Five fundamentals for the week: Powell's powerful testimony, politics and inflation figures stand out

- Softer US inflation figures are set to encourage markets.

- Fed Chair Jerome Powell will testify before Congress, and may acknowledge weaker Nonfarm Payrolls.

- Speculation about President Biden's candidacy and the next French government are also of interest.

How fast is the US economy slowing? That remains the question for investors, eager to see rate cuts – but fearful of recession. After Nonfarm Payrolls figures showed weakness on Friday, a response from the US central bank and inflation data is of interest. Political distractions remain constant on the agenda.

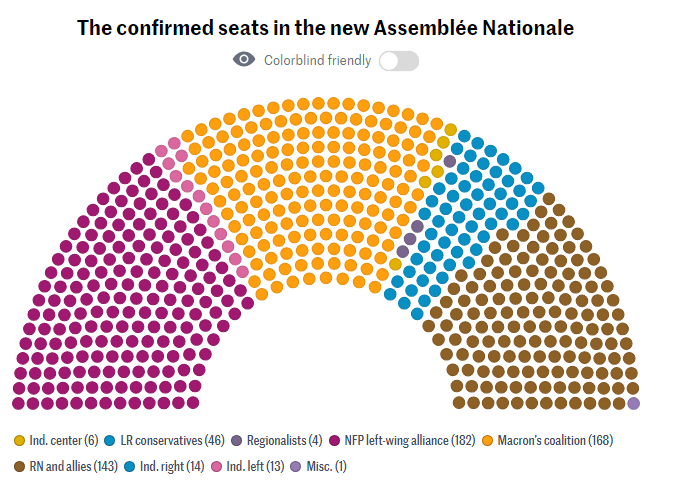

1) French elections fallout set to lift Euro, calm markets

Policies of the populist left are more extreme than those of the extreme right – that was the thinking before the second round of French parliamentary elections. While the left-leaning bloc came out on top, the extremists are far from mustering a majority.

Fragmented French parliament

Composition of the new French parliament. Source: Le Monde

There is a good chance that Europe's second-largest economy will find itself without a functioning government for some time – but it does not mean derailing of President Emmanuel Macron's reforms.

If the electoral blocs disintegrate, moderate left factions could team up with centrist Macron's party and the center-right to form a government with a limited agenda. That would be the best-case scenario for markets.

Assuming the extreme left led by Jean-Luc Mélenchon fails to influence policy, the Euro has room to recover and broader markets to shine.

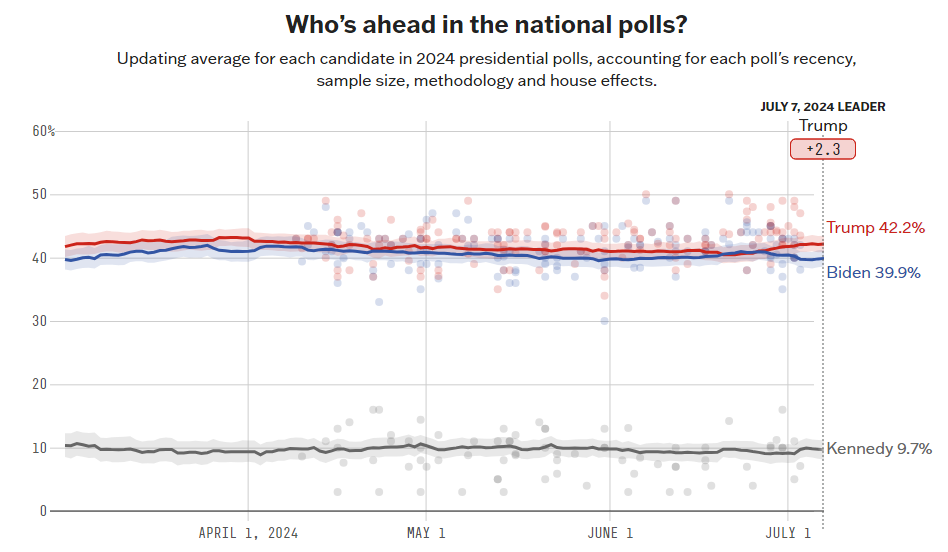

2) Biden to bow out? Speculation moves markets

Only "the Lord almighty" could force President Joe Biden to abandon his bid for a second term. Those are his words – but pressure within the Democratic Party is mounting to find someone else to battle former President Donald Trump.

Trump gains ground against Biden:

National polls. Source: 538

Biden's disastrous debate raised the stakes of a Trump victory – and also a clean Republican sweep. That would enable tax cuts which markets like, but also higher deficits which mean higher interest rates, disliked by investors.

If Democrats rally around Biden and polls continue to show he is losing, yields could rise, weighing on stocks and Gold.

If voices calling him to step aside grow, markets would wobble on uncertainty at first. However, if a moderate Democratic candidate emerges, investors would cheer prospects of divided power, which would mean no extreme deficits nor trade wars.

US politics are usually a sideshow for markets so far from the vote in November, but doubts over Biden put the topic high on the agenda with more than four months to go.

3) Powell to acknowledge labor market jitters

Tuesday, 14:00 GMT, and Wednesday, 14:00 GMT. While politicians think about the elections, they still have to fulfill their oversight duties – which includes grilling Federal Reserve Chair Jerome Powell. In his appearance before lawmakers, the world's most powerful central banker is set to call for more patience before cutting interest rates, reiterating his mantra.

However, he may acknowledge some weakness in the labor market, mostly seen via the gradual increase in the unemployment rate to 4.1% as of June. He previously linked reducing borrowing costs to "unexpected weakness" in jobs. Is the employment situation worrying? Probably not, not yet, but any comments about it may boost markets expecting interest rate cuts.

Powell will surely discuss inflation as well – the bank's current focus. Price rises have decelerated, but they are far from being satisfactory. With inflation on the public’s agenda, politicians will likely push Powell on the topic. If he sees the glass half full, defying pressures, markets would cheer, while any pledge to fight inflation to the bone would cause fear.

4) Core CPI expectations too narrow, any 0.1% up or down may trigger an explosion

Thursday, 12:30 GMT. The Consumer Price Index (CPI) report is the #1 market mover. The Fed is focused on inflation, and CPI is the first release of hard data on the topic. Core CPI, which excludes volatile food and energy prices, is set to have risen by 0.2% MoM in June and 3.4% YoY. That would be a repeat of May's data.

Core CPI YoY. Source: FXStreet

Any 0.1% deviation from the data would have substantial consequences. A small miss would raise hopes of an early rate cut, sending stocks and Gold up while weighing on the US Dollar. A small beat would trigger worries about higher rates for longer, causing markets to take the other direction.

Until inflation stabilizes around 2% yearly for some time, the CPI report will have more influence than Nonfarm Payrolls.

5) PPI set to cause some confusion before trading ends for the week

Friday, 12:30 GMT. While CPI is more important and has more influence, the Producer Price Index (PPI) is also of importance. Some see it as inflation in the pipeline. Moreover, it is released on Friday, as investors close a turbulent seven days, including Nonfarm Payrolls, CPI, and Powell's speech.

Core PPI is marginally off the lows:

Core PPI YoY. Source: FXStreet.

Even if the data is not outstanding, the mere publication tends to unleash price action. A small beat or miss could trigger a knee-jerk reaction, which would then be reversed & and a potential trading opportunity.

Core PPI YoY is set to rise to 2.5% in June after 2.3% in May. I think there is room for a small miss.

Final thoughts

A mix of top-tier data, the world's most important central banker, and political headlines that can erupt at any moment imply high volatility.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.