FOMC Preview: Do we really have to care about Yellen now?

- Policymakers expected to maintain the status quo.

- Fed's head replacement announcement set to overshadow FOMC announcement.

The Federal Open Market Committee starts its two-day meeting today and will unveil any decision on monetary policy on Wednesday, with the Central Bank largely expected to maintain the status quo, at least until December, when Yellen & Co. are expected to provide a third rate hike for the year. One should wonder, how much attention would the market pay to Mrs. Yellen, as this would be one of the last times she presides a meeting. December will be her final one, as on February, whoever Trump chooses will take over the Fed.

The list of possible candidates and their status as favorites, or not, has been responsible for a good part of dollar's strength during this October. Earlier this week, White House officials said that President Trump would likely announce his choice this Thursday, ahead of a trip abroad. At this point, the favorite is a Fed Governor, Jerome "Jay" Powell, who is aligned with Yellen in her view over monetary policy, somehow signaling that the Central Bank will maintain the current path toward normalization. Nor extremely hawkish, neither an ultra-dove, Powell´s nomination seems a "safe bet" from President Trump. And while uncertainty reigns ahead of a definition, a Powell confirmation on Thursday will undoubtedly bring some relief.

As for the Federal Reserve and as said above, the Central Bank is not expected to take any actions this time, but investors will be eagerly watching for clues to confirm or deny a December hike, and whatever 2018 will bring on monetary policy. Next Fed's chair announcement will probably be more relevant than this particular "non-live" meeting.

A big surprise will be if Trump chooses its second favorite nominee, John Taylor, who thinks that the monetary policy should be considerably less accommodative than it's been since the financial crisis. That puts him well into hawks side, but an ultra-hawkish Fed's head will have two immediate consequences: a stronger dollar, and a collapse of Wall Street, something that not even Trump is willing to deal with.

Anyway, and while the meeting could be a non-event ahead of Fed's head decision and the US Nonfarm Payroll report on Friday, surely market's participants will maintain a cautious stance ahead of the event, and rush afterward to price in any change in the wording seen previously.

EUR/USD technical outlook, levels to watch

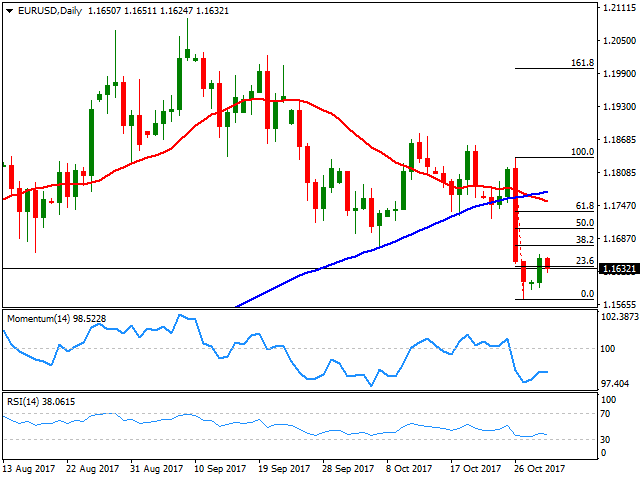

For the EUR/USD pair, things don't look good ever since the ECB's latest decision sent it down to its lowest in 3-month, with the decline later fueled by stronger-than-expected US advanced Q3 GDP. The pair remains near its October low of 1.1574, and while recovering some, the upward movement seems just corrective, as the pair trades around the 23.6% retracement of the ECB-US GDP decline. The daily chart presents a technically bearish stance, as the price broke below its 100 DMA, with the 20 DMA gaining downward traction below the largest, and technical indicators paring their advances well below their mid-lines, after correcting oversold conditions.

The same chart shows a H&S formation of around 400 pips height, with the broken neckline at 1.1660, which theoretically means that the pair has room to fall to 1.1260, although there's a long way toward the level and many big "stones" in the pathway. At this point, however, a test of 1.1460 seems possible, particularly if the upcoming events, including Fed's decision, the name of the new Fed's head, and the Nonfarm Payroll report, all surprise toward the upside. The 1.1460 region has been a major resistance area for most of 2015 up to mid this 2017. Between the monthly low and this last, the pair has an intermediate support at 1.1520.

To the upside, the main resistance is the neckline of the mentioned figure at 1.1660, followed by the 1.1720 level. Beyond this last, 1.1800 comes next, with steady gains beyond it required for a trend change, something that seems quite unlikely at the time being.

Author

Valeria Bednarik

FXStreet

Valeria Bednarik was born and lives in Buenos Aires, Argentina. Her passion for math and numbers pushed her into studying economics in her younger years.