Fading US consumer confidence intensifies the Fed’s inflation dilemma

- Michigan Consumer Sentiment falls to a fresh 10-year low in October.

- Real wages have fallen for seven straight months.

- Retail Sales and Personal Spending have yet to drop with sentiment.

Americans hate inflation. Every time they go to the supermarket, consumers can see their paychecks shrink. For seven straight months, rising prices have outpaced wages. It should be no surprise that for half of that time consumer optimism has languished at a decade low despite a job market that is begging for workers and willing to pay for them.

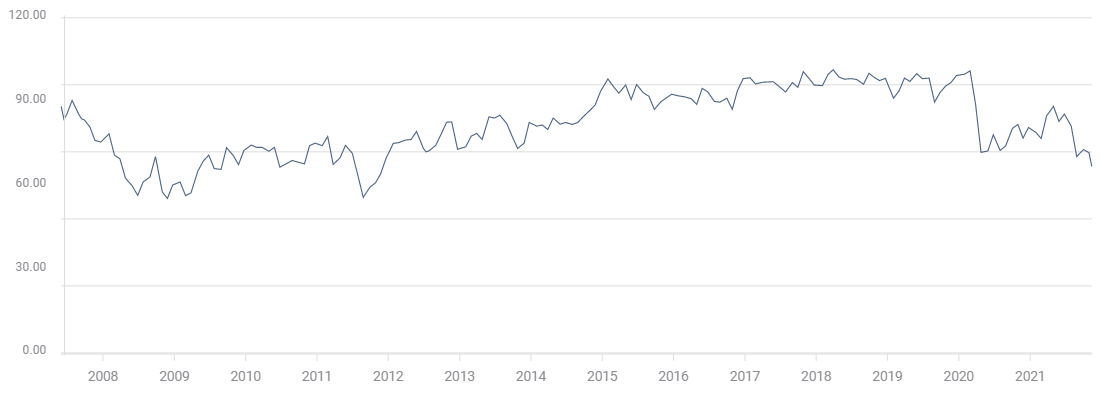

The University of Michigan Consumer Sentiment Index unexpectedly dropped to 66.8 in October from 71.7 in September setting a new 10-year low, the third in the last four months. Analysts had forecast a small increase to 72.4. Over the past four months, the Michigan Index has averaged 70.4.

Michigan Consumer Sentiment

Labor Market

The number of US positions on offer in the Job Openings and Labor Turnover Survey (JOLTS) has averaged 9.9 million for seven months. That is more than two million more than the previous monthly high of 7.6 million in November 2019. Hiring in the Nonfarm Payroll accounts has averaged 592,000 for that period. These are the best numbers since the initial recovery from last spring’s lockdown.

JOLTS

FXStreet

A record 4.4 million workers quit their jobs in September seeking different or better-paid employment. These voluntary separations reflect worker confidence in finding a more lucrative or more congenial job and the growing pricing power of employees in a very tight labor market.

These labor market statistics favor workers over employers and cannot be the source of consumer discontent.

Wages and inflation

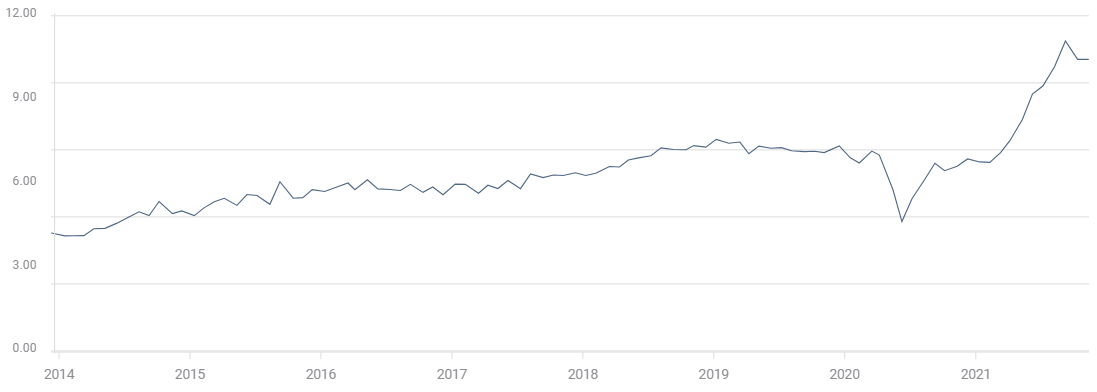

Despite the nationwide shortage of workers, wage increases have not kept pace with soaring inflation. Annual real income (wages minus inflation) have fallen every month since March. Average Hourly Earnings (AHE) have averaged a 3.9% annual gain for those seven months and have climbed from 0.4% in April to 4.9% in October.

Average Hourly Earnings (YoY)

FXStreet

Annual CPI inflation has averaged 5.3% for the same period. Americans have lost 1.4% of their purchasing power in a little more than half a year.

CPI (YoY)

FXStreet

The overall inflation and wage statistics understate the impact of inflation on most families because the prices for some necessities, particularly cars, gasoline and fuel, have risen far faster than the general inflation rate.

Consumer Sentiment, Retail Sales and Personal Spending

Retail Sales have been essentially flat over the past six months from April, averaging 0.07%, though they were stronger in August and September at 0.9% and 0.7%. October’s figures will be reported on Tuesday November 16 and are forecast to be unchanged at 0.7%.

Retail Sales

FXStreet

If the October projection is accurate, given the sentiment numbers hardly a guarantee, Retail Sales will have averaged 0.8% for the three months of weak consumer outlook, August through October.

Personal spending has been stronger than sales for the half-year through October averaging a 0.6% monthly increase. August and September were the strongest consecutive months of the six, averaging 0.8%. November’s spending result will be reported in two weeks on November 24.

Personal Spending

The US economy expanded at a 2% annualized rate in the third quarter with a 0.17% monthly increase in Retail Sales and a 0.5% average for Personal Spending.

The Atlanta Fed GDPNow estimate for the fourth quarter, based on the limited data available, is 8.2%. The next revision will be after October's Retail Sales on November 16.

Consumer Sentiment has been weak for four months, averaging 70.4 from August. Sales and spending numbers have been released for only two of those months, August and September. The identical averages of 0.8% for sales and spending show no evidence that the trough in sentiment has had an effect on consumption.

Whether consumers will continue to spend in the fourth quarter as inflation increasingly appears to be a long-term prospect is unknown. What is certain is that a drop in consumption from third-quarter levels will register far slower economic growth.

Market response

Weak Consumer Sentiment numbers are normally a negative indicator for Treasury yields and equities. The logic flows from poor sentiment and falling confidence to fading consumption, lower economic growth and eventually lower interest rates.

Friday’s markets took the opposite tack. Treasury rates rose across the board. The gains were small, 1.2 basis point in the 10-year, 2 in the 30 and 1.5 in the 5-year, but coming after Wednesday’s powerful yield rally, it is an indication that credit traders do not expect the weakening sentiment numbers to deter the Fed’s taper schedule.

US 10-year Treasury yield

CNBC

Equities were higher, with the Dow rising 0.5%, the NASDAQ 1% and the S&P 500 adding 0.72%. Stocks are taking their cues from the third quarter's consumption figures and the obvious fact that consumers have not yet taken their inflation discontent shopping.

The dollar was higher on the week in every major pair. The surge in Treasury rates was the last word for the greenback.

-637723589200878800.png)

The Fed’s dilemma

The worst possible outcome for the Fed’s taper program is for collapsing consumer attitudes to take a large bite out of consumption and GDP.

Dislike of inflation is the most likely culprit behind the plunge in consumer sentiment. The longer inflation continues at current levels, the greater the chance that households begin to adjust spending to their diminished purchasing power.

In an extremely tight job market with widespread labor shortages, inflation exacerbates demands for higher wages which in turn forces employers to raise their own prices, driving both sides of a wage-price spiral.

The Federal Reserve has underestimated the strength, duration and causes of US inflation. Far from price increases being a temporary effect of the lockdown plummet in consumption, global dislocations in supply, manufacturing and distribution, worker reluctance and unprecedented deficit spending from Washington, have created a near-perfect storm of inflationary pressures.

Unchecked price increases are a far greater threat to consumer outlook, spending and the economic recovery than rising Treasury yields.

It is too late for the modest recent gains in Treasury yields and commercial rates to have any impact on the next six months worth of inflation. If the Fed does not begin to curb the monetary impulse for inflation, the following six months could be even worse.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.