Fed funds traders happy to ignore US government shutdown

Outlook:

We can gnash our teeth about a ridiculous state of affairs in Congress and an incompe-tent president, but as we see from this morning's prices, markets don't much care. Government shutdowns last from one to 17 days and average 3 or 4 days, depending on how you count. The White House answering machine blames the Dems in an offensive way, with the Dems having a more coherent story, but never mind—the public will blame whomever they choose regardless of facts. El-Erian has a piece in Bloomberg about why political events are undervalued or ignored by markets. The one we like is that political disruptions do not affect earnings (in the West, anyway).

While the market may not care about shutdowns—and there is another vote at noon today—they do care about default. We're not there yet, but inability to fund the government leads to inability to pay interest on the debt at some point. At a guess, TreasSec Mnuchin is studying the Rubin playbook.

What they do care about is the Fed, and unless and until Mr. Powell makes any changes upon taking over from Yellen in February, that's a steady picture. In fact, the CME FedWatch tool has the probabil-ity of the March hike rising from 71.8% on Friday to 72.6 today. A week ago it was 66.5% and a month ago, 61.5%. It's as though Fed funds traders are perfectly happy to ignore Washington.

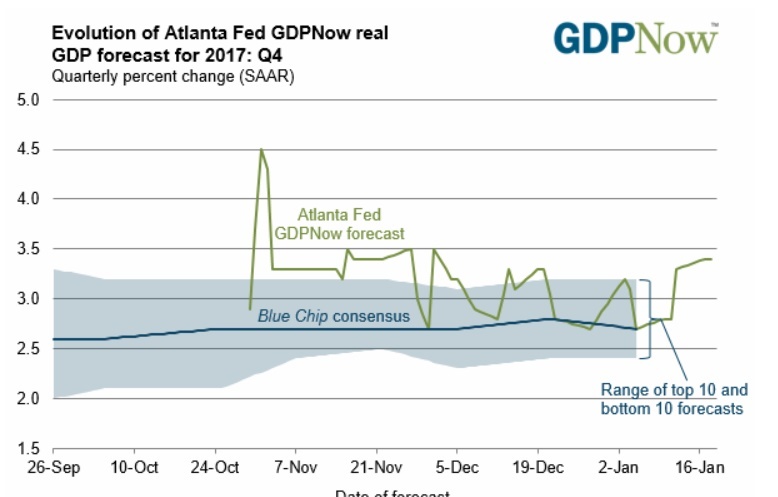

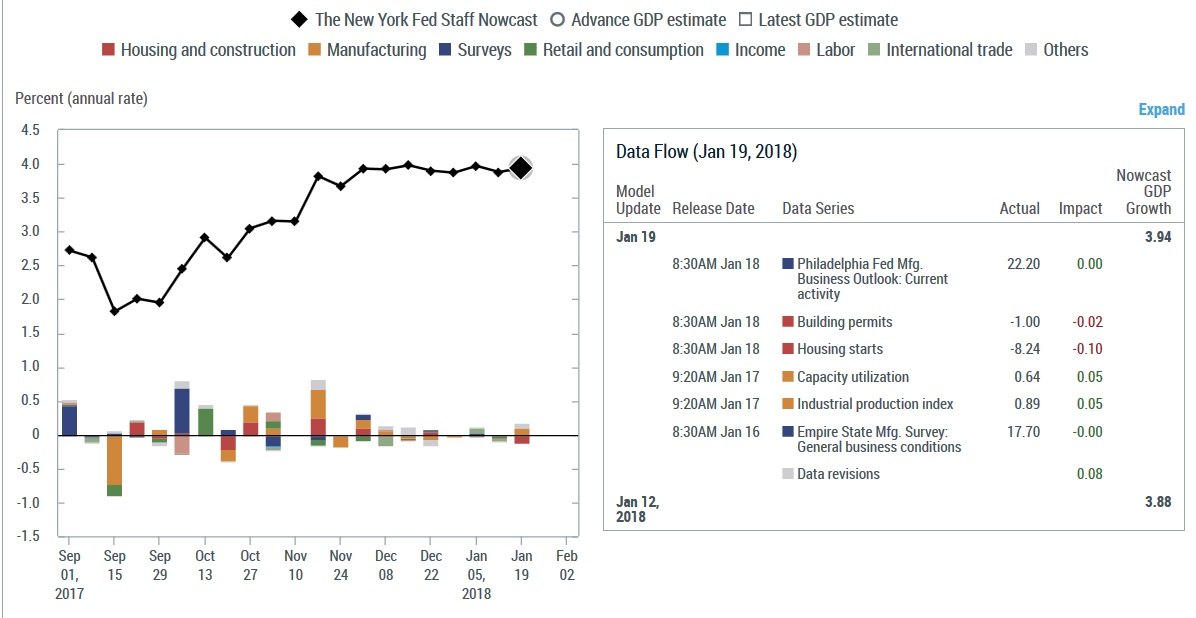

Traders do like data, though, and this Thursday we get Q4 GDP again, forecast at 3.4% last Thursday by the Atlanta GDPNow gang and possibly still rising. The NY Fed NowCast has 3.9% as of Friday (if fall-ing back to 3.1% in Q1). In fact, Thursday is an enormous data day—see the calendar. We get trade and new home sales, among other things (like jobless claims). Some of this data, possibly including GDP, will not be released on schedule if the government is still shut down. The statisticians will be on unpaid leave.

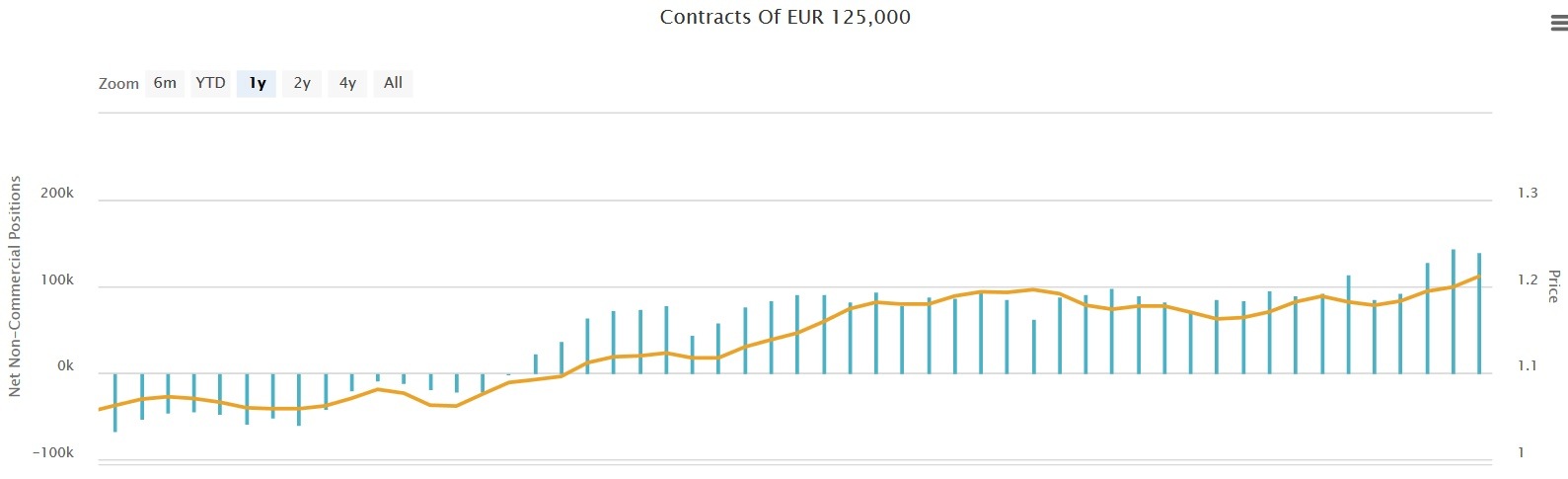

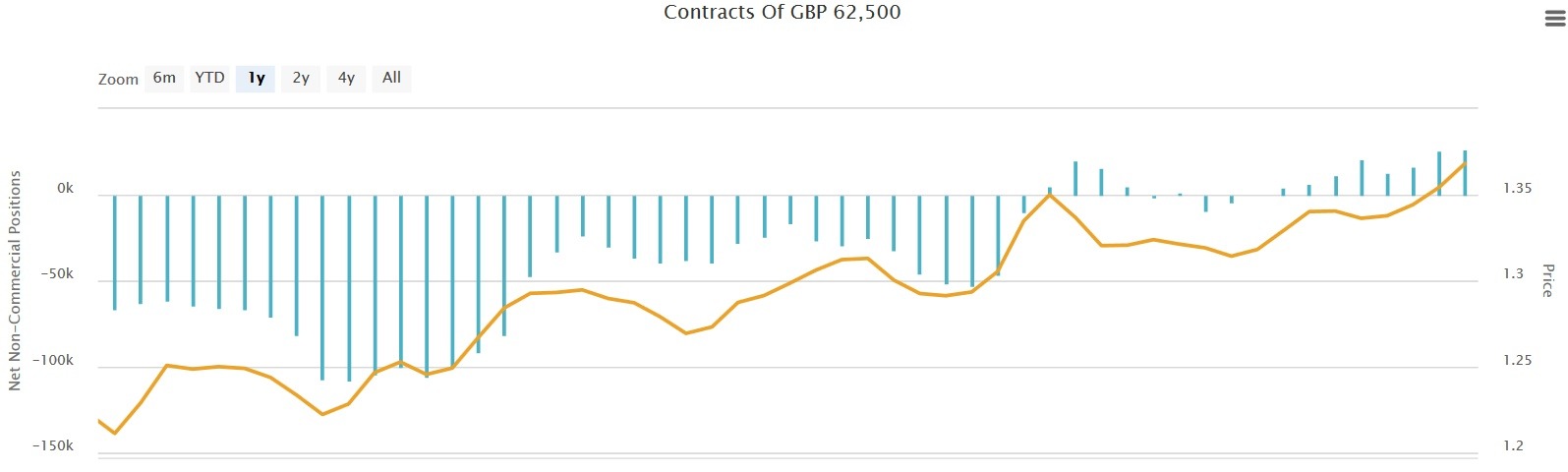

The Commitments of Traders reports show some remarkable shifts. See the euro gains over the past year. Reuters reports UBS today upgraded the euro from 1.18 to 1.25 for the next three months. The sterling COT chart is even more remarkable.

Bottom line, we may suspect that the dollar is oversold and many indicators show it that way, but de-mand for other currencies is continuing to manifest itself. We may get a pop when the shutdown is end-ed, but it will probably be short-lived. The canary is chirping merrily.

And finally, the eurozone finance ministers will discuss ending the last Greek bailout this week and Greece is already well ahead in preparations to re-enter the bond market for the first time since 2010. The FT has a cautionary tale about this. It might not be as "seamless" as Greek politicians hope.

And yet some indicators are wildly positive. "The yield on two-year Greek bonds fell below that of the equivalent US government paper earlier this month, as the global economic recovery saw investors re-pricing Treasury debt and shifting into equities in anticipation of rising interest rates. While this is not the most apposite direct comparison — Europe's risk-free rate is the German Bund, which remains deeply in negative territory at the two-year maturity — it is nevertheless a startling illustration of the extent to which market jitters about Greece have eased. With even Bund yields beginning to rise, how-ever, the recovery in the price of Greek bonds may not have much further to go." The Athens stock market has yet to catch up, though.

Greece has aggregated existing debt into different tranches and issued some short-term paper, but still seeks further debt relief, something the IMF insists is necessary but the EU resists. But Greek debt is equal to184% of GDP in the coming year. Eek. The FT notes that "Nearly three-quarters of Greece's outstanding debts are held by other eurozone countries — including via the bloc's rescue funds, the European Financial Stability Facility and the European Stability Mechanism. This helps to explain why Greek bond prices are doing so well — because very little of it is in private hands and even less trades regularly. Although Greece is now attempting to increase the liquidity of its debt by consolidating ex-isting paper and planning new issuance to reach the market later this year — the scale is dwarfed by the amounts held by non-trading creditors."

At a guess, the finance ministers are not going to be in the mood to give debt relief to Greece. The cur-rent situation is still whistling past the graveyard. And yet nobody is talking about big-time turmoil again. It ain't over, but it's over.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes. To see the full report and the traders’ advisories, sign up for a free trial now!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat