European stocks suffer third wave; will the ECB react?

Outlook:

We have been complaining for most of the year that the stock market is divorced from reality and turning a blind eye to the economic consequences of the pandemic, so when it does finally seem to be doing exactly that, we feel confused. It's the European exchanges suffering the most, but maybe equity analysts are blinded by their own self-importance and missing the critical point—the ECB response.

The ECB meets Thursday and can pat itself on the back a little for getting stability in some areas, including a small increase in money supply and bank lending. The question is whether more is needed right now because of the second wave or more would not be sensible; many analysts expect no fresh action until the Dec meeting when new forecasts are due from the backroom boys, aka economists. One idea might be ECB guarantees of new loans to business, and another is a second long-term loan program. The BBK squawks but does not rule, at least not in a pandemic.

In the US, we get a ton of "high-frequency" data today, including Aug house prices, Sept durable goods orders, and Oct Conference Board consumer confidence. The Richmond Fed delivers the manufacturing survey. All the US data is forecast to show improvement over the previous month, with only the Richmond Fed fading a little.

Again, the biggie and less-frequent number is Q3 GDP on Thursday. As we all know to our rue, that are 87 ways to display the statistics. The Atlanta Fed has 36.3% as of Oct 20. The New York Fed has 13.7%, falling back to 3.5% in Q4. A lot depends on whether the numbers are year-over-year or annualized. TradingEconomics.com shows Q2 at a 9% annual contraction rate, so a 7% expected rise from there would appear nice. Appearances can deceive, of course.

Just as ideas about the ECB may be behind the euro's performance and not the pandemic surge directly, we await the Bank of Japan overnight, the Bank of Canada tomorrow and the Bank of England next week.

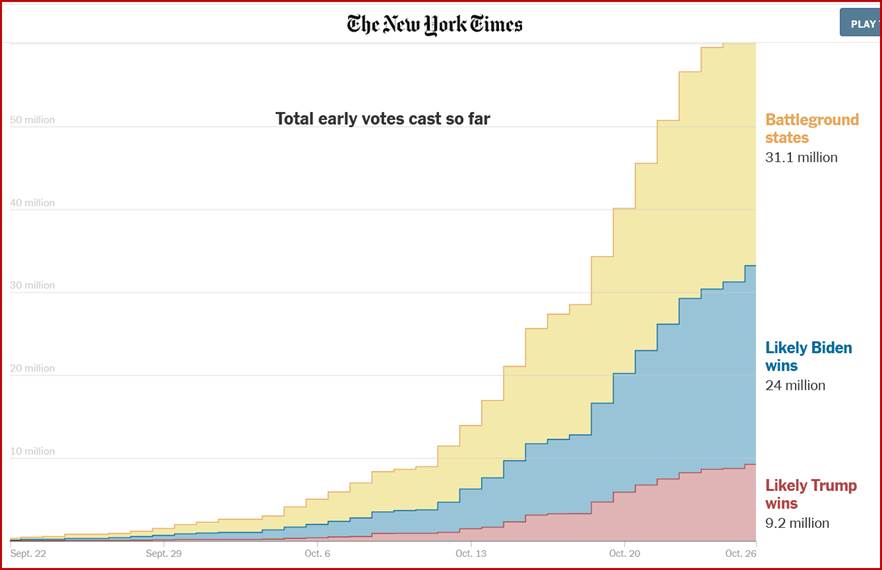

Then there is the election. Only if it's landslide does Trump concede, and probably not even then. Tigers and stripes. Trump likes to make noise and air grievances, and nobody expect the country after Nov 3—one week!—to be quiet and normal. Even after he does concede, he has 97 days to inauguration to make messes. We assume a Biden win for a number of reasons, not least that Trump's 2016 win was a fluke and largely dependent on Dems staying home our switching sides because Clinton was unlikeable and deemed untrustworthy. The deeper reason is that most voters know Trump is incompetent and erratic, and he lies. They may not mind if he lies about Mexicans but are thought to care a lot that he lies about Covid-19.

See the chart from the NY Times. A return to normalcy, blessedly boring, seems to be in the cards—unless Trump can pull an inside straight again.

At a guess, we will get a return to risk-off and dollar sell-off. That's unless Trump comes up with a Shock or one of the other central banks surprises.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat