FX: Sterling risk premium tracker

With Brexit uncertainty rising, we introduce a sterling risk premium tracker. We look at various measures of sterling stress, gauged by factors such as our short-term financial fair value model, speculative positioning or the options market. We think the risk of no-deal Brexit / early election is underpriced by the market and look for more downside to GBP .

Where we are now?

Despite the rebound in the UK pound in the last few weeks, the short term sterling risk premium isn't extreme.

We estimate it to be worth around 2.5 % in EUR/GBP (vs 5% this August), with EUR/GBP still within its 1.5 standard deviation band as can be seen in figure 1. This means that more risk premium can be built into sterling. Our financial fair value model is based on short-term drivers of currencies such as rate spreads, yield curves and a gauge for risk appetite.

Read all about Brexit and the UK government's decision to suspend parliament here

Figure 1: More scope for GBP risk premium to rise

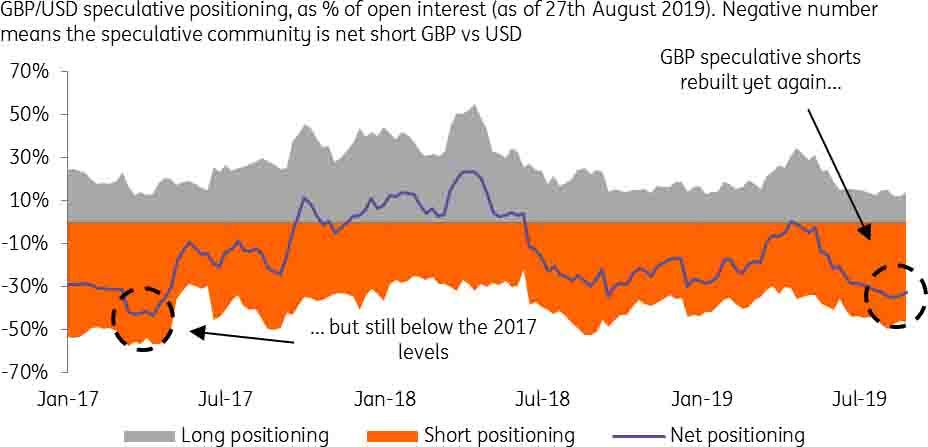

The built-up of speculative GBP/USD shorts paused in recent weeks. Although elevated, they are still below the 2017 extremes (33% of open interest currently vs 43% back then – as can be seen in figure 2). In the case of the rising probability of a no-deal Brexit and/or early elections, the shorts can rise further.

Figure 2: Speculative positioning elevated but below the 2017 levels

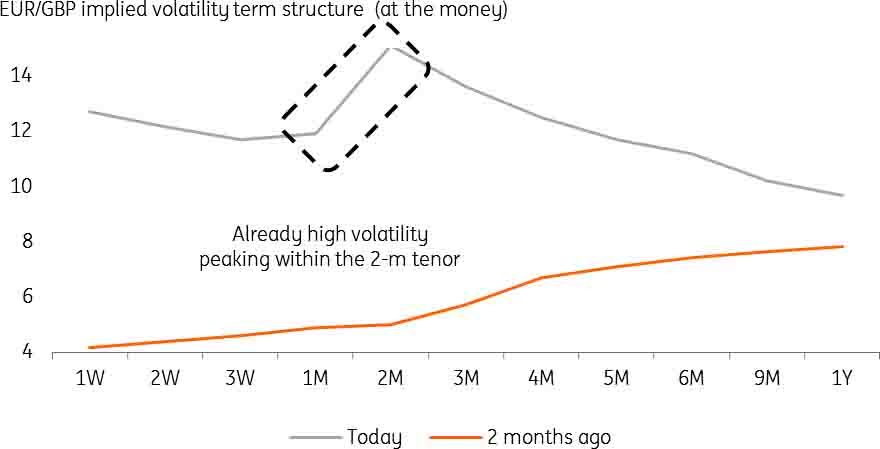

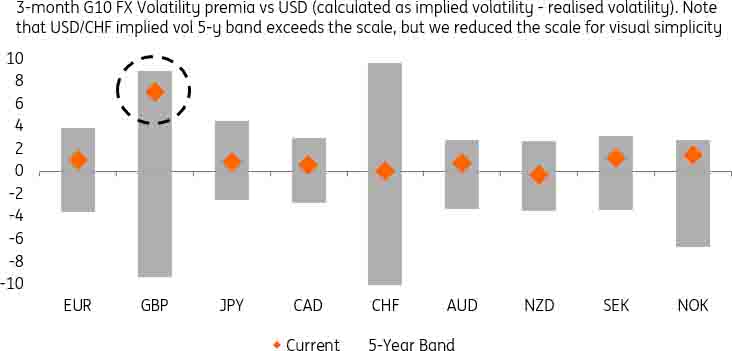

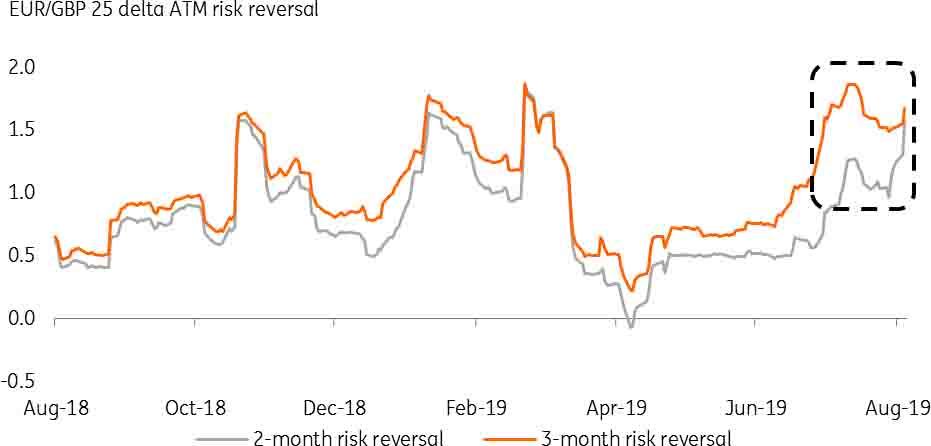

The options market clearly shows signs of stress. The EUR/GBP implied volatility curve (the term structure) is kinked around the deadline data as can be seen in figure 3 and GBP volatility premium is the highest in the G10 FX space (figure 4). Still, EUR/GBP risk reversals can rise further (figure 5)

Figure 3: The GBP volatility curve already heavily kinked around the Brexit date

Figure 4: Sterling volatility risk premium remains high

Figure 5: Risk reversals already at stressed levels but can get stressed even more

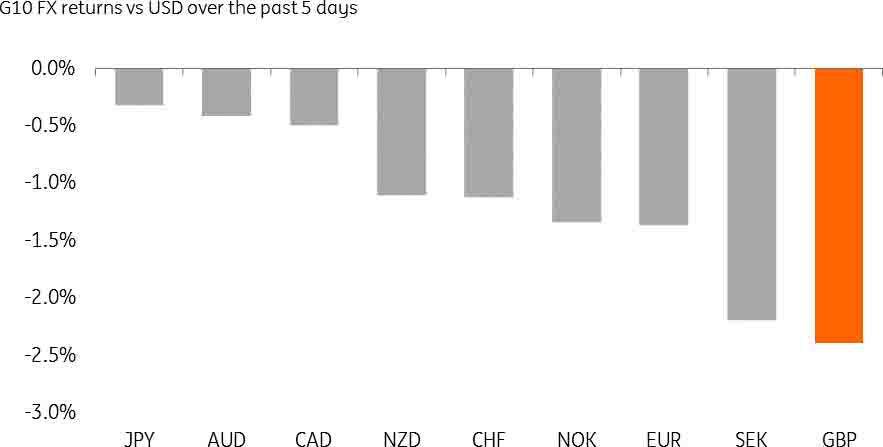

The recent decline of the pound over the last few days has turned sterling into the G10 FX underperformer yet again (figure 6) but we don’t expect the Bank of England to provide any help to the struggling pound, with dovish market pricing to firmly remain in place (figure 7). Currently, more than one full 25bp rate cut is priced in within six months.

Figure 6: GBP turning into a G10 FX underperformer yet again

Figure 7: Market pricing Bank of England rate cuts

What to look for?

If parliament moves a step closer to legislating against no-deal Brexit today by seizing control of the parliamentary agenda and prime minister Boris Johnson subsequently and successfully calls for early elections (likely in mid-October), we would see this as GBP negative given that (a) the Conservative party under PM Johnson's leadership will likely run on the ticket of a divisive stance vs EU (“no ifs or buts”), (b) the alternative option of a Labour government under Jeremy Corbyn may not be seen as an overly positive for market participants.

As we've written before, we view early elections as negative for GBP and continue to see downside risks to sterling. This is consistent with our forecast of EUR/GBP 0.95 within 1-3 months and GBP/USD falling to 1.17.

Read the original article: FX: Sterling risk premium tracker

Author

Petr Krpata, CFA

ING Economic and Financial Analysis

Petr Krpata is an FX strategist at ING and has been covering G10 and CEE currencies since May 2014. Previously, he was an FX and Rates strategist at Barclays Wealth and Investment Management.