GBP/USD Forecast: After the big breakout, Boris' Brexit move, UK GDP, and the Fed are keys

- GBP/USD has been rising amid ongoing opening optimism resulting in dollar weakness.

- UK GDP, the Federal Reserve's decision, and coronavirus developments are eyed.

- Early June's daily chart is showing the uptrend may be stretched despite the breakout.

- The FX Poll is pointing to losses on all timeframes.

Unrest in Hong Kong or in New York markets march on the dollar's downward drift continues. Will the Fed now fuel the next move forward? For GBP/USD concerns about Brexit have only had a limited impact, yet the story is set to grow in importance, in addition to fresh figures for the British economy.

This week in GBP/USD: Brexit on the edge, US unrest

Will the UK end the Brexit transition period without a trade deal? That is a growing worry among investors and also in the corridors of the Bank of England. Reports that both sides are willing to make concessions have not materialized, and the impasse continues.

Sterling suffered in response to fears the UK will fall back to World Trade Organization terms in 2021. Prime Minister Boris Johnson stuck to his stance of refusing an extension to this period amid deadlocked negotiations.

UK coronavirus figures have continued falling, yet at a slow pace. Germany's snubbing of Britain – leaving it in a list of countries where travel is not advised – speaks volumes of the current health situation. Business confidence, as seen in Markit's final Services Manufacturing Index, has only marginally improved.

Traders continued unwinding positions in the safe-haven US dollar amid hope that the ongoing reopening of the world's largest economy continues. Daily deaths from the disease have dropped below 1,000, yet concerns about a second wave and the lack of testing capacity persist.

The disease may also spread among densely crowded demonstrators. The murder of George Floyd, an unarmed black man at the arms of the police, sparked massive protests, with peaceful daytime events occasionally turning into looting late at night. Several cities imposed curfews yet the scenes – some last seen in the 1960s – failed to worry markets for now.

Moreover, the unfolding events have reportedly prompted lawmakers in both major parties to accelerate talks about the next fiscal package, also keeping markets bid and the dollar depressed.

Business confidence continues rising in America, with ISM's Purchasing Managers' Indexes bouncing more than expected, albeit continuing to point to contraction.

However, the US jobs report is already pointing to fresh expansion. The Non'Farm Payrolls shocked economists with a leap of over 2.5 million jobs – not a loss. Moreover, the unemployment rate dropped to 13.3% and the fall in wages indicates a return of low-earners to the labor force. The greenback gained some ground, but it was limited against the pound.

UK events: GDP and further Brexit developments

Will Johnson make a dramatic intervention to salvage Brexit talks? The PM previously relented on not having a customs border in the Irish Sea, providing the necessary trigger for a breakthrough in October.

Brussels is banking on a similar move from London, yet that is still to be seen. The major sticking points remain fisheries – a minuscule industry yet one that is prized by Brexiteers – and general trading terms, especially those concerning the all-important financial services sector.

COVID-19 statistics remain of high interest. It is essential to note that figures published on Monday tend to be extraordinarily low and encouraging, but they tend to jump afterward. The seven-day rolling moving average should continue falling in order to provide more hope and a boost to the pound.

Gross Domestic Product figures for April stand out on the calendar. While monthly growth publications are normally shrugged off by investors, statistics for April 2020 are of high importance – they are for a full month of lockdown.

The data will allow economists to extrapolate the data and make better estimates for the devastation in the second quarter. The British economy shrank by 5.8% in March and the downfall was likely considerably worse in April.

Manufacturing Production figures for that month may also move markets. The industrial sector was less affected than the services one.

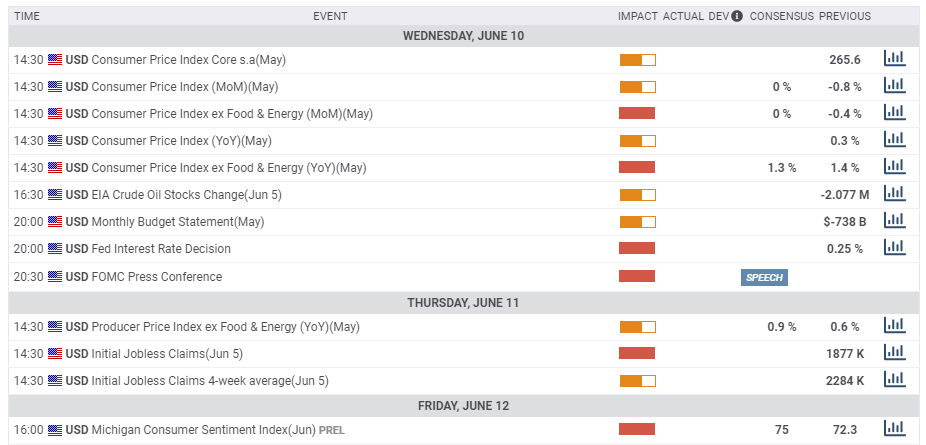

Here is the list of UK events from the FXStreet calendar:

US events: Fed decision stands out

Race relations, which have dominated headlines in the past week, could easily slip out of the news cycle even as the underlying issues remain unresolved. On the other hand, if they impact opinion polls, showing growing chances of Democrats winning all levers of power, the greenback may rise.

Sino-American tensions may return to the forefront. China has reacted gleefully to unrest in the US, criticizing Washington for hypocrisy around Hong Kong. Investors will likely shrug off anything that is unrelated to the trade deal. Dogs that bark but do not bite may only provide excuses to buy stocks.

US inflation figures for May will likely show some stability after the drop in energy prices sent the headline Consumer Price Index down. Core CPI tumbled down amid the coronavirus crisis and will likely remain depressed.

The main event of the week is the Federal Reserve's rate decision. The world's most powerful central bank will most likely leave the borrowing costs unchanged, resisting pressures to set negative rates. The Fed is set to publish growth, employment, inflation, and internet rates projections – the dot-plot.

While the Washington-based institution will surely stress that uncertainty is high, an outlook that is not outright downbeat may boost sentiment and weigh on the dollar. A gloomy forecast, that reflects double-digit unemployment through year-end and a return to pre-pandemic output levels only late next year, will likely boost the greenback.

Jerome Powell, Chairman of the Federal Reserve, meets the press and is set to reject negative rates. On the other hand, his unequivocal commitment to support the economy will likely keep the mood cheerful. The Fed surprised many market observers with open-ended Quantitative Easing and buying of municipal and state bonds.

Powell will nudge lawmakers to act to boost the economy, with a new fiscal plan still under consideration. If he conveys a sense of urgency, the dollar may rise, while omitting such a message would imply things have improved. He will also have the chance to take stock of the latest economic indicators.

Late in the week, the University of Michigan's preliminary Consumer Sentiment Index for June is set to rock markets. After tumbling from around 100 to the low 70s, this gauge of expenditure is set to bounce from the lows. However, if the bounce is shallow despite recent reopening, the greenback has room to advance.

Here the upcoming top US events this week:

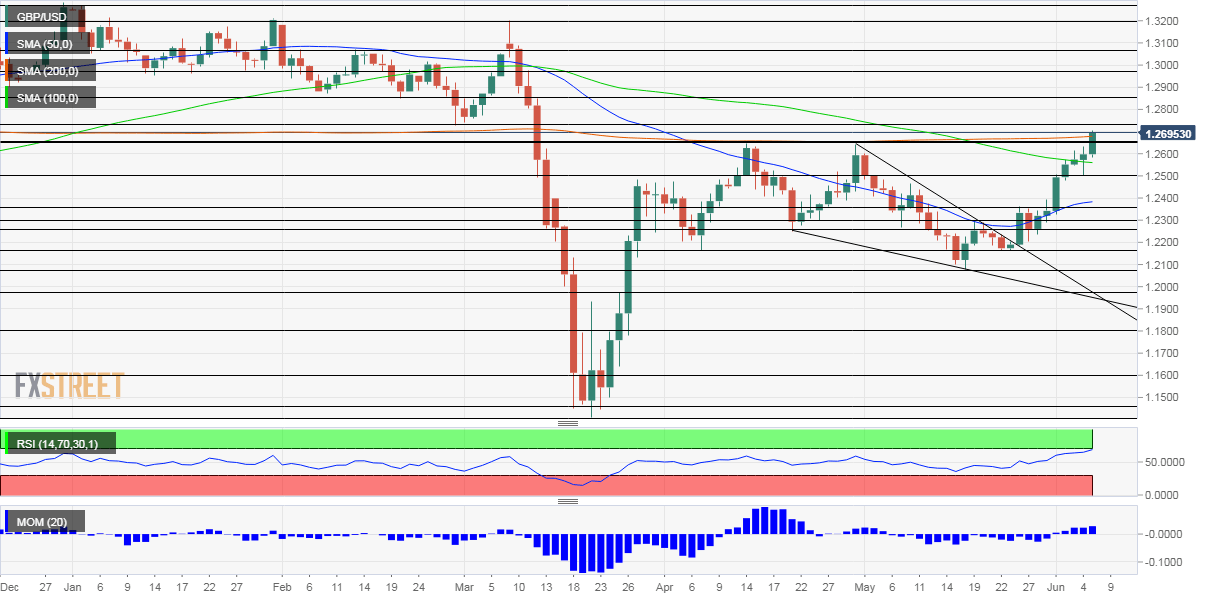

GBP/USD Technical Analysis

Pound/dollar finally broke above 1.2645, a trough double-top. It also won the battle against the 200-day Simple Moving Average on its way up, adding to the bullish, even though the break is yet to be confirmed. The Relative Strength Index on the daily chart is around 70 – entering overbought conditions and implying a correction.

The next line to watch is 1.2735, which provided support in early March. It is followed by 1.2850, a support line from earlier this year, and then by 1.2980. Above 1.30, the high upside target is March's peak of 1.32.

The former double-top of 1.2645 remains a battle line and a separator of ranges. Significant support awaits at 1.25, which is a round number and also a swing low in early June. Next, we find 1.2360, which was a stubborn cap in late May. The next lines are 1.23 and 1.2280, which were in play in April and May. Further down, 1.2160 worked as support twice in recent weeks.

GBP/USD Sentiment

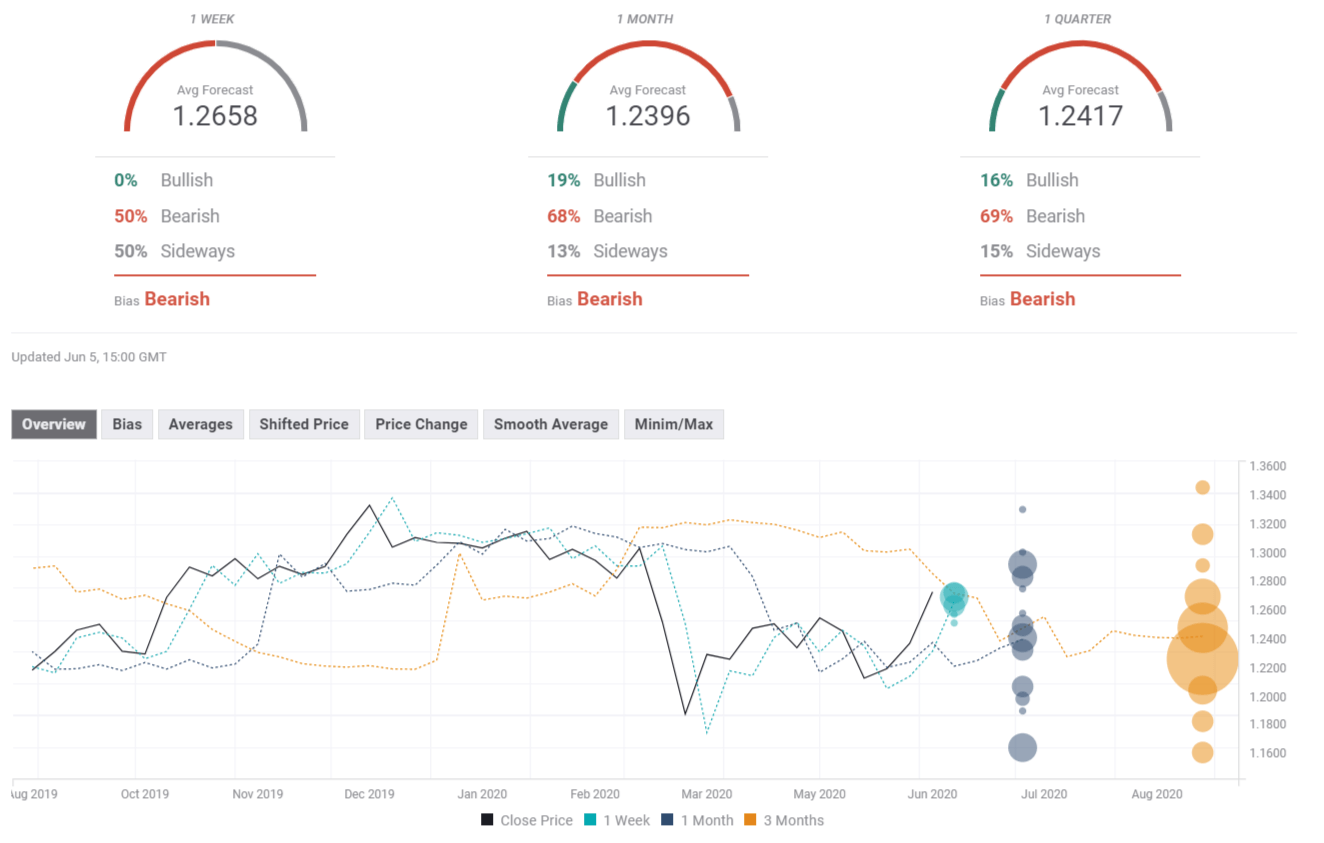

Without an improvement in UK COVID-19 statistics and Brexit, the fuel from the Fed may run out. Markets have gotten ahead of themselves and oversold conditions may trigger a correction.

The FXStreet Forecast Poll is showing a bearish trend with falling targets. It seems that experts remain skeptical about the recent rise. Short-term targets have been upgraded while medium and long-term ones are little changed.

Related Reads

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.