For the FX market, what has the potential to hold back “sell on the news” is the dot-plot

Outlook: The Fed rate decision this afternoon is likely a third hike by 75 bp and the 5th hike overall. The probability of a 100 bp surprise is miniscule. Many analysts expect another 75 bp in November.

For the FX market, what has the potential to hold back “sell on the news” is the dot-plot. The new median dot for Fed funds at year-end is likely going to be 4-4.15%, from 3.375% in June and much ridiculed at the time. We are also interested in the GDP growth rate and inflation dots, but they don’t have the same muscle as Fed funds.

The dollar “should” gain over the longer term on the resolute Fed, even if we get the usual dollar sell-off this afternoon. But the dollar recovery will likely be hampered and maybe wrecked by some other factors, including the market’s great respect for the ECB stance that it needs to keep hiking, recession or not, to prevent inflation mentality. ECB Pres Lagarde repeated that position yesterday, leading to expectations of another 75 bp at the Oct 27 meeting. Anticipation of the ECB matching the Fed is a drag, even though the rate itself is so much lower.

Then there are tomorrow’s meetings at the Bank of England and Swiss National Bank. The Bloomberg survey for the BoE is 50 bp, but again there is a non-zero probability the BoE prefers to match the Fed. That could be buttressed by the idea of halting sterling’s slide.

As for the SNB, several analysts expect 75 bp from it, too, taking the deposit rate to a decent positive of 0.50% for the first time since 2015. Something big and favorable is expected–the dollar/CHF nosedived yesterday.

Finally, the Bank of Japan, about which nobody has a clue. It would be ridiculous to hold to the current policy unless the Bank wants to keep the yen falling, and intervention under the circumstances is equally silly.

Let’s dismiss one idea right off the bat–central banks as a general rule do not target their currency levels using interest rates. Essays saying so are either wrong or just out of date. In most instances, the currency is “managed” by the Treasury/Ministry of Finance, anyway. Switzerland was somewhat an exception when it decided years ago to hold the CHF down against the euro, a policy now dropped. That doesn’t mean central banks don’t look at the currency effect of rate policies, but it does mean that commentary linking the two are literally ignorant in the true sense of that word.

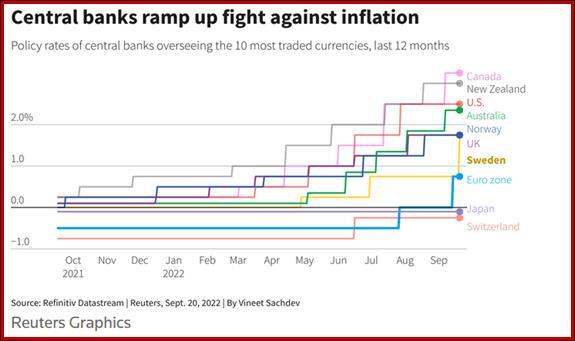

So far today, the rise in geopolitical risk from Russia is buttressing the “buy on the rumor” dollar gain, but tigers and stripes–we must expect a sell-off this afternoon. Late in the day it may seem like a good time to buy the dip, but beware–three central banks to go. See the nice Reuters chart of the major central banks. Canada and New Zealand lead. Now look at the NZD.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat