German data sends stark warning on global growth

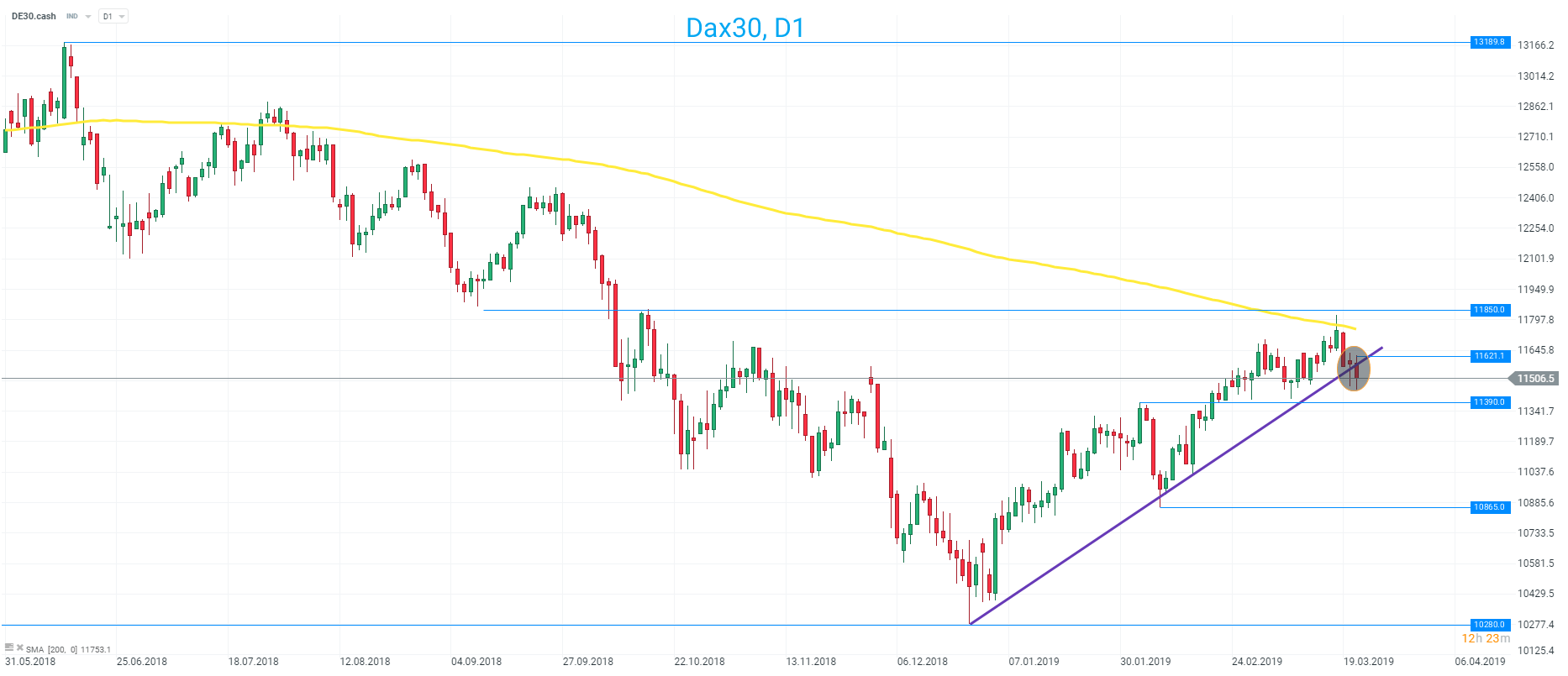

A series of worse than expected economic releases from Europe have sounded the alarm bell not just for the bloc, but also the global economy, by providing further evidence of a worldwide slowdown in economic activity. These industry surveys are keenly followed, and unlike employment or GDP figures they are commonly seen as leading indicators due to the nature of their composition which is heavily weighted to future expectations. Due to the country's large level of exports, German manufacturing is often seen as a bellwether of global economic activity and with this metric falling to its lowest level since August 2012 - and in doing so chalking up a 3rd consecutive month in contraction territory with another PMI reading below 50 - it's sending a clear and obvious warning sign on the health of the global economy. The German stock market tumbled on the release, with the Dax30 promptly shedding some 150 points in the initial reaction and after rising to its highest level since October on Tuesday, the market is now in danger of breaking down after a strong run higher of late.

The Dax is threatening to break below a rising trendline dating back to the December low. Price has taken a turn for the worse after hitting a 5-month high on Tuesday and briefly trading above the 200 day SMA. 11390 now seen as potentially key support. Source: xStation

EU offers UK two delays

As we come to the end of what has been another busy week on the Brexit front, it has now been confirmed that the Article 50 deadline of 29th March will be extended, but the length of the extension is still not certain. This new deadline will depend on the outcome of another meaningful vote on Theresa May's withdrawal agreement, with a victory for the PM seeing the UK leave the EU on the 22nd May – the last possible data for an exit without taking part in EU elections. Alternatively, and what now looks like the most likely outcome, if May's deal is rejected then a short extension to 12th April will be granted in what appears to be an effort to simply buy some time and avoid a no-deal Brexit by accident. Should May be defeated once more then it is likely that parliament will seek to take control of proceedings and therefore seek a longer extension, meaning participation in the EU elections, and a substantial change of tack in pursuing a softer version of Brexit – called by some Common Market 2.0.

No-deal tail risk remains

This would on balance be seen as positive for the pound but while the dual offer of an extension has reduced the threat of no-deal once more, there is still a feasible route through which it could occur. While Theresa May has thus far proven remarkably resilient to a number of events that would have ended many a Prime Minister's career, but another heavy defeat could well signal her death knell as she would surely find it hard to alter course so drastically after resolutely insisting that her deal is the only way forward. Her replacement would likely come from the hard Brexiteer camp, and they may then be not just reluctantly willing, but actively pursuing a no-deal Brexit. Of course, this series of events remains a long shot for now, but a significant tail-risk remains for the pound as the almost everyone seems to believe that a no-deal won't occur. The market has been badly wrong on Brexit once before, with the pound rallying strongly into the 2016 referendum on the expectation of a Remain victory and if it is caught wrong-footed once more then another large drop in sterling may lie just around the corner.

Author

David Cheetham

XTB UK