FOMC minutes break no new ground on policy or bond timing

- Fed officials discuss tapering asset purchases but without timing.

- “Substantial further progress” not yet evident for the whole FOMC.

- Recent market trends continue, S&P sets record, Treasury yields fall, dollar gains.

The Federal Reserve taper discussion is out in the open, but unlike its mention in the April FOMC minutes, which sparked considerable volatility, markets took almost no notice of the commentary.

Minutes of the Federal Open Market Committee (FOMC) meeting on June 15-16 offered no new information on timing or the economic conditions for reducing the amount of bond purchases, running at $120 billion a month since last March.

There was no sense of urgency or agreement that the criteria had been met evident in the edited record of the meeting.

A number of members noted that the US economic recovery was faster than expected and that inflation warranted curtailing policy support.

However, the consensus, or as the minutes put it, "most members", agreed that the criteria first set forth by ChairJerome Powell in the April meeting, of “substantial further progress” had not been met.

Many comments focused on the need “to provide notice well in advance of an announcement to reduce the pace of [bond] purchases.”

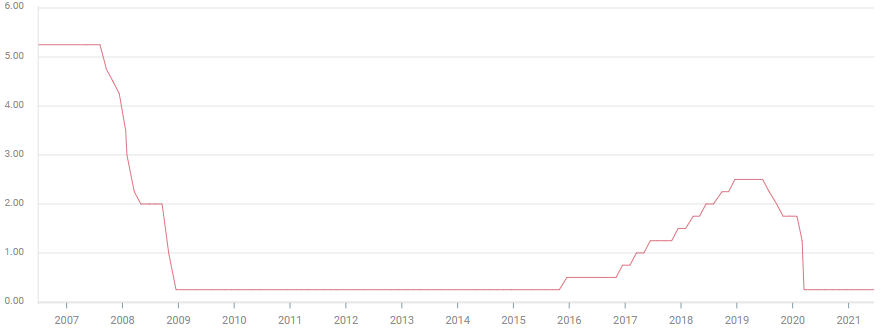

At the June meeting the committee kept the fed fund target range between 0% and 0.25%, where it has been for 17 months and left the bond program undisturbed. This was as universally expected.

Fed funds upper target

Chair Powell's comments

In his press conference following the policy announcement last month, Mr. Powell was somewhat more optimistic on the economy that he had been six weeks earlier.

After the April meeting, Mr. Powell, normally a detailed and fluent talker, had answered almost every question from reporters on bond program timing with when “substantial further progress” had been made.

The phrase was deliberately used to avoid discussing the details of the US economy in relation to the bond program. March Nonfarm Payrolls had just come in at 916,000 and the Fed seemed to fear a credit market sell-off and higher Treasury rates if it spoke approvingly of the recovery. On April 28, the day of the FOMC, the 10-year Treasury yield closed at 1.6200.

At his press conference in June, Mr. Powell spoke a more expansive brief. He went into detail about the FOMC’s thinking on inflation, the labor market, product and material shortages, and the difficulty of forecasting in this highly unusual economic situation.

Mr. Powell mentioned several times the possibility that inflation might be stronger and more persistent than the bank had expected. He acknowledged that officials discussed the taper issue at this meeting.

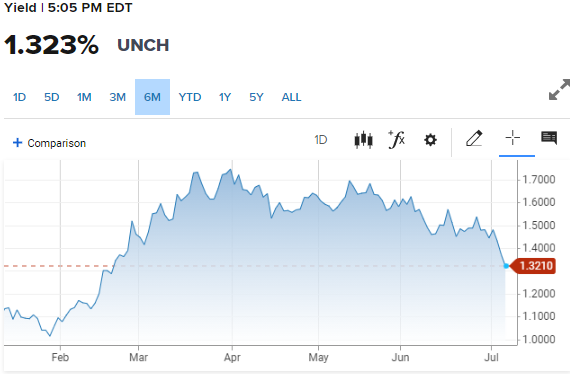

One possible reason for his openness in June may have been the retreat in bond yields. On June 15 the 10-year Treasury yield had closed at 1.499%. The gain of 7 basis points the next day, largely on the improved forecasts in the Projection Materials, was the subsequent highpoint for Treasury yields. The 10-year has since lost 25 points to 1.32% on Wednesday.

10-year Treasury yield

CNBC

Markets

Equities responded to the prospect of continued low rates. The S&P 500 rose14.59 points, 0.34% to 4,358.13, a new record. The NASDAQ added 0.1% to 14,665.0 and the Dow climbed 104.42 points, 0.30% to 34,681.79.

S&P 500

CNBC

Treasury yields continued their decline. The 10-year lost 5 basis points to 1.32% bringing it to its lowest since February. The 30-year dropped 7 points to 1.936%. The 2-year was unchanged at 0.218%.

Bond prices have rallied on concerns that the US economy is slowing, inhibited by labor, product and raw material shortages that are not abating. The employment indexes for the manufacturing and service sectors fell into contraction in June for the first time since last November and December.

The US dollar was mostly higher on the day with the EUR/USD closing at 1.1794, its first finish below 1.1800 since April 2. The USD/JPY was flat, adding just 5 points to 110.66. The USD/CAD was the most active, rising more than a figure to 1.2461. Disarray at the OPEC meeting had dropped West Texas Intermediate (WTI) 4.6% in two days to close at $71.64 on Wednesday.

Conclusion

Each official mention of tapering and the conditions needed serves to inure the markets to the eventual action. The June minutes were another step in making the end of the bond program routine. Further discussion and considerations can be expected during and after the Fed’s annual Jackson Hole policy symposium at the end of August.

The Fed would like nothing more than for the announcement of the first bond reduction to be as uneventful and boring as a community board meeting on sewer replacement.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.