Street open, while Yields firmed a bit.

EURUSD continues to remain in a broadly consolidative phase, which has been unfolding for over a month now, following a 6-week down phase from levels above 1.2400. The range over this period has been 1.1508 to 1.1851.More of the same looks likely for now, though strong US Economic growth and the Fed’s tightening course tip the fundamental balance in favour of the Dollar, and so the downside of EURUSD. Any move from Trump to follow-through on hits threats to tariff car imports would also be negative for the Euro relative to the Dollar. EURUSD has intraday Support is at 1.1645-47. Resistance comes at 1.1690- 1.1700.

The 18k Initial Claims drop to 214k in the first week of July more than reversed the 4k rise to 232k (was 231k) from 228k in the prior week and 218k in the June BLS survey week, as the figures are almost exactly tracking the June rise and ensuing July drop we expected with auto retooling. Claims remain above the 48-year low of 209k seen in late-April, though we assume a modest underlying downtrend that will keep new multi-decade lows in reach. Claims are entering July below recent averages of 225k in June, 223k in May, 221k in April, and 228k in March. Next week’s BLS survey week reading should sit near recent readings of 218k in June, 223k in May, 233k in April, and 227k in March.

Meanwhile, US headline CPI rose 0.1% in June with the core rate 0.2% higher, less than feared after the jump in PPI yesterday. There were no revisions to May’s 0.2% gains overall and for the ex-food and energy component. The 12-month paces sped up with the headline rate rising to 2.9% y/y versus 2.8% y/y, matching the highest since February 2012. The core rate rose to a 2.3% y/y clip from 2.2% y/y. That matches the firmest since January 2017.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in