Global Stocks Slide as The US Threatens More Sanctions on Turkey

World stocks declined today as the Turkish crisis continued. Yesterday, the United States government announced that a new set of sanctions on Turkey were ready if the country failed to release an American pastor. The Turkish Lira fell by more than 6%. In response, Europe’s Stoxx and Germany’s DAX fell by more than 50 basis points. US futures too pointed to a lower open following disappointing result from chip makers.

The euro was little moved after the European Union released the consumer price index (CPI) data. In July, consumer prices held at an annualized rate of 2.1% and at a monthly rate of minus 0.3%. This contraction was in line with expectations. In June, consumer prices rose by 0.1%. The core CPI rose by an annual rate of 1.1%, which was in line with expectations. Monthly, the CPI fell by minus 0.5%. The region’s current account rose to 23.5 billion euros, which was better than the expected 23.2 billion euros.

The Nasdaq futures declined after a weak performance by NVIDIA, one of the fastest growing chip and GPU manufacturers. The company announced better-than-expected quarterly results. The revenues and EPS for the quarter were $3.2 billion and $1.76. This was a growth of 40% and 91% growth respectively. The stock’s decline was mostly because of the weak guidance the company offered. The weak guidance by the company sent shockwaves among the chip investors who worried that the industry had peaked. Intel, Qualcomm, and other chip manufacturers’ stocks declined too. On stocks, the US president announced through Twitter that he will lobby the SEC to end quarterly earnings, which has been blamed for the short-sightedness of managers.

The Canadian dollar strengthened against the US dollar after the statistics office released better-than-expected CPI for the month of July. The numbers showed that the core CPI rose by 1.6%, which was better than the expected 1.3%. Monthly, the core CPI rose by 0.5%, which was better than the expected 0.1%. The general CPI rose by an annual rate of 3.0%, which was higher than the expected 2.5%. In June, foreign securities purchases rose to C$11.55 billion, an indication of the bullishness by global investors. In the same month, Canadian investors bought stocks worth C$11.29 billion.

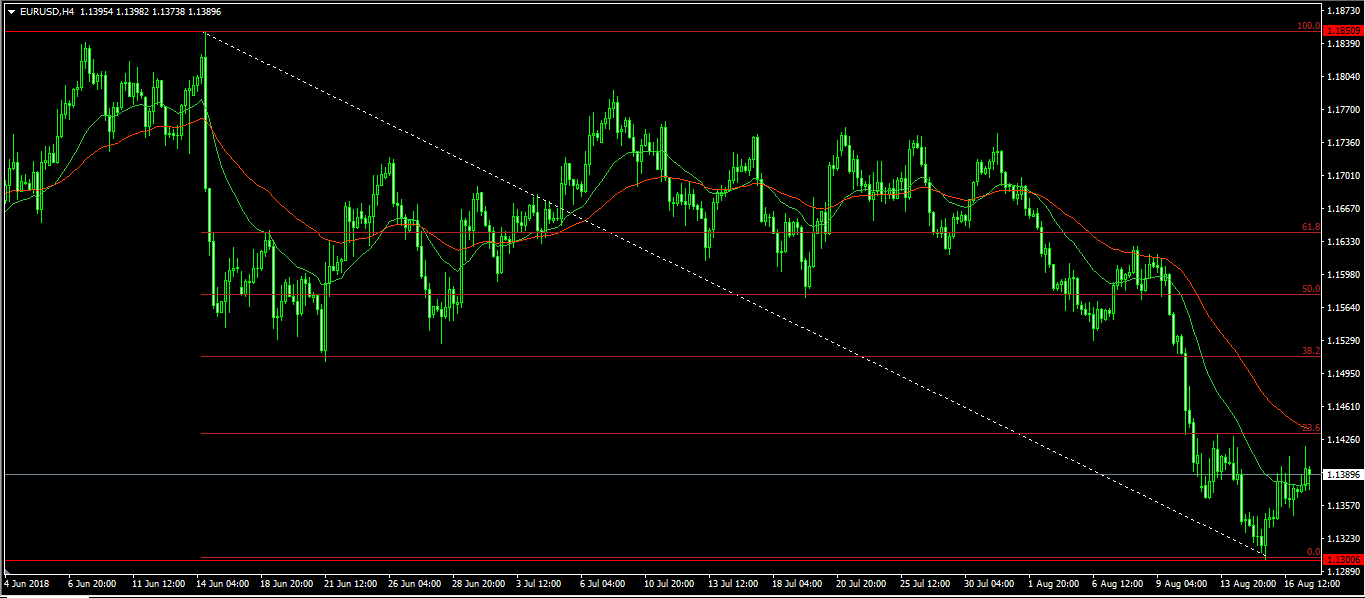

EUR/USD

The EUR/USD pair was little moved after the EU’s inflation data. It is now trading at 1.1390, which is close to the YTD low of 1.1300. The ADX is currently at 23 while the current price is close to the 23.6% Fibonacci Retracement level. The price is also close to the 21-period moving average and lower than the 50-period moving average, which is at the 23.6% Fibonacci level. The current trend seems weak based on the ADX number which means that the pair could resume the downward trend.

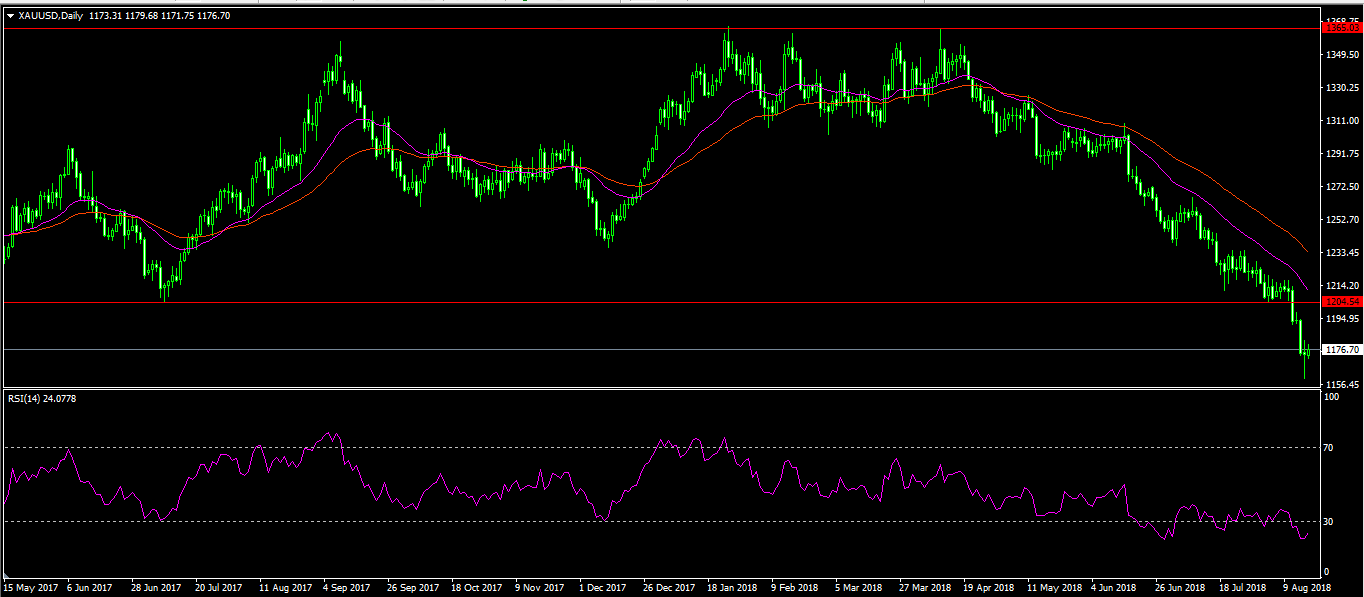

XAU/USD

The XAU/USD pair crossed the important support level of $1200 last week. This happened as the dollar strengthened. This week, the pair reached a low of $1160, which is the lowest level since January 2016. It is now trading at $1177, as the dollar takes a pause. On the daily chart below, the RSI for the pair is 24, which is the lowest level since May this year. The price is also below all the major moving averages. The pair is likely to continue to descend with the next target being the $1100 level.

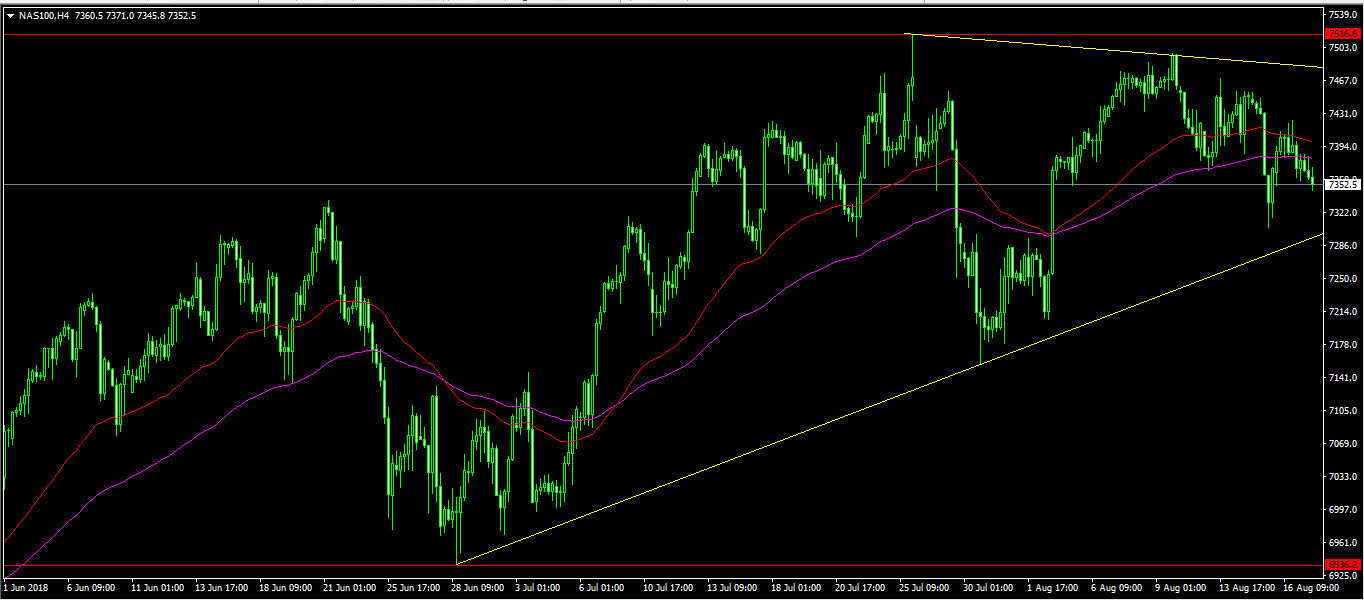

NAS100

The tech-heavy Nasdaq is trading at $7350, which is slightly lower than the all-time high of $7510. Today, the index fell after disappointing results by Nvidia and the worry about chip stocks. On the four-hour chart below, the current price is slightly below the 100 and 50-period exponential moving average (EMA). It is also slightly above a key support level. As the US and China restart the talks on trade, the index is likely to resume the upward trend.

Author

OctaFx Analyst Team

OctaFX

OctaFX is a market-leading forex broker, providing personalised forex brokerage services to customers in over 100 countries worldwide.