Germany - The Euro’s weakest link?

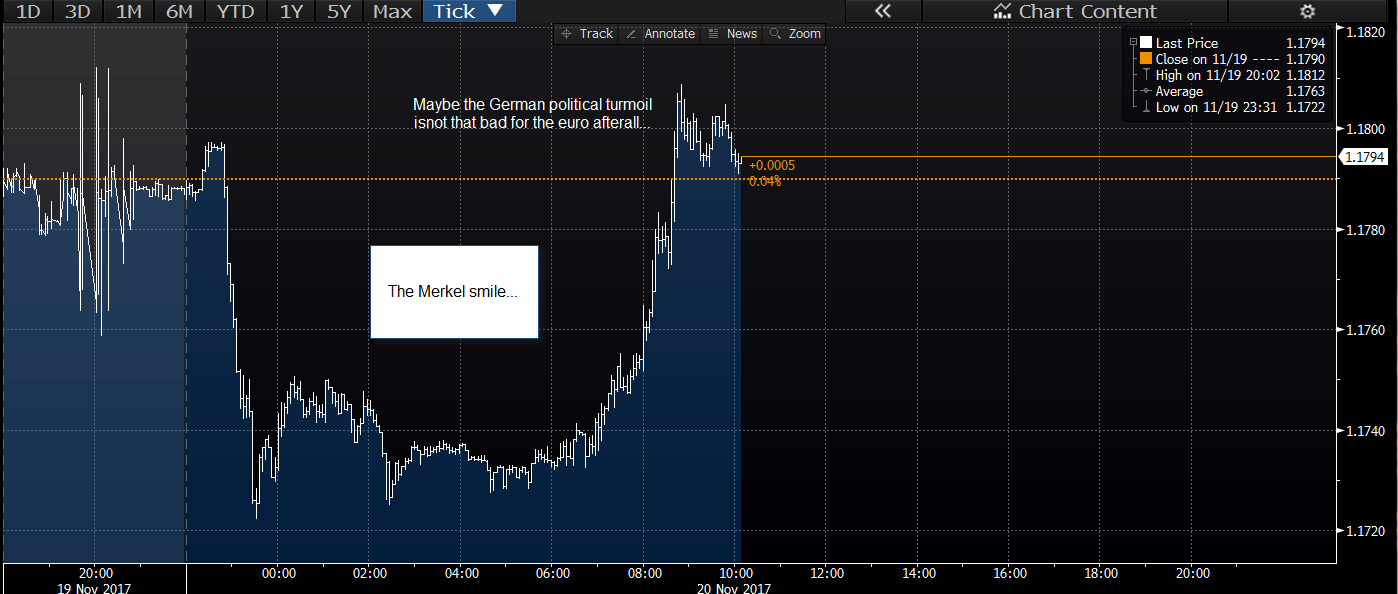

It’s been a morning of two halves for the euro on Monday, with news that the Jamaican coalition talks in Germany had broken down and Merkel’s position as Chancellor was at risk firstly weighing on the euro, driving EUR/USD down some 80 pips, before the market changed its mind and clawed back the early losses. Is the EUR/USD’s recovery, as we have affectionately named the Merkel ‘smile’ due to the shape of the chart as you can see below, a sign that the FX market is too complacent, or is the prospect of a Europe without Merkel at its heart just too ludicrous to contemplate?

Why the market is optimistic on the German political future

The latter seems most likely. Merkel’s options at this stage include forming a grand coalition with the Social Democrats, ruling a minority government or staging a new election. We believe that you can rule out the first option, the second and third options are most likely at this stage. If anyone can rule a minority government, surely it’s the consensus- building Angela Merkel? Also, Merkel’s own CDU party would surely be mad not to keep her as leader if there is another election due to her personal popularity across the country? This is why we think that the euro, German bond yields and the Dax have all managed to recover even in the midst of German political uncertainty.

Is the market being too complacent?

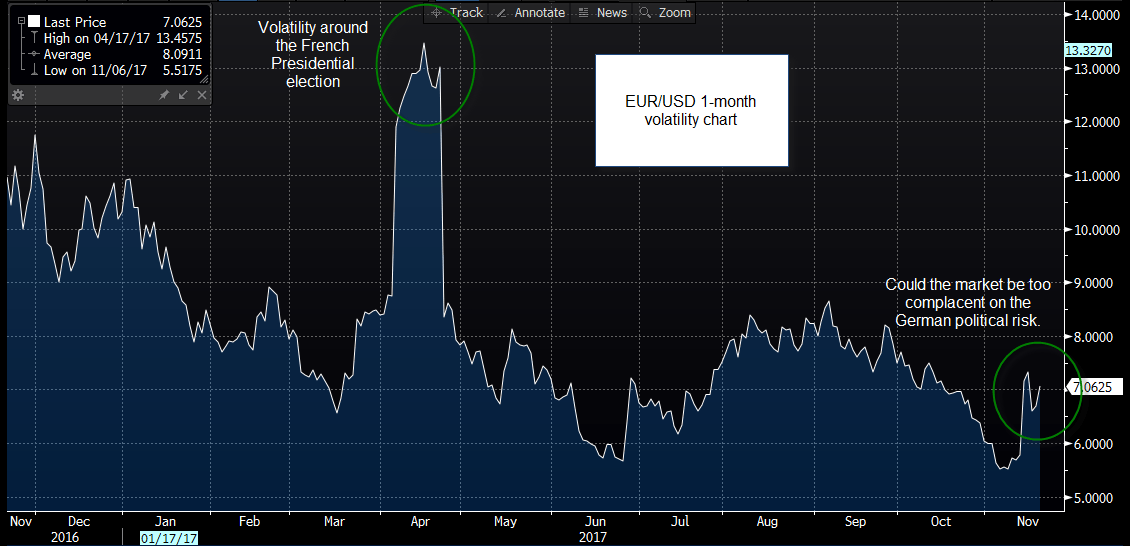

Of course we have to caveat that the market could be underestimating German election risk. If you look at chart 2 below, which shows 1-month EUR/USD volatility over the last 12 months, volatility has not picked up much as German coalition talks have broken down. Interestingly, volatility spiked ahead of the French election, which turned out to be a boon for markets as Emmanuel Macron was easily elected President of France. The market got the level of risk wrong back in April, and were overly worried, could they be wrong this time and be overly complacent? How this saga plays out in the coming days will be crucial for European traders. It’s not beyond the realm of possibility that Germany could end up being the biggest political hot potato for the Eurozone this year.

Brexit protected from political turmoil for now

The pound is also making headway at the start of the week, which is likely down to the news that the UK government is willing to offer an increased divorce settlement to the EU, potentially up to £40bn. The fact that the Brexit-baiting members of the cabinet also seem ready to back the enhanced offer is boosting the market reaction to this news. Of course, a Germany without Merkel could ultimately derail the Brexit negotiations and hurt the UK, and the pound, down the line. However, at this stage of the Brexit talks the negotiations are being led by the EU Commission rather than Germany, which should protect the process from the political turmoil for now.

UK: The Chancellor has to keep the Chancellor out of the Budget

With little economic data out today and relative quiet in Germany, the UK Budget is taking centre stage. While everyone knows that the Chancellor is unlikely to announce any major changes on a macro scale on Wednesday, the focus could shift to the economic projections and also how well the Chancellor’s Budget is received. Reports suggest that cabinet rivals are circling for his job and the Brexiteers’ want one of their own at the Treasury. Thus, the Chancellor has a tricky balancing act to ensure that his policies rather than his future is the central story on Wednesday.

There could be better news on the economic forecast front, with the Debt Management Office likely to reduce its borrowing target for 2017/2018. This could trigger a UK bond market rally (when yields fall) into year end. Surprisingly, the UK bond market is already the second best performing in the major market behind Italy, with a 2.3% gain so far this year. This performance could improve further if the Chancellor manages to pull off the impossible: boost spending and cut debt at the same time!

The FTSE 100 is mostly flat today, with only small gains for other European indices. The biggest movers to the upside are Sky and Barret Developments, with 3i one the weakest. Financials is one of the weakest sectors, and headlines like this from chief EU Negotiator Michael Barnier “Brexit means banks lose EU passporting” are unlikely to boost sentiment as the Brexit premium starts to weigh on some key sectors in the UK index into year end.

Chart 1: The Merkel ‘smile’

Chart 2: EUR/USD 1-month volatility

Author

Kathleen Brooks

XTB UK

Kathleen has nearly 15 years’ experience working with some of the leading retail trading and investment companies in the City of London.