EUR/USD Weekly Forecast: US Dollar reaffirms its dominant role

- The Federal Reserve and other central banks pledged to higher for longer, markets fret.

- Euro Zone economy keeps contracting as the ECB cannot find a balance.

- EUR/USD slid not yet over, break through 1.0600 likely in the near term.

The EUR/USD pair maintained the bearish path, bottoming on Friday at 1.0614, the lowest since last March. The pair heads into the weekend, trading a handful of pips above the level as investors continue to bet on the US Dollar.

The Euro advanced throughout the first half of the week, partially helped by profit-taking but also amid a scarce macroeconomic calendar and a better market mood. However, EUR/USD gains were limited ahead of the most relevant event of the week, the United States (US) Federal Reserve (Fed) monetary policy announcement.

Federal Reserve delivers hawkish pause

As expected, the Federal Open Market Committee (FOMC) left the benchmark interest rates unchanged at 5.25% – 5.50%. Inflation in the US has persistently exceeded the central bank’s target range and even ticked higher in August but is way below the record highs posted in mid-2022. The Fed can take a wait-and-see stance and reap the benefits of aggressive monetary tightening. Still, the central bank did not sit back. Chairman Jerome Powell highlighted the FOMC’s commitment to maintain rates higher for longer, meaning the tightening cycle could be almost over, but rate cuts are not yet in sight.

Fresh Economic Projections showed policymakers believe inflationary pressures will continue, and hence, left the door open for another rate hike. Furthermore, potential rate cuts for 2024 are now estimated at 50 basis points (bps) against the 100 bps foreseen in June. Additionally, they expect growth to slow next year to 1.5% from 2.1% this year, while the unemployment rate is seen not higher than 4.1%. Still, these projections are closer to hope than scientific calculations.

Finally, Powell said that a soft landing is a “plausible outcome” but clarified he does not see it as a baseline scenario. “Ultimately, this may be decided by factors outside of our control at the end of the day, but I do think it’s possible,” Powell said. “I also think this is why we are in a position to move carefully again. We will restore price stability, and we know we have to do that, and we know that the public depends on us doing that.”

The Fed’s announcement benefited the US Dollar, as investors got spooked and sought safety in the safe-haven currency. The EUR/USD pair was trading around 1.0730 ahead of the event, shedding over 100 pips afterwards.

More central banks in the on-hold path

The Bank of England (BoE) also announced its monetary policy decision this week and partially surprised investors by keeping rates unchanged. Financial markets somehow anticipated the possibility after the United Kingdom (UK) Consumer Price Index (CPI) came in below expectations for August, but still, the news benefited the USD. Like their American counterparts, UK policymakers leave room for more hikes and pledged to higher for longer.

Finally, the Bank of Japan (BoJ) unveiled its decision on Friday. Despite former hints from Governor Kazuo Ueda on a potential shift to a “quiet exit,” the central bank introduced no changes to the ultra-loose monetary policy, and neither suggested a change is on the table. For sure, it was no surprise, but it was yet another disappointment for speculative interest.

Where are we?

Probably the most notorious behavior was that of US Treasury yields. Yields were on the run ahead of the Fed’s announcement, but that of the 2-year note soared to 5.20%, its highest in almost two decades, after the announcement. It currently stands at 5.11%, while the 10-year note offers 4.46%. The inverted curve widened, indicating mounting concerns about an economic setback.

Furthermore, the US released Initial Jobless Claims data on Thursday, which came in much better than anticipated at 201K for the week ended September 15, suggesting the labor market is still far from cooling.

The monetary policy tightening cycle is “almost” over but lasting much longer than what anyone could have anticipated a year ago. Global policymakers won’t let it go, as inflation has largely surpassed previsions while labor markets remain quite tight. True, the US economy is proving to be resilient and in much better shape than that of its major counterparts.

The US Dollar may benefit from fears lately, but it is also becoming attractive on its own. Regarding EUR/USD, the Euro Zone is closer to the bottom of the list of economic performance. Furthermore, the European Central Bank's (ECB) decision to hike rates by 25 bps earlier this month has spurred rage among local governments amid worsening living conditions.

Furthermore, S&P Global released the preliminary estimates of the September PMIs, and the report brought more bad news. “The eurozone private sector remained in contraction at the end of the third quarter of the year as waning demand led to a further decline in activity,” the official report reads. Manufacturing output index contracted to 43.4, while services activity posted a modest improvement but the index remained below 50, reaching 48.4. The Composite PMI resulted at 47.1, the highest in two months. The report also noted that, despite weak demand, “input costs continued to rise sharply, and the rate of inflation even picked up from that seen in August.”

US figures, on the other hand, indicated a tepid contraction in manufacturing as the index printed at 48.9 from 47.9 in August, while services output stood at 50.2, slightly below the previous 50.5 but still within expansionary levels. The S&P Global Composite PMI was confirmed at 50.1.

Inflation under scrutiny, once again

The calendar will feature next week critical inflation data. Germany will publish on Thursday the preliminary estimate of the September Harmonized Index of Consumer Prices (HICP), foreseen to be sharply lower than the final August readings. The annual HICP is expected at 4.6% from 6.1% previously, while the core yearly reading is anticipated to print 4.7% vs. 6.4% the month before. The EU will offer the HICP for the same period for the whole Union, also seen easing, although at a slowest pace.

The US will release the August Personal Consumption Expenditures (PCE) - Price Index, the Fed’s favorite inflation reading. Besides inflation figures, the country will release the final estimate of the Q2 Gross Domestic Product (GDP).

EUR/USD technical outlook

The EUR/USD pair is closing in the red for the tenth consecutive week and continues to post lower lows, hinting at persistent selling pressure in the coming days. Corrective advances so far have not lasted long, and a more relevant one seemingly will need to wait.

The weekly chart shows that a bearish 100 Simple Moving Average (SMA) provided dynamic resistance, maintaining its bearish slope at around 1.0730. The 20 SMA, in the meantime, gains bearish traction above the longer one, in line with persistent selling interest. Meanwhile, the Momentum indicator heads firmly south within negative levels, while the Relative Strength Index (RSI) indicator consolidates at around 41, skewing the risk to the downside.

In the daily chart, the pair is developing below all its moving averages, with the 20 SMA extending its slump below the longer ones, currently standing at 1.0737, reinforcing the resistance area. The Momentum indicator resumed its decline below its 100 level, while the RSI indicator keeps grinding south at around 36, favoring a bearish breakout of the 1.0600 threshold.

The next bearish target and a relevant support level is 1.0515, the March monthly low, while a break below the latter could see the pair edging towards the 1.0420/40 price zone. As said, the 1.0730 area offers strong resistance, with a break above it exposing the 1.0800 mark.

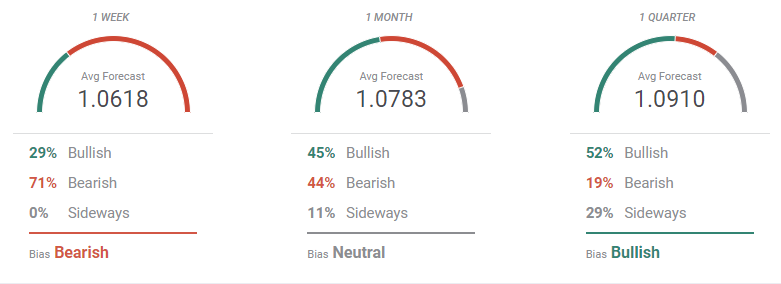

EUR/USD sentiment poll

According to the FXStreet Forecast Poll, EUR/USD will remain under pressure in the near term, with 71% of the polled experts betting for lower levels in the weekly view. The pair is seen averaging 1.0618 in the upcoming days, with growing odds for a bullish correction afterwards, as in the monthly perspective, bulls and bears are pretty much equal, but the average target rises to 1.0783. Finally, a more bullish view is clear in the three-month outlook, with bulls up to 52% and bears down to 19%, resulting in an average target of 1.0910.

The Overview chart, however, suggests the risk remains skewed to the downside. The three moving averages head south with increased downward strength. More relevantly, the largest accumulation of targets is between 1.0400 and 1.0600 in the three cases, although there’s a wide range of possible targets above the current price zone.

Author

Valeria Bednarik

FXStreet

Valeria Bednarik was born and lives in Buenos Aires, Argentina. Her passion for math and numbers pushed her into studying economics in her younger years.