GBP/USD Price Forecast 2021: Cable braces for calendar comeback amid three exits

- With Brexit talks out of the way, markets can focus on the consequences of this historic change

- With Trump’s turmoil over, Biden’s tight work with the Fed is key to dollar action.

- Coronavirus vaccination should finish the crisis by year-end, yet a bumpy road awaits.

- The economic calendar is set for a comeback in influencing cable.

A traumatic 2020? Not for those cable traders looking for volatility. GBP/USD hit historic lows in response to the coronavirus crisis, changed its reaction function to printing money, and provided endless Brexit-related movements.

With Trump, Brexit – and eventually coronavirus out of the door – will things calm down 2021? The fading out of these three factors will likely lead to a calendar comeback – serving as the judge of the vaccine’s impact, Brexit, and government policies on both sides of the Atlantic.

GBP/USD Price Analysis 2020: Coronavirus outweighs Brexit and Trump

“When you lose, don’t lose the lesson.” The Dalai Lama’s words of wisdom are relevant to newbie traders – and for seasoned ones as well. The past year has seen a range of over 2,000 pips in GBP/USD, as well as how markets respond and lessons to take forward.

A turbulent year in pound/dollar, here is the daily chart:

-637442368446185649.png)

Coronavirus hits hard and high

One dark weekend in northern Italy in late February was when markets fully came to grips with a virus that previously only put Wuhan on the map. Coronavirus triggered a downfall that pounded the pound, sending it to 35-year lows against the safe-haven dollar.

Britain seemed to be caught off-guard. Prime Minister Boris Johnson hesitated before following other countries into lockdown and later came down with COVID-19, including a spell in intensive care. His recovery in April, at a time of massive fiscal and monetary support on both sides of the Atlantic, marked the grand comeback.

UK economy’s fall and rise in response to covid:

-637442369429175162.png)

Source: FXStreet

Britain was more prepared for the winter wave of the virus. Despite Johnson’s second lockdown hesitance, investors seemed to worry more about London’s status and Brexit (see later) than the new economic damage.

The UK was more successful with the covid vaccine announcement – and its dual positive effect on GBP/USD. The government secured agreements with a wide variety of pharma firms, including its homegrown AstraZeneca. The first Western-world vaccinations also began in Britain after a quick regulatory approval of the Pfizer/BioNTech jab, boosting the pound – while every progress on immunization weighed on the safe-haven dollar.

Printing pounds ≠ printing dollars

The peak of the crisis caught the Bank of England transitioning from Mark Carney to Governor Andrew Bailey. The new chief slashed interest rates to 0.10% – the lowest in the “Old Lady” set in its 300+ year history on his fourth day at the job.

More importantly, the BOE more than doubled its bond-buying scheme in three moves, with the last one coming despite the parallel vaccine announcement. The pre-pandemic logic that creating money out of thin air devalues the currency vanished and made way for a new narrative – monetary funding would help the government support the economy in times of trouble. The announcements were coordinated with the Treasury and convinced investors of an efficient government keen to keep the economic engines running.

On the other side of the pond, the old logic prevailed – printing greenbacks devalued the dollar, as it also reduced the flight to safety. The Federal Reserve boosted its balance sheet by some $3 trillion and at a rapid clip.

The Fed’s balance sheet:

-637442370574027417.png)

Source: Federal Reserve

The Washington-based institution also introduced new lending programs and announced a new policy framework – it would prioritize reaching its employment goals at the expense of letting inflation overheat. Jerome Powell, Chairman of the Federal Reserve, stressed that the bank was “not even thinking about thinking of raising rates.”

Austerity tossed away

While British hospitals lacked Personal Protective Equipment and the government’s U-turns on lockdowns made it a laughing stock, the economic response was applauded by most.

Chancellor of the Exchequer Rishi Sunak delivered rapid support to businesses and the successful furlough scheme, which paid those unable to work a large chunk of their salaries – keeping them attached to their workplace and depressing the unemployment rate. This Conservative government ditched austerity and markets cheered.

Capitol Hill also delivered at first, launching the generous, multi-trillion CARES act, which provided a federal top-up to unemployment benefits and support to small businesses. Later in the year, Republicans and Democrats failed to reach an agreement on additional aid.

Both parties probably calculated that ceding ground to the other party would be bad politics in an election year, yet there were also critical differences, and the US economy recovered. While the dollar moved in response to stimulus news, the lack of a new accord did not materially halt the dollar’s decline.

Brexit disappears, then resurfaces

Parliament Square was the scene of a celebration on January 31, the day the UK formally left the EU and entered the transition period that expires at year-end. Brussels and London kicked off talks about future trade relations, which were quickly sidelined due to the virus – that infected both chief negotiators.

While governments were battling covid on both sides of the English Channel, Johnson refrained from extending the implementation phase when he could, up to mid-June, and preferred introducing the controversial Internal Markets Bill (IMB), which knowingly violated the 2019 Brexit Withdrawal Agreement he signed. That angered the Europeans but seemed like a side issue at the time.

Talks only entered high gear in the autumn, closer to the deadline, and markets rediscovered their interest in the topic. The IMB triggered legal action from Brussels and diminished trust, pushing the bloc to emphasize governance even after Britain dropped the controversial clauses in the legislation.

As the days shortened, deadlines and break-offs in talks came and went. Apart from governance, the EU and the UK clashed on the sensitive topic of fisheries – despite its minuscule economic size – and the Level Playing Field (LPF).

Every headline related to London’s insistence on sovereignty and Brussels seeking to disallow Britain to undercut it on labor and environmental issues triggered sharp reactions in GBP/USD. Brexit returned in full force as the clock was ticking toward the only real deadline – December 31.

US elections: Changing narratives

The US Presidential Elections provided powerful drama – such as the death of Supreme Court’s Justice Ruth Bader-Ginsburg and President Donald Trump’s coronavirus infection – but not as much market action.

Nevertheless, similar to the pound’s positive reaction to money printing, more of it was a novelty, so were changing narratives around the long campaign, which serve as a lesson moving forward.

Investors initially feared that now-President-elect Joe Biden would enact sweeping market-unfriendly reforms with a clean Democratic sweep – a “blue wave” and seemed to prefer a split government, whichever candidate won. Later in the campaign, the greatest fear became a contested election that would put the US in political limbo. Investors learned to love the “wave” – which would guarantee more stimulus.

Biden eventually won a decisive 306:232 electoral college, enough to calm fears of a bitter court battle – Trump tried, but was defeated in dozens of legal cases. However, Democrats have yet to flip the Senate. While the fate of the upper chamber and large stimulus now hinges on special elections in January, the prospects of a divided government suddenly looked more appealing. The safe-haven dollar has been on the decline since the vote. While vaccines’ developments did the heavy lifting for markets and pushed the dollar lower, politics remained on the sidelines – they were insufficient to alter the optimism the pandemic was nearing the end.

Biden won some 81 million votes, seven million or 4.5% more than Trump:

-637442372868715190.png)

Source: New York Times

GBP/USD 2021 Forecast: Is the only way up?

After incredible uncertainty, one anchor of stability is that time cannot be stopped – 2020 will be over, and 2021 will see three significant endings: Brexit, Trump and the virus.

Brexit: Images first, trade data later

The Brexit transition period expires strictly at year-end, but the consequences will take time to be known. Like in 2020, Brexit-related developments will likely dominate the headlines at first – especially as images of long queues of lorries in Dover take over the news cycle.

It is unclear if both sides will sign a trade deal, but this is the first time Britain is practically out of the EU – during the transition period there were virtually no changes in bilateral relations. Moreover, Johnson opted already in 2019 to a relatively hard exit. With an agreement, the Office of Budget Responsibility assumes a 4% hit to GDP and an extra 2% without an accord.

Traffic jams will likely be sorted out relatively shortly, and the media is set to move on from stories about companies facing bureaucratic hurdles to the ongoing coronavirus crisis. It would also be hard to disengage the Brexit damage from the blow inflicted by a potential post-Christmas wave of the virus.

After over four years that Brexit headlines had a substantial impact on the pound, traders may feel that the topic is entirely over after a few weeks. Following long-suffering and the feeling that Brexit belongs to the past could send sterling higher.

Nevertheless, the first closure of a main 2016 event – the second being Trump’s victory – is set to continue impacting the economy, but its influence will probably move to economic data rather than via the latest comments from an unnamed EU official. Once the world begins emerging from the covid disaster, Britain could find itself at a competitive disadvantage – a potential downward driver for the pound.

Vaccine vs. the virus

The first few months of 2021 will likely be horrible as winter forces pandemic-fatigued people to stay indoors – potentially further spreading the virus. Moreover, the production, distribution and efficiency of the vaccines will probably run into bumps, and an atmosphere of despair may take over.

While Britain is unlikely to suffer more than others, the safe-haven dollar has room to rise in early 2021. However, human ingenuity during 2020 promises rapid solutions to initial issues.

Effect of the Pfizer vaccine:

-637442374090130193.png)

Source: Science Alert

The UK is moving faster than other countries in vaccinating its population, and that may be underappreciated by markets. A successful and rapid immunization campaign could send sterling higher in the spring and summer when Britons will likely return to normal life sooner than their counterparts in other parts of the developed world.

By the end of 2021, the world will probably return to almost wholly to the new normal, and the virus’ impact on currencies will likely wane.

Pound going north with northern politics? BOE in the balance

As Brexit and the virus gradually fade away, domestic fiscal policy is set to gain ground. Johnson owes a substantial part of his 2019 election victory to breaking the “red wall” – turning former working-class, Labour northern seats Conservative blue. The “Get Brexit Done” message and a hint at throwing a stone at the system convinced many to “lend” their vote to the Tories.

The party of Margaret Thatcher and austerity-leading George Osborne up to 2016, ditched prudence and opted for more generous spending to make the northern loans permanent. However, appealing to northern voters may push anti-Brexit, socially liberal and more affluent southern voters to Labour’s new moderate leader Keir Starmer.

Markets are currently in love with the “money tree” – increased government spending – while forgetting about debt. As long as inflation is kept depressed, the BOE could continue funding the government and investors would rush into the pound – a re-run of 2020.

BOE Balance Sheet:

-637442375187480685.png)

Source: Trading Economics

However, if Chancellor Sunak returns to his Thatcherite roots and cuts spending, sterling could suffer. This man at 11 Downing Street is the one to watch as his influence continues to grow while Johnson’s mismanagement of the crisis is making him less popular. There is a good reason why the opposition was moving its attention away from the PM and onto the Chancellor as 2020 progressed.

Returning to the “Old Lady”, its policy has become more intertwined with the government in 2020 and that is unlikely to change. As mentioned above, continued government funding would be positive for sterling, but if inflation rises – whether a result of fiscal expenditure, Brexit, rising commodity prices or anything else – the BOE would be forced to act.

Governor Bailey will probably try to refrain from any rate hikes as much as possible in such a scenario. However, if push comes to shove, a rate hike would not necessarily be a boost for sterling – as it would slow the economy and curb government spending.

The BOE could also hurt the pound by finally setting negative rates – after seemingly crying wolf for months. That would have little impact on the economy but would weigh on the currency.

Overall, the bank’s rate policy is set to be a lose-lose situation for sterling, while additional bond-buying tied to fiscal splashing would be pound-positive.

US stimulus critical for the dollar

Georgia is on everybody’s minds – the runoff Senate elections on January 5 will determine control of the upper house. If Democrats pull off a dual victory in the tightly contested state, stimulus is set to be generous, pushing the dollar down. While Biden would find it hard to pass major reforms, aid to states, infrastructure spending and higher unemployment benefits should be a no-brainer, and markets would love the cash.

However, one Republican victory in Georgia will be enough to limit any extra spending and would set Washington back to a stalemate. That would ultimately fail to provide meaningful support to the US and global economies, boosting the dollar.

The reaction to monetary stimulus will be more straightforward in the US – an expansion of the Fed’s bond-buying program would weigh on the dollar while tapering it down – a highly unlikely scenario in 2021 – would push it higher.

The US monthly budget statement shows the impact of the virus:

-637442376618273773.png)

Source: FXStreet

The belief that inflation would make a comeback is gaining momentum among economists. Domestic final supply has shrunk during the coronavirus crisis and it would be hard to ramp it up again. One example is the need of retraining pilots to fly the freshly-vaccinated hoards of tourists. Another potential trigger of higher prices comes from the slow deglobalization process and the Sino-American decoupling. Sourcing materials in local markets cost more.

Are the 2011 inflationistas coming out of their woodwork shortly? Not so fast, this theory is far from becoming reality. However, if prices do rise and the Fed raises rates, the dollar would rise, another straightforward reaction.

The special relationship could be pound-positive

Johnson has been sometimes called “Britain’s Trump” and Biden has warned the UK not to violate the Good Friday peace agreement in Ireland. Does that mean a fraught “special relationship”? Probably not, as both leaders are practical, and more importantly, the US Democratic Party is economically aligned with the UK’s Conservatives.

Both support free trade and a dose of welfare. Both countries also have a common interest in halting China’s technological advance and Russian aggression. The special relationship is making a comeback and that could serve as a bullish factor for cable, albeit a minor one.

GBP/USD technical levels 2021

-637442377690148375.png)

The weekly chart comes in handy when looking toward the full year. The picture is generally bullish for cable, with momentum pointing higher and after the pair recaptured the 50-week and 200-week Simple Moving Averages. The Relative Strength Index is far from overbought or oversold territories.

Critical resistance awaits at 1.3540, the 2020 peak, which is only barely above the 2019 high. It is followed by 1.3730, a swing low from 2017 and then by the round 1.40 level, 1.4220 and 1.44.

Support is at the December swing low of 1.3140, followed by 1.2850, a cushion from several months earlier, and then by 1.2670. Further down, 1.2430, 1.2080 and 1.1970 await for GBP/USD.

Conclusion

There was no 20/20 vision in 2020, a year full of uncertainties – both old such as Brexit and Trump, and new, as covid. These three clouds are set to clear at various paces, making way for rapid changes and new challenges. Economic figures will likely be the arbiter of Brexit dampening effect, the UK’s high readiness for receiving the vaccine and other factors. The changing relationship between governments and central banks will likely be in focus.

How will GBP/USD trade during 2021? After a year full of surprises, it is hard to predict, but going on a limb, there is room for the pound to blossom in the spring, as it outperforms rivals in exiting the covid crisis and as Brexit is forgotten. Sterling could later turn south once peers catch up and the exit from the EU takes its toll.

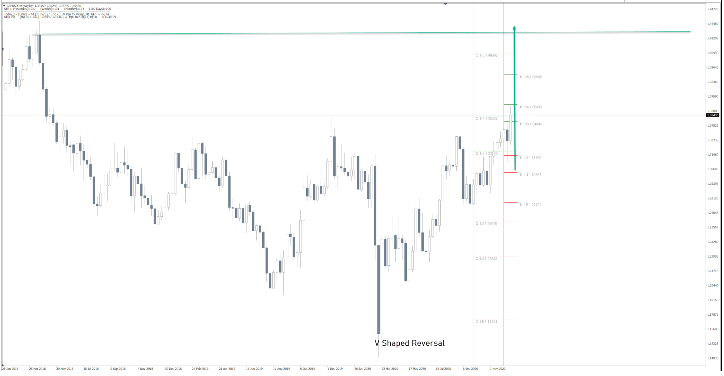

Nenad Kerkez projects a long-term bullish outlook for the Pound on his Camarilla Pivot Point analysis:

GBP/USD Camarilla Pivot Point Analysis

The GBP/USD is in an uptrend. Whatever happens with Brexit, the UK has always been a strong force and the presence in the world and the GBP will get stronger. Buying the dips is the option. We can also spot the V-Shaped Reversal meaning the low has been set.

Forecast Poll 2021

| Forecast | Q1 - Mar 31st | Q2 - Jun 30th | Q4 - Dec 31st |

|---|---|---|---|

| Bullish | 53.5% | 52.3% | 63.6% |

| Bearish | 7.0% | 9.1% | 9.1% |

| Sideways | 39.5% | 38.6% | 27.3% |

| Average Forecast Price | 1.3733 | 1.3883 | 1.4162 |

| EXPERTS | Q1 - Mar 31st | Q2 - Jun 30th | Q4 - Dec 31st |

|---|---|---|---|

| Alberto Muñoz | 1.3700 Bullish | 1.3850 Bullish | 1.4300 Bullish |

| Andrew Lockwood | 1.2800 Bearish | 1.3500 Sideways | 1.4500 Bullish |

| Andrew Pancholi | 1.3280 Sideways | 1.2856 Bearish | 1.4330 Bullish |

| Andria Pichidi | 1.3600 Sideways | 1.3950 Bullish | 1.4260 Bullish |

| ANZ FX Strategy Team | 1.3600 Sideways | 1.3700 Sideways | 1.4000 Bullish |

| BBVA FXTeam | 1.3800 Bullish | 1.4000 Bullish | 1.4400 Bullish |

| Blake Morrow | 1.3600 Sideways | 1.3500 Sideways | 1.4000 Bullish |

| Brad Alexander | 1.4000 Bullish | 1.3000 Sideways | 1.2500 Bearish |

| Dmitry Lukashov | 1.4100 Bullish | 1.4800 Bullish | 1.4400 Bullish |

| Dukascopy Bank Team | 1.3600 Sideways | 1.4200 Bullish | 1.4350 Bullish |

| Eliman Dambell | 1.4600 Bullish | 1.3200 Sideways | 1.3700 Sideways |

| FP Markets Team | 1.4300 Bullish | 1.4600 Bullish | 1.5000 Bullish |

| Frank Walbaum | 1.3600 Sideways | 1.4200 Bullish | 1.5000 Sideways |

| George Hallmey | 1.3800 Bullish | 1.4500 Bullish | 1.5000 Bullish |

| Giles Coghlan | 1.4000 Bullish | 1.5000 Bullish | 1.5000 Bullish |

| Grega Horvat | 1.3800 Bullish | 1.3500 Sideways | 1.3000 Sideways |

| Jamie Saettele | 1.2800 Bearish | 1.4300 Bullish | 1.5800 Bullish |

| Jeff Langin | 1.3700 Bullish | 1.3950 Bullish | 1.3500 Sideways |

| Jeffrey Halley | 1.4000 Bullish | 1.4500 Bullish | 1.5000 Bullish |

| JFD Team | 1.3770 Bullish | 1.4375 Bullish | 1.5000 Bullish |

| Joseph Trevisani | 1.3800 Bearish | 1.4000 Bullish | 1.5000 Bullish |

| JP Morgan Global FX Strategy | - | 1.3400 Sideways | 1.3200 Sideways |

| Kaia Parv, CFA | 1.3300 Sideways | 1.3000 Sideways | 1.2800 Sideways |

| M.Ali Zah | 1.3000 Sideways | 1.3800 Bullish | 1.2600 Bearish |

| Matthew Levy, CFA | 1.7500 Bullish | 1.8000 Bullish | 1.8000 Bullish |

| Michael Hewson | 1.4000 Bullish | - | - |

| Mthokozisi Mpofu | 1.3075 Sideways | 1.2714 Bearish | 1.2279 Bearish |

| Murali Sarma | 1.3743 Bullish | 1.3539 Sideways | 1.3998 Bullish |

| Navin Prithyani | 1.3400 Sideways | 1.3700 Sideways | 1.3000 Sideways |

| Nenad Kerkez | 1.3880 Bullish | 1.4082 Bullish | 1.4200 Bullish |

| Nomura FX Research & Strategy | 1.3300 Sideways | 1.3600 Sideways | 1.4000 Bullish |

| Paul Dixon | 1.3300 Sideways | 1.3300 Sideways | 1.3300 Sideways |

| Rick Ackerman | 1.3465 Sideways | 1.3802 Bullish | 1.3335 Sideways |

| RoboForex Team | 1.4977 Bullish | 1.4246 Bullish | 1.6072 Bullish |

| Sachin Kotecha | 1.4000 Bullish | 1.5500 Bullish | 1.7000 Bullish |

| Slobodan Drvenica | 1.4200 Bullish | 1.3700 Sideways | 1.4800 Bullish |

| Société Génerale Analyst Team | - | 1.4300 Bullish | 1.4800 Bullish |

| Standard Bank Research Team | 1.4000 Bullish | 1.4000 Bullish | 1.4000 Bullish |

| Stephen Innes | 1.3000 Sideways | 1.2700 Bearish | 1.2500 Bearish |

| Theotrade Analysis Team | 1.2000 Bearish | 1.2500 Bearish | 1.3000 Sideways |

| Unicredit Research | 1.3200 Sideways | 1.3400 Sideways | 1.3600 Sideways |

| Vladislav Brykin | 1.3950 Bullish | 1.3170 Sideways | 1.4200 Bullish |

| Walid Salah El Din | 1.3400 Sideways | 1.3600 Sideways | 1.4000 Bullish |

| Wayne Ko Heng Whye | 1.3600 Sideways | 1.3500 Sideways | 1.3400 Sideways |

| Yohay Elam | 1.4000 Bullish | 1.3800 Bullish | 1.3000 Sideways |

Regardless of Brexit deal or no-deal the path of the GBP should be higher. Certainty will bring relief to investors and send inflows into the GBP.

Uncertainty of Brexit deal keep under pressure pound next few years, also negative interest rate expecting Q1 end from BOE.

by M.Ali Zah

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.