Dollar stronger again with notable yen weakness continuing

Market Overview

The impact of prospective higher US inflation rippled through markets yesterday as the US dollar surged higher in the afternoon. The higher than expected US Producer Prices Index (PPI) comes ahead of today’s consumer prices data, the CPI, which is expected to tick towards 2.9% but given the surprise in producers data, could have a 3 handle for the first time since 2011. This has fuelled expectation that the Fed will indeed need to push ahead with two further rate hikes this year. It is interesting to see though that this dollar strength comes with the bond markets remaining subdued and are not driving the move in the greenback. Longer dated yields remain anchored and the yield curve continues to flatten further. The fears over the negative impact of an escalation in the trade dispute with China is playing a role here. Despite this though, the US dollar made a key multi-month breakout against the Japanese yen, whilst also pulling the euro, sterling and also gold weaker. Sentiment over the trade tariffs dispute has settled once more overnight and a mild rebound has been seen in Asian trading. It will be interesting to see how this develops today. In the UK, the UK Government issues its long awaited white paper on its vision for a trade deal with the EU, whilst there is expected to be a mixed reaction to the visit of President Trump.

Wall Street closed strongly to the downside with the S&P 500 -0.7%, but with futures higher (S&P e-mini +0.4%) has helped Asian markets higher (Nikkei +1.2%) with European markets set to open higher today. In forex, there is a degree of settling in the dollar strength. The yen remains the underperformer, but the euro and sterling have found some support, as has the Aussie, although the remarkable one day turnaround to weakness in the Canadian dollar (despite the BoC rate hike) has yet to be decisively stemmed. In commodities, markets are trying to stabilise from the sharp decline (the largest in two years) in oil yesterday, with a mild rebound today, whilst gold has bounced a couple of dollars. However, there is yet to be any suggesting the moves are going to substantially retrace.

Traders have a little Eurozone data to deal with before US inflation which is today’s main event. The Eurozone Industrial Production is at 1000BST and is expected to pick up by 1.2% in the month of May and improve the year on year to +2.1% (from +1.7% last month). The ECB monetary policy meeting accounts are at 1230BST and will add more meat to the bones of the recent move to end asset purchases in December. However, the big focus for today is the US CPI inflation which is expected to show the headline CPI ticking higher again to +2.9% (from +2.8%) which will be notable given the wage growth lies stubbornly at just 2.7%, whilst the core CPI is expected to tick up to +2.3% (from +2.2%). The Weekly Jobless Claims at 1330BST are expected to improve slightly to 225,000 (from 231,000 last week).

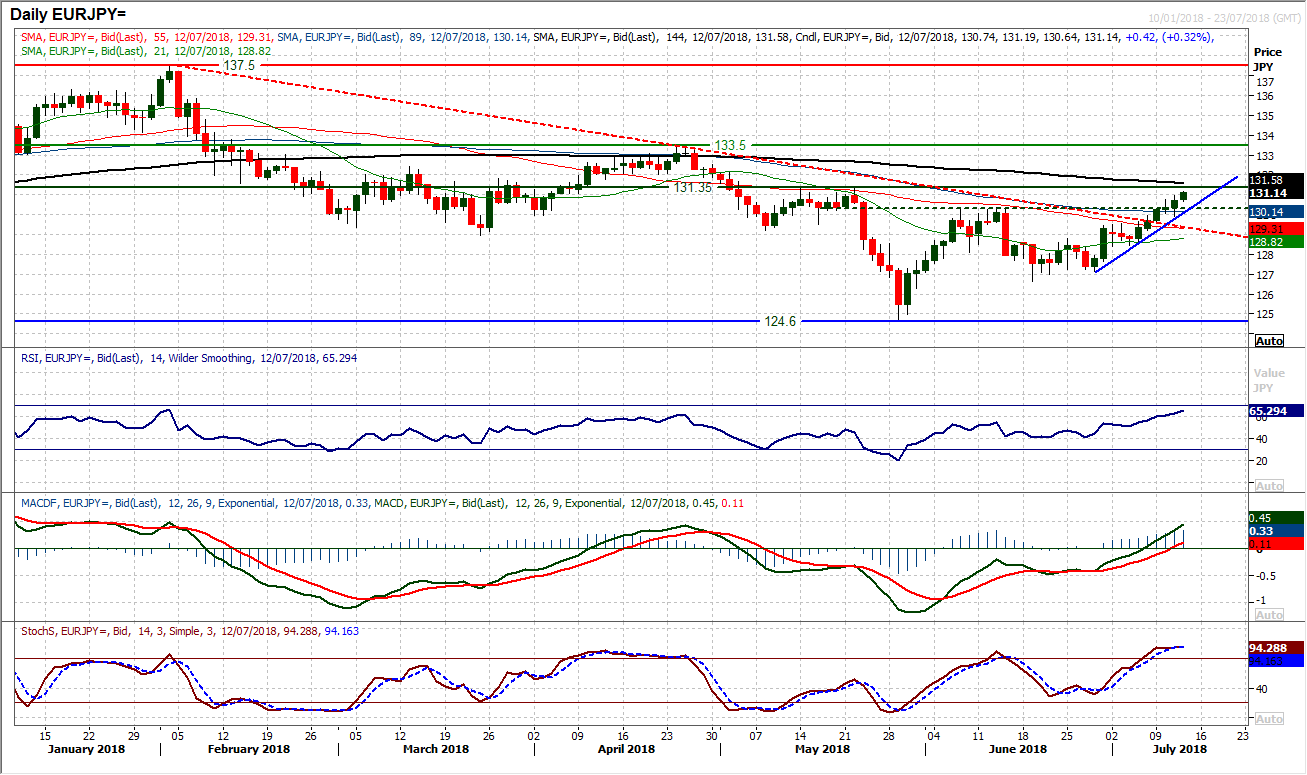

Chart of the Day – EUR/JPY

The yen has been showing broad strength against the euro for much of 2018, with a downtrend that originated back in February. However, the outlook has shifted in the past few days. Bouncing in May from 124.60, with the breakout above 130.35 the market has now confirmed a higher low at the June low of 126.65. This has come with the pair breaking the five month downtrend. This all suggests that a new uptrend formation is coming. The momentum indicators all point towards a strength in the recovery, with the RSI rising decisively above 60 and at its highest since the sell-off began in February, whilst the MACD lines are accelerating above neutral and the Stochastics are strong. Yesterday’s positive candle included a close above 130.35 whilst a two week uptrend is also forming to suggest intraday corrections are a chance to buy. A move above the next resistance at 131.35 would continue the run of breaching resistance and open the key April high at 133.50. The old resistance is now supportive at 130.35 whilst the hourly chart shows positive momentum configuration with support at 129.90 and then a pivot around 129.60.

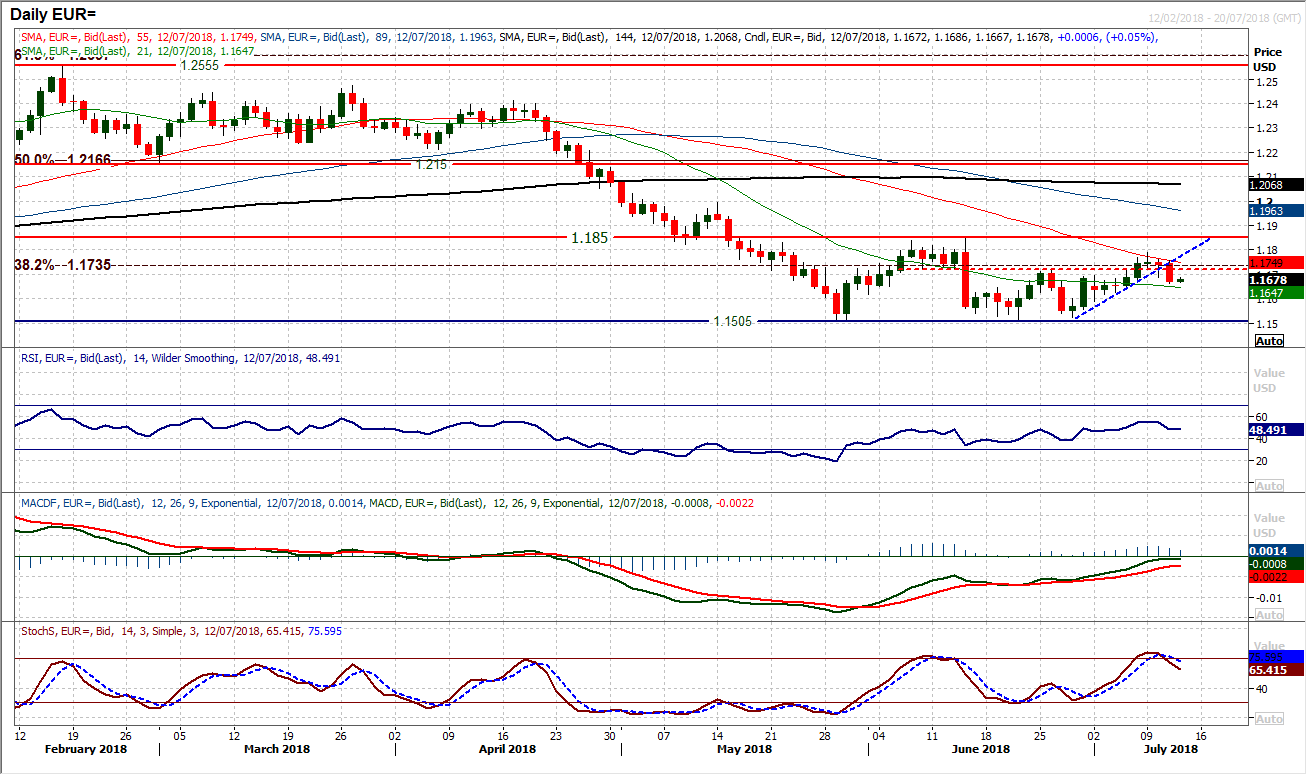

EUR/USD

The prospect of a sustained euro recovery has been put on ice, at least for now, as the stronger dollar into the close formed a decisive bear candle yesterday. This now means that having posted higher lows for a run of seven sessions, the situation is being turned on its head as the market has now posted lower highs and lower lows in the last two sessions. This move is pulling negatively on momentum indicators, with the RSI back below 50, Stochastics crossing lower and MACD lines stalling their recovery under neutral. The uptrend recovery has also been decisively broken. The reaction today will be key as to whether the momentum now builds to the downside. The hourly chart shows the importance of momentum signals, with the hourly RSI now failing at 60 and pushing on 30, whilst the MACD lines are failing under neutral. If this situation continues then intraday rallies will be a chance to sell, with the band of resistance $1.1690/$1.1720 now a key gauge of near term overhead supply. Initial support is at $1.1665 before $1.1630.

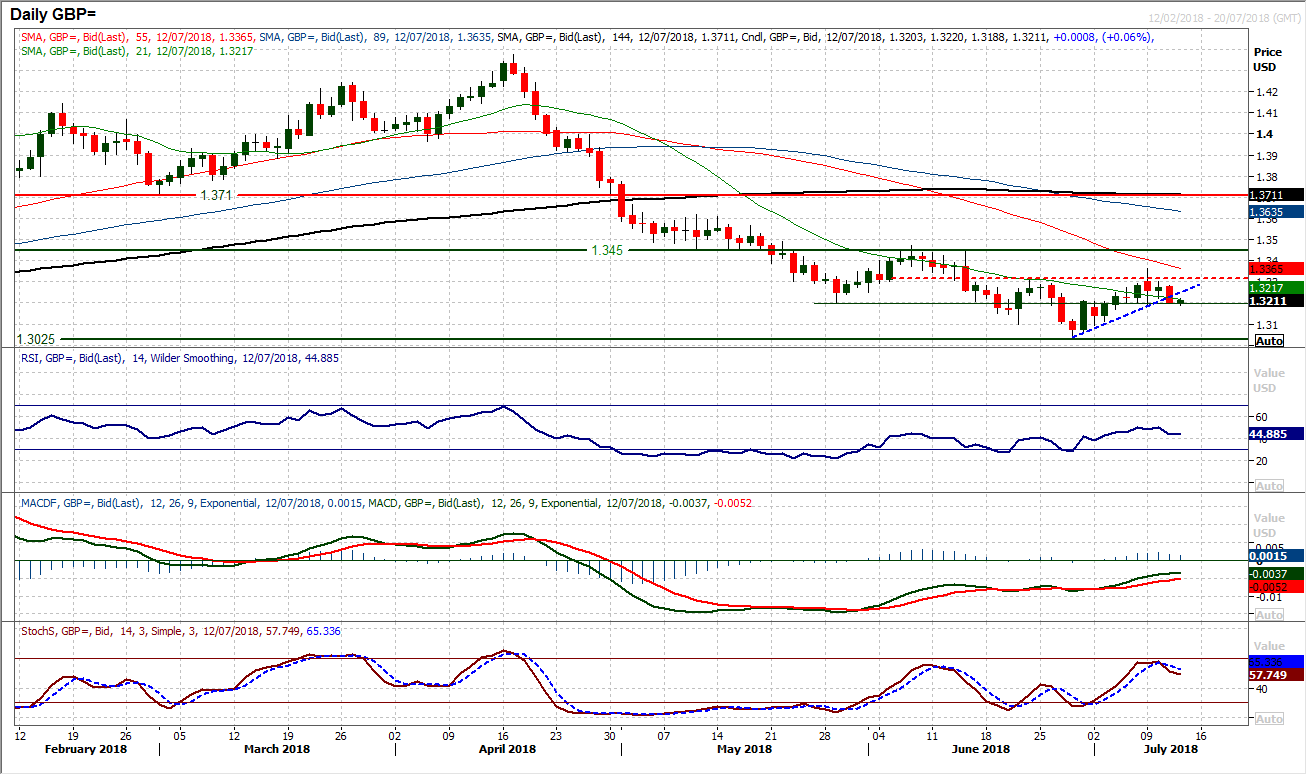

GBP/USD

After a second strong bear candle this week, the recovery uptrend has been broken and the selling pressure is mounting again. A pivot around $1.3200 is a basis of support and a decisive close below the pivot would now suggest that the recovery had lost its way and instead the risk would be for a test of the June low at $1.3050 again. Momentum indicators have been improving well, until the slip yesterday and so the price action in the next session or two will therefore be critical for how the market now develops. There has been no decisive deterioration yet in Cable on price or momentum, but should the selling pressure breach $1.3200 decisively, then the outlook will look negative once more. The importance of this pivot is shown on the hourly chart which again is on the brink, but with a negative bias developing. There is a lower high now at $1.3300. Subsequent support is $1.3170 and then $1.3090.

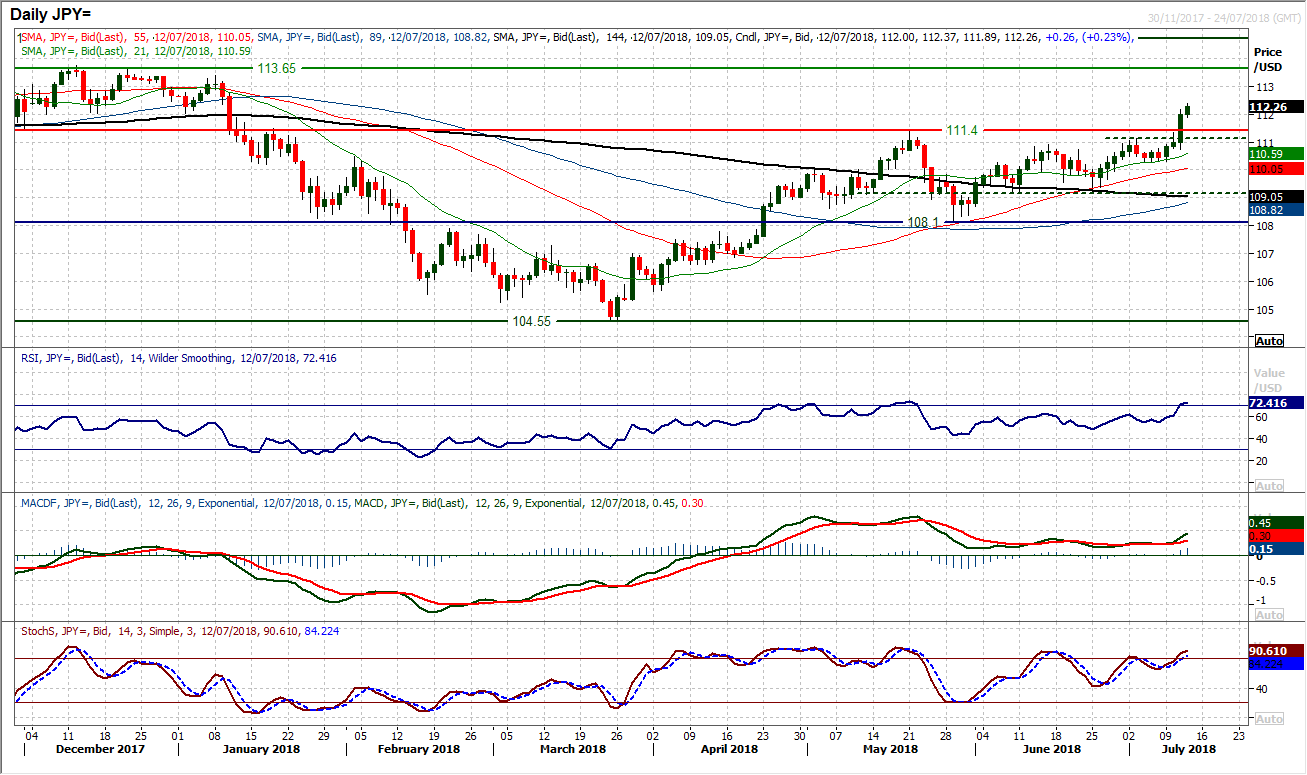

USD/JPY

After several weeks of consolidation, the upside pressure has finally told and the dollar bulls have broken through. The fact that this came during a session where risk appetite was supposedly weaker perhaps also makes this break even more significant. A strong bull candle not only closed above 111.15 but also the key May resistance at 111.40 to take Dollar/Yen to its highest level since early January. This now opens the December/January resistance band 113.40/113.65. All indicators now confirm the breakout, with even the MACD lines ticking higher (finally). There is now a good band of breakout support 111.15/111.40 but the bulls look strong with this one, and when Dollar/yen trends, it really does go! The hourly chart shows overnight support now 111.90/112.15 and weakness is a chance to buy.

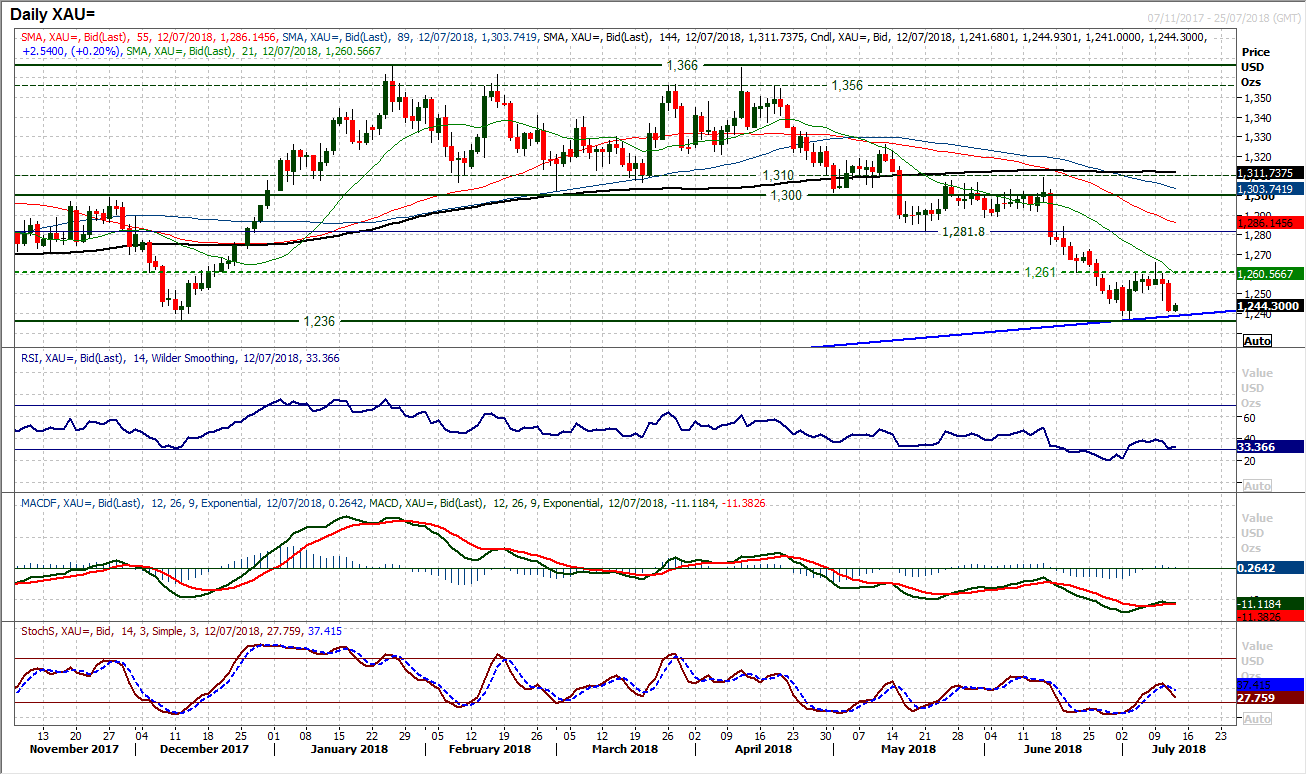

Gold

Renewed dollar strength has ripped gold lower, as a consolidation that failed to breakout decisively above $1261 has ended with a decisive bear candle. The move that fell $13 into the close is now testing the key support $1236/$1237 but also the long term uptrend. An initial rebound of a couple of bucks is giving the bulls hope, but the deterioration in the momentum indicators is a real concern now. The Stochastics crossing back lower with the RSI back into the low 30s and MACD lines stuttering lower too is a real problem now. There is overhead supply now at $1250 whilst hourly momentum is negative to suggest intraday rallies are a chance to sell. The importance of the resistance band $1260/$1265 is growing. A decisive closing break of $1236 opens $1204.50.

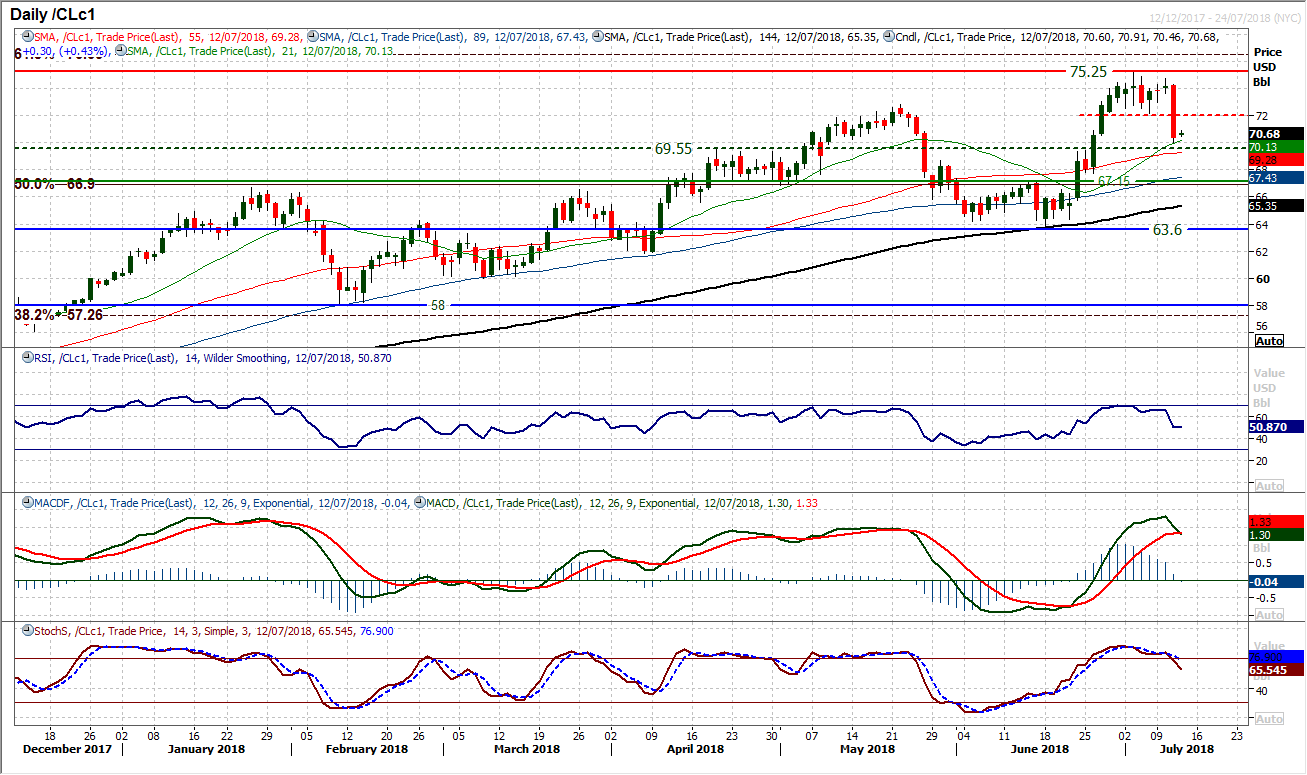

WTI Oil

A massive bearish one day candle has completely changed the outlook for oil. A close below $72.15 completed a small top pattern which implies $3.10 f downside which means $69.00 is a realistic correction area now. A sell signal on the Stochastics adds to the corrective pressure too. Today’s reaction is mildly higher initially and the day after such a huge move can often see a retracement, but unless there is an instant reaction from the bulls, then the move may struggle for traction. The $70 psychological level is clearly being watched now, marking yesterday’s low. The Marabuzo line (mid-point) of the yesterday’s candle is at $72.30 and is a gauge of resistance now.

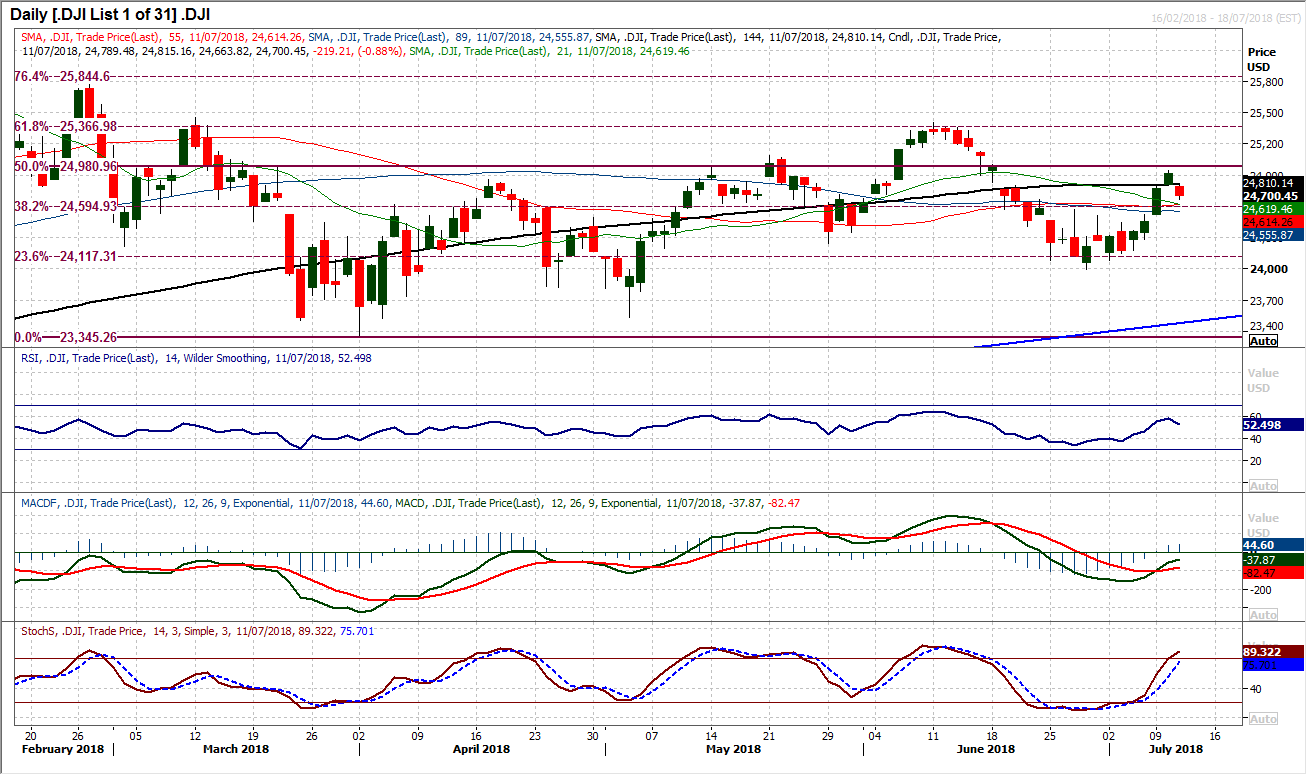

Dow Jones Industrial Average

The rally lost its way yesterday amidst the reduction in risk appetite from the trade tariffs, and this has maintained the rather mixed medium term outlook on the Dow. Only a mild negative candlestick formed on the day would suggest that the selling pressure was relatively well contained. It will now be interesting to see how the bulls react, as it appears that the negative reactions to the trade tariffs are becoming less long lasting. Wall Street futures are pointing higher now but as technical momentum indicators have already begun to roll over again, this needs watching. The support now needs to build with the band of initial support 24,569/24,663. The bulls will be concerned that the turn lower has once more come around a key Fib retracement level, with the resistance of 50% at 54,980 a factor in leaving the high at 24,945. Once more around the clutch of moving averages this is a choppy look to the market.

Author

Richard Perry

Independent Analyst