FOMC Minutes Preview: Did policymakers discuss returning to bigger rate hikes?

- The first FOMC Minutes of 2023 will be published on February 22.

- US Dollar Index looks to post monthly gains, supported by hawkish Fed bets.

- Investors will look for comments regarding the possibility of Fed going back to 50 bps hikes.

The US Federal Reserve will release the minutes of the Federal Open Market Committee’s (FOMC) January 31 - February 1 policy meeting at 19:00 GMT, on Wednesday, February 22.

Following its first policy meeting of the year, the FOMC decided to raise the federal funds rate by 25 basis points to the range of 4.5 - 4.75% as expected. In its policy statement, the Fed reiterated that it would consider cumulative tightening, policy lags and economic developments in determining the extent of future rate hikes. Still, it noted that “ongoing increases” in rates will be appropriate.

During the press conference, FOMC Chairman Jerome Powell acknowledged that the disinflationary process had started and said that it was in the early stages. Market participants assessed this comment as a significant dovish shift in the Fed’s tone. Although Powell tried his best to convince markets that it will not be appropriate to cut rates this year, risk flows dominated the action and the US Dollar suffered heavy losses against its rivals.

Just a couple of days later, the US Bureau of Labor Statistics reported that Nonfarm Payrolls rose by 517,000 in January. With this reading surpassing the market expectation of 185,000 by a wide margin, hawkish Fed bets returned and investors started to consider the possibility of the Fed raising the policy rate one more time after March in light of tight labor market conditions.

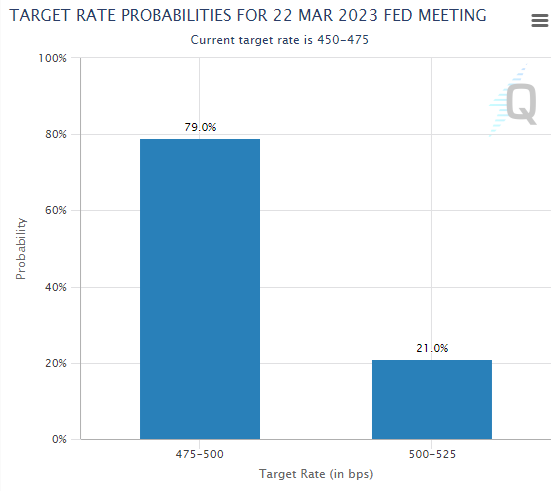

Additionally, hawkish comments from FOMC policymakers triggered a leg higher in US Treasury bond yields and helped the US Dollar preserve its strength. According to the CME Group FedWatch Tool, markets are pricing in an 80% probability that the Fed will raise its policy rate by 25 bps in March and May.

FOMC Minutes market implications

The US Dollar’s upbeat performance in February has been driven by the impressive January jobs report and the hawkish Fed commentary that followed the report. The US Dollar Index remains on track to snap a four-month losing streak as it’s up nearly 2% this month. Hence, it would be fair to say that the Fed’s publication is likely to be outdated and unlikely to offer any fresh insights into the policy outlook.

Having said that, Cleveland Fed President Loretta Mester said last week that she saw a “compelling case” for a 50 bps rate hike at the last policy meeting. On the same note, "I was an advocate for a 50 bps hike and I argued that we should get to the level of rates the committee viewed as sufficiently restrictive as soon as we could," St. Louis Federal Reserve's James Bullard said.

We know that the vote for the 25 bps hike at the last FOMC meeting was unanimous. Mester and Bullard are not voting members this year. However, it will be interesting to see whether policymakers seriously discussed a return to 50 bps rate increases if the softness in inflation proved to be temporary or labor market conditions suggested that the economy could handle bigger hikes. If that’s the case, investors could start thinking about the possibility of a 50 bps hike at the next meeting. The CME Group FedWatch Tool shows that the odds of a 50 bps hike in March currently stand at around 20%, suggesting that there could be an extended USD rally in case the Fed’s publication opens the door to such a decision.

Author

Eren Sengezer

FXStreet

As an economist at heart, Eren Sengezer specializes in the assessment of the short-term and long-term impacts of macroeconomic data, central bank policies and political developments on financial assets.