Fed preview: Rate cut on deck, but with 2025 caution

Key points

-

25bp rate cut expected: The Fed is set to cut rates to 4.25%-4.50%, but it may signal caution on further easing.

-

Dot plot adjustments: The 2025 dot plot could shift to signal only three cuts, with fewer cuts expected further in 2026 as well. This would make the December rate cut a hawkish one.

-

Market implications: Hawkish guidance could support tactical USD strength and challenge equity valuations, but strategic bets still remain in favor of US dollar and US equities heading into 2025.

The Federal Reserve is widely expected to deliver a 25 basis-points (bps) rate cut this week, reducing the target range for the federal funds rate to 4.25-4.50%. With the Fed's moves becoming more data-driven, investors will be paying close attention to the tone of Chair Powell’s post-meeting remarks and the updated Summary of Economic Projections (SEP), especially the dot plot, which provides insights into the rate path for 2025 and beyond.

Rate cut this week: A 'hawkish' cut?

The Fed Funds futures show a 95% probability of a 25bps rate cut at the December meeting, following a similar move in November. This could come on the back of:

-

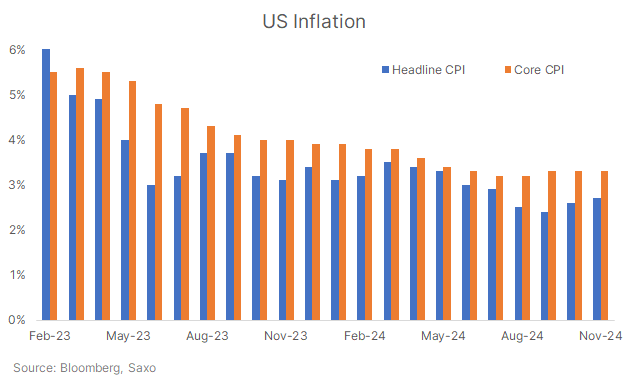

Labor market softening: The unemployment rate has edged higher to 4.2% in November, while labor force participation declined. This slowdown in job market strength could justify additional rate cuts to prevent excessive labor market slack.

-

Easing shelter inflation: While the last mile of inflation has been proving sticky, there was a sense of relief in housing inflation in the latest update. Shelter costs, a key driver of inflation, have started to ease as new rental leases are renegotiated. Since shelter has been a sticky component of inflation, any relief here strengthens the case for rate cuts.

While the rate cut is almost fully priced in, the market will be watching for any signals of a "hawkish cut." This means that while the Fed is easing policy, it could signal caution about the pace of future cuts, either through the committee’s updated dot plot or via Chair Powell’s press conference.

2025 rate path: Will the Fed pause?

There’s growing chatter about the Fed possibly skipping a rate cut in January 2025, signaling a potential pause in the easing cycle. Why might this happen?

-

Sticky inflation: While shelter inflation is easing, other components of inflation remain persistent, complicating the Fed's ability to justify an aggressive pace of cuts.

-

Resilient economy: Recent economic data has shown surprising resilience, which may prompt the Fed to take a more measured approach in cutting rates further.

-

Trump-flation risks: With the new Trump administration likely to focus on trade tariffs early on after taking office on January 20, there is risk that it could create upside risks to inflation, which could make the Fed more cautious about future cuts.

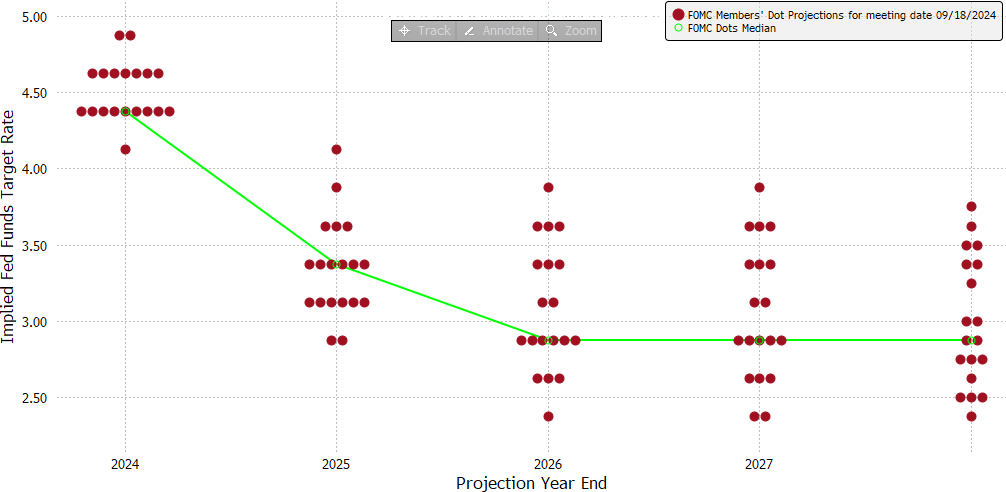

The dot plot, which reflects each FOMC member’s rate expectations, will be critical for market sentiment as it gives insights into the Fed members’ thinking. The dots for 2025, 2026, and 2027 will provide clues on how aggressively the Fed sees rates coming down.

-

2025 outlook: The previous dot plot indicated four rate cuts (100bps) for 2025, but this could be revised to just three or even two cuts as inflation risks remain elevated. Consensus expects 2025 dot to move to 3.625% from 3.375%, signalling a baseline view of three rate cuts next year. If the 2025 dot moved to 3.875%, signalling just two rate cuts next year, that will be a considerable hawkish surprise for the market.

-

Longer-term rates: Projections for 2026 could also shift to two cuts, reflecting a slower normalization path. Consensus expects end-2026 rate to be at 3.125% from 2.875% projected by the dot plot in September.

-

Terminal rate: The "long-run" neutral rate could also tick higher to 3% from 2.875% in September, reflecting a structurally higher interest rate environment.

-

Updated economic forecasts: The SEP is likely to be revised to show higher 2024 core PCE inflation from 2.6% in September, lower unemployment from 4.4%, and stronger GDP growth projections for 2024.

Source: Federal Reserve (Sept 2024 meeting)

Market implications and portfolio strategies

Equity market reaction: Markets have priced in the 25bps cut, but if the Fed signals fewer cuts in 2025, risk assets like equities may see renewed volatility. A hawkish tone could put downward pressure on equity valuations, especially growth stocks that are more sensitive to higher rates. Other interest rate-sensitive sectors, such as homebuilders and small-caps, could also face headwinds. Investors may consider rotating into defensive sectors like utilities and consumer staples if the Fed signals a slower pace of cuts.

Fixed income positioning: If the dot plot hints at a higher terminal rate or fewer cuts in 2025, the yield curve could bear flatten, with short-term yields rising relative to longer-term yields. This could expose short-duration bonds to downside risk as yields rise.

FX strategy: A hawkish rate cut could be USD-supportive, driving demand for the dollar. While there’s potential for a short-term pullback in USD due to year-end seasonality and stretched positioning, any dips may be seen as a buying opportunity. The Trump administration’s potential pro-dollar policies, such as heightened tariff talks, could support the USD in 2025. Meanwhile, Japanese yen faces downside risks if US 10-year yields jump higher, and tariff threats could weigh on the Chinese yuan, euro, and Australian dollar heading into 2025.

Read the original analysis: Fed preview: Rate cut on deck, but with 2025 caution

Author

Saxo Research Team

Saxo Bank

Saxo is an award-winning investment firm trusted by 1,200,000+ clients worldwide. Saxo provides the leading online trading platform connecting investors and traders to global financial markets.