ECB Preview: Another hike, but what next?

- Following the Fed, the ECB will be the next central bank to decide on interest rates.

- A 25 basis point interest rate hike is expected, along with a hawkish tone.

- The focus is on what the ECB will do after July.

On Thursday, July 27th, the European Central Bank (ECB) will announce its monetary policy decision at 12:15 GMT. Later, at 12:45 GMT, ECB President Christine Lagarde will hold a press conference.

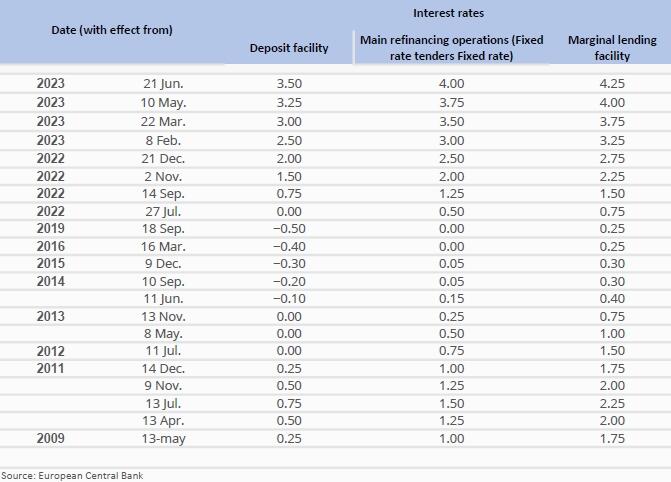

At the June meeting, the ECB raised its key interest rates by a quarter of a percentage point. It was the eighth consecutive hike, with the Deposit facility rate rising to 3.5%, the Main refinancing operations up to 4.0% and the Marginal Lending Facility to 4.25% – their highest levels since May 2001. The hike took place despite reports suggesting evidence of contraction in most Eurozone countries but with inflation remaining elevated. At that meeting, Lagarde said that another rate hike at the July meeting was “very likely”.

Even after the meeting Lagarde and other ECB members continued to indicate that another rate hike was likely. Markets listened, and came to expect the ECB to deliver another rate hike. This time, however, there has been no doubt about the size – whereas previously there had been speculation of a 50 basis point hike, this time markets foresee only a 25 basis point increase. The more pressing question for markets now is what the ECB will do after July.

The key justification for the rate hike was reiterated in the June statement, where the ECB explained that “inflation has been coming down but is projected to remain too high for too long”.

Euro-area prices rose 5.5% year-over-year in June (the lowest level since early 2022), below the 6.1% recorded in May and the 7% of April. The inflation trend is downward; however, it remains far from the ECB’s 2% target. While the CPI remains above the target and particularly at a level below key interest rates, the bias at the ECB will remain towards more tightening, considering the current context.

Focus on the September decision

With a 25 basis point rate hike practically guaranteed this week, the focus turns to the September 14 decision. The latest round of comments from Governing Council members shows that another hike is not a done deal, and the decision, as of now, looks to be a close call.

While the minutes from the June meeting and comments mention that raising rates again in July is a “necessity”, what the ECB will do in September is not certain at the moment. Before the September meeting, there will be two inflation reports. The July data starts to come out this Friday, with preliminary readings from Spain and Germany. On Monday, July 31, Eurostat is scheduled to release the flash estimate of Eurozone inflation data for July. Before the September ECB meeting, the August inflation numbers will also be released.

How much more the ECB can tighten its monetary policy is the outcome of the balance between high inflation and rising wages, on one side, and the evidence of weaker growth on the other. A pause in September would not necessarily mean it is the end of the hiking cycle. The end of the cycle requires more evidence of inflation slowing down toward the target (with inflation readings below interest rate levels) and a deterioration in the growth outlook. The central bank will be more data-dependent going forward.

Positive for the EUR?

The ECB wants to show a strong commitment to returning inflation to its target, and such a scenario is already expected. A hawkish surprise to lift the Euro would require at least Lagarde mentioning that a September hike 'is very likely' and talking with more determination about higher interest rates for longer – and markets would have to buy that message.

The level of terminal rates is being debated among analysts. If the ECB offers signs of higher terminal rates, then the Euro could benefit across the board, sending Eurozone bond yields higher. An unlikely dovish response should trigger a rally in equity markets but would weigh on the common currency.

However, what happens with EUR/USD over the next few days is most likely to be driven by US Dollar dynamics, with the FOMC decision on Wednesday and key data due on Thursday and Friday.

The weekly chart shows the EUR/USD retreating from the year-to-date high, still above a short-term uptrend and well above the 20-week Simple Moving Average (SMA). If, after all the central bank meetings and economic reports of the week, the pair holds above current levels or higher, a resumption to the upside looks like a matter of time. A strong signal about more gains ahead would be provided by a weekly close above the 200-week SMA that currently stands at 1.1190. On the contrary, under 1.0950, the outlook for the Euro would deteriorate, exposing the 20-week SMA at 1.0900. A weekly close below that should add pressure to the downside.

-638258885536675576.png)

Author

Matías Salord

FXStreet

Matías started in financial markets in 2008, after graduating in Economics. He was trained in chart analysis and then became an educator. He also studied Journalism. He started writing analyses for specialized websites before joining FXStreet.

![How Wall Street rigs the game [Video]](https://editorial.fxsstatic.com/images/i/market-chaos-01.jpg)