Dollar negative again going into key inflation data

Market Overview

The market remains dollar negative as the trading week draws to a close, with the key data points of the week as US inflation and retail sales set to be announced. The Fed minutes continue to reflect the FOMC being concerned over a lack on inflation despite pushing ahead in its tightening cycle. Looking at the flattening shape of the US yield curve this is clearly how the market sees risks too, with the 2s/10s spread falling further overnight. Inflation seems to be a key theme and with the prospects of success in Trump’s tax reform plans getting through Congress receding, the ability for the US economy to generate its own inflation (due to the Fed’s trusted old Phillips Curve kicking in) will be in focus today. Core CPI picking up for the first time in 2017 could begin to shift a few staunchly held beliefs in the market that the Fed will struggle to hike three times in 2018 due to subdued inflation. Going into the inflation data, the dollar remains on the offer, but momentum in the recent selling pressure has just reduced as this important announcement has approached. Donald Trump could also have a part to play in today’s trading, as he is set to speak on the Iran nuclear agreement. Press briefings suggest that he will stop short of renouncing the agreement, however with this maverick President, one never really knows.

Wall Street had a pause for thought yesterday and dropped back a touch into the close (S&P 500 -0.2% at 2551) and although Asian markets were mixed to positive (Nikkei +1.0%) the European markets are cautiously lower again although FTSE 100 looks to be an underperformer initially as sterling has bounced. In forex, the dollar is again underperforming across the majors but it is likely that the US inflation data will drive moves later today. In commodities, with the mild dollar weakness we find gold again supported whilst the choppy moves on oil of recent times continue, with a rebound after yesterday’s decline.

For the final day of the trading week the key tier one data comes into focus. After a quiet European morning, the US CPI inflation is at 1330BST. Headline CPI is expected to jump to +2.3% from +1.9% however it will be the core CPI which is expected to tick higher to +1.8% from +1.7% that will be the big news. Core CPI has not increased at all during 2017 and could mark a sea change which helps to support the Fed’s tightening cycle of three hikes in 2018. US Retail Sales is also a key factor 1330BST with ex-autos expected to jump by +0.3% for the month after +0.2% last month. The University of Michigan Sentiment is also at 1500BST and the consumer sentiment gauge is expected to drop very slightly to 95.0 from 95.1 last month. Fed speakers are also on the agenda again today with Charles Evans (voter, centrist/hawk) at 1525BST and Robert Kaplan (voter, mild dove) at 1630BST.

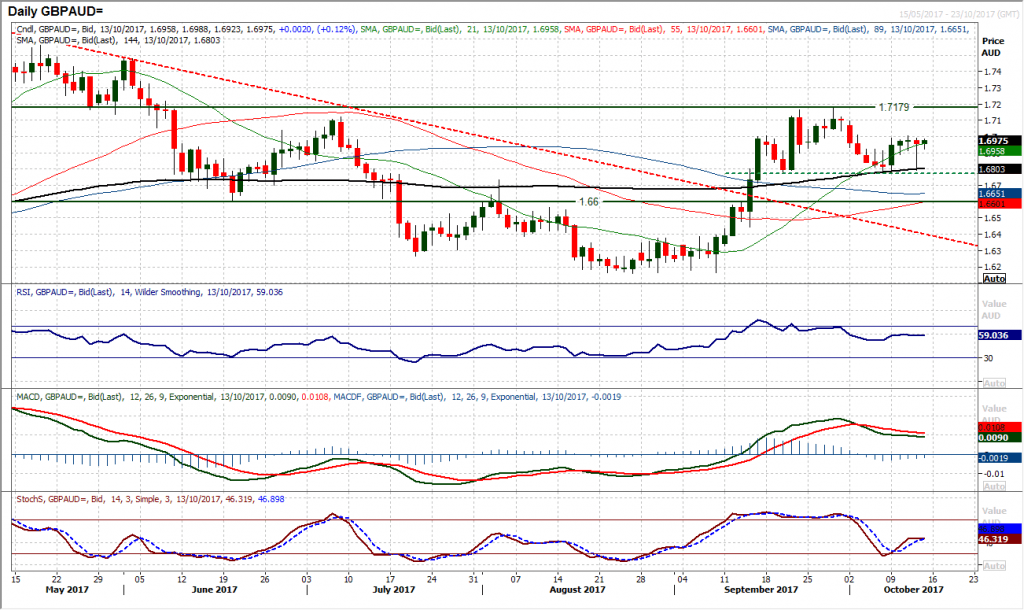

Chart of the Day – GBP/AUD

Even though sterling saw a sharp intraday rally into the close yesterday, it is still worth pointing out the move that is developing on Sterling/Aussie. Another test of the key near term support at 1.6775 shows how the market is forming a four week reversal pattern, which currently looks to be a well-defined head & shoulders top. The support has held at 1.6775 but the prospect of this top pattern remains in play. Aside from the intraday noise yesterday the candle was still a negative close and has continued lower today, suggesting that the Aussie is now beginning to outperform sterling again. The momentum indicators are already tracking lower with the RSI showing a series of lower highs over the past few weeks, the MACD lines in decline and the Stochastics also turning back lower again. On the hourly chart the rebound has helped to unwind negative momentum and it will be interesting to see how the market reacts with 1.6970 as a lower high below the resistance around 1.7000. A move back below 1.6890 would also increase downside momentum for another go at the neckline of 1.6775 again.

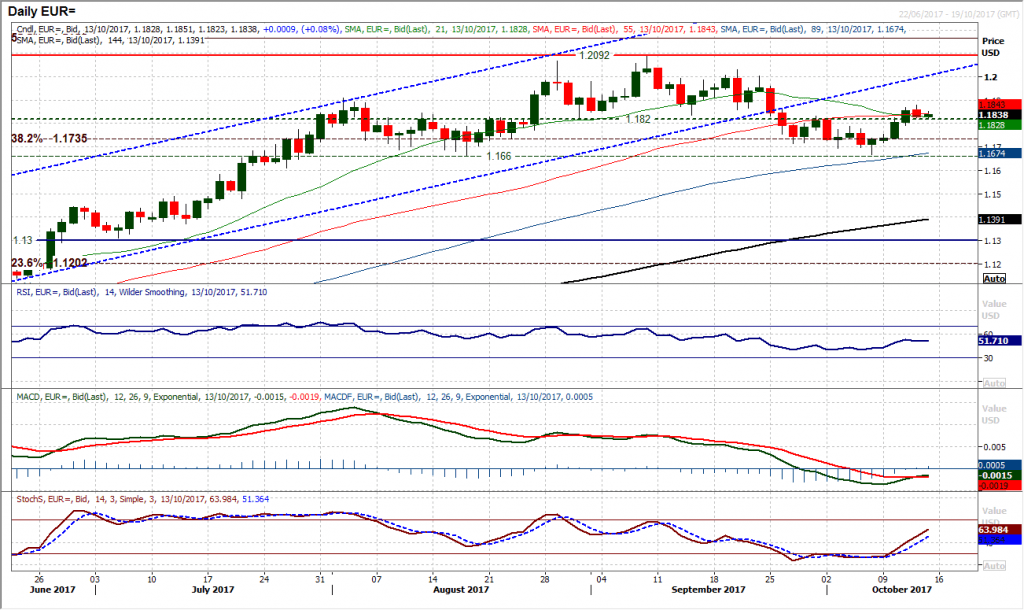

EUR/USD

Having broken back above the neckline resistance the euro is testing the stability of $1.1820 to act as a new pivot, and it is so far standing up to the job. There is though a degree of consolidation that we are seeing ahead of the key US inflation and retail sales data later today that could limit the moves in the early European session. Despite this though the bulls will be looking to build now above $1.1820 to continue to improve the outlook that has been picking up over the past week since bottoming near term at $1.1667. The daily momentum indicators are ticking solidly higher with the RSI and Stochastics both rising above 50, whilst the MACD lines have just also completed a bull cross. There is now a near term band of support $1.1795/$1.1820 to watch through the inflation data and if this can survive the initial test (certainly if inflation gives a negative surprise) then the bulls could continue higher. Resistance initially at yesterday’s high of $1.1880 before $1.1960 and then up to test $1.2000 again.

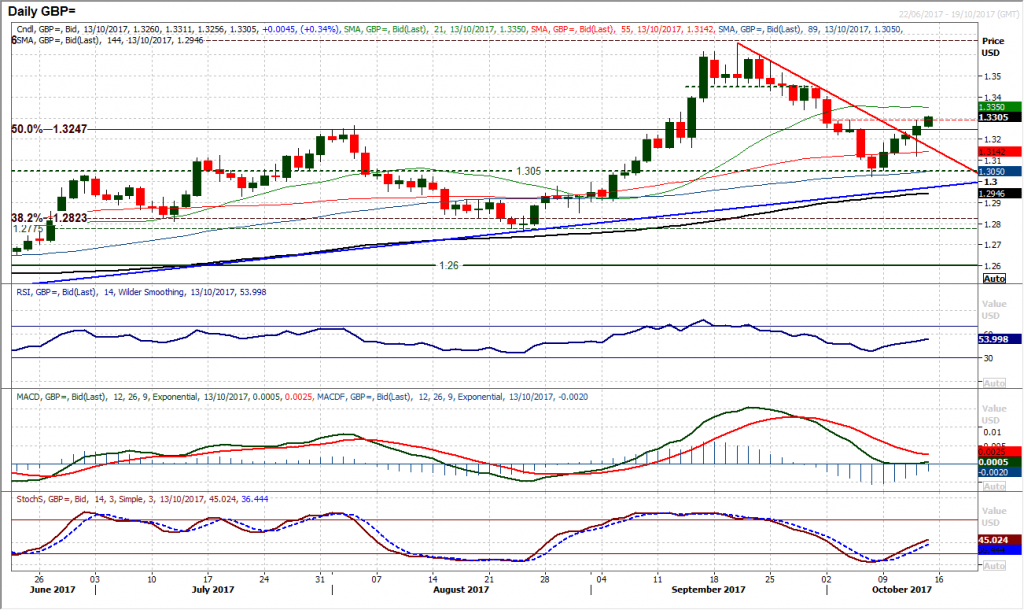

GBP/USD

It was a choppy session yesterday for Cable but the bulls seemed to win the day in the end to continue the recovery of the past few days. Despite an intraday spike lower to $1.3120 the sharp turnaround of over 150 pips has pulled the market back higher to test the $1.3290 resistance. This is the next resistance within the old downtrend and one which protects the subsequent $1.3340. Momentum indicators are still hovering around neutral medium term levels and need this near term move to continue to break resistance in order for the bulls to sustainably look in control. With the intraday wobbles yesterday there is still an uncertainty about the hourly momentum indicators. Once more, the tier one US economic data this afternoon will have a big say in near term direction, however it would probably need strong inflation to break what is now a higher low at $1.3120 and to put the bears back in control.

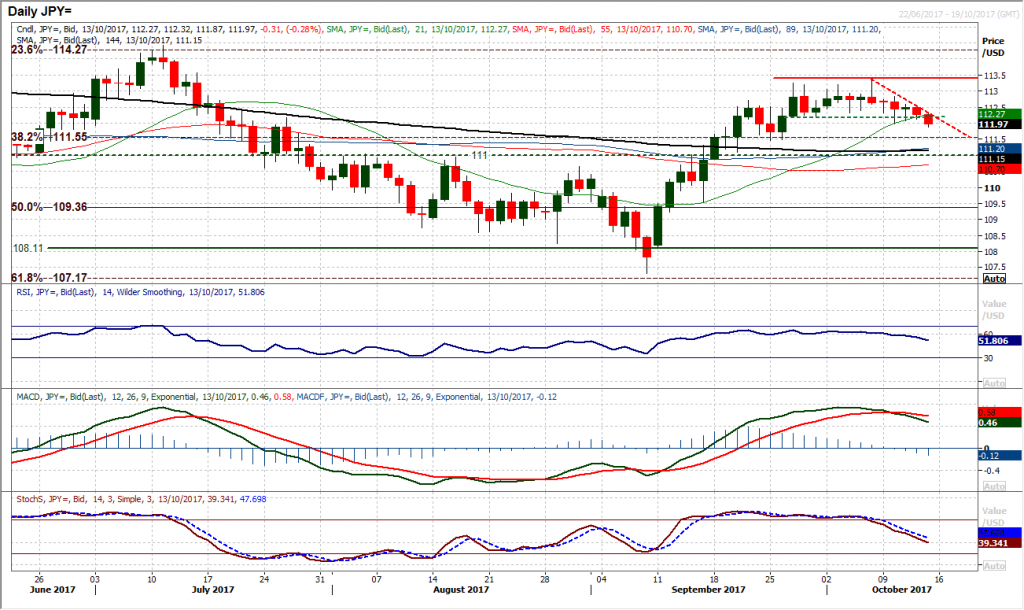

USD/JPY

More intraday pressure on the old support at 112.20 as for a third session we see a breach only to close back above. However in this war of attrition the sellers seem to be gradually gaining the control. Once more we see the support breached early today and technically the market is breaking down, albeit in slow motion. A close below 112.20 would complete a small rolling top and imply 120 pips down to the medium term pivot at 111.00. The deterioration in the momentum indicators would certainly agree with this with the Stochastics and RSI tracking decisively lower whilst the MACD lines continue to drop following their bear cross. The sequence of lower highs is also building with the hourly chart showing 112.45, 112.60 and 112.80. An intraday failure of 111.98 would also drive a break lower with 111.45 the next support. The one big caveat with this deteriorating technical picture would be a positive surprise in US inflation and retail sales today which would drive a dollar recovery. The move lower on Dollar/Yen would suggest the market is certainly not expecting it.

Gold

The recovery continues to creep back higher as the momentum indicators begin to all line up for a more positive outlook. This comes with a fifth consecutive positive close and a market positioning for a move back to test the key $1300/$1310 pivot resistance. The bull cross on the MACD lines is the most compelling technical factor now as each of the three previous bull crosses in 2017 have all coincided with strong rallies. Intraday corrections continue to be bought into with the hourly chart showing old breakout levels being seen as supportive. This is leaving support at $1279, around $1285 and now around $1290. Initial resistance is at $1297 from yesterday’s high but the bulls continue to build for a test of the key long term pivot again. Today could be the key day for this test with the tier one US data likely to impact strongly on the dollar and subsequently on gold.

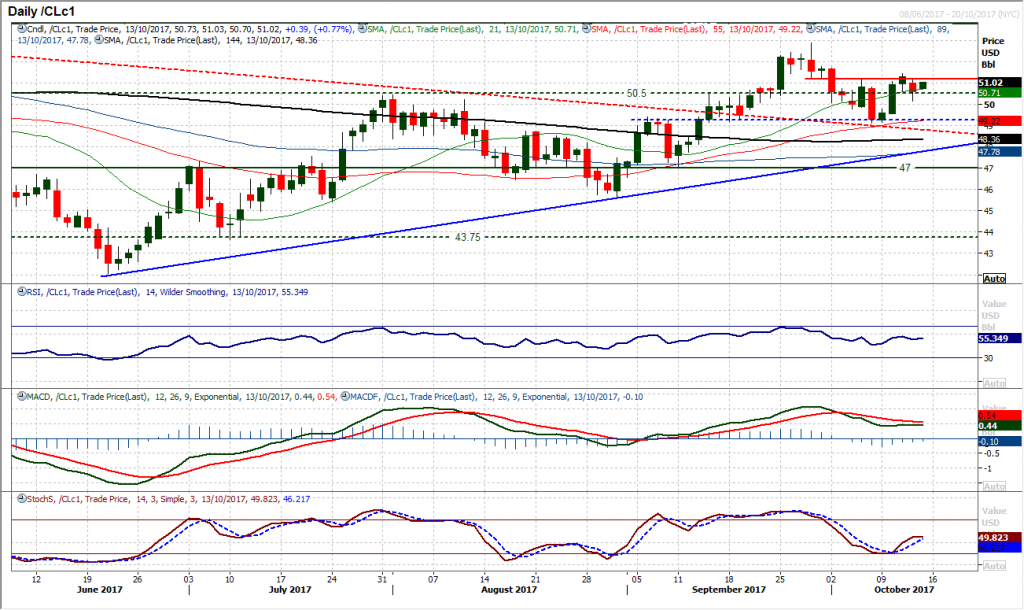

WTI Oil

As in keeping with the market of the past week or so, yesterday was another volatile session which is difficult to decipher on a near term basis. The bulls looked to be grasping control on the close above $51.20 but have been dragged back once more. There is though a positive medium term pull higher on the market which is providing an underlying support. This is reflected in momentum indicators which are holding in positive configuration through the near term noise. The bulls have reacted higher again today as the supportive EIA inventories seem to have cancelled out the previous API inventories which had been apportioned at least some of the blame to the initial downside yesterday. Yesterday’s low does now leave support in place at $50.15 and the bulls are now eying Wednesday’s $51.40 high again.

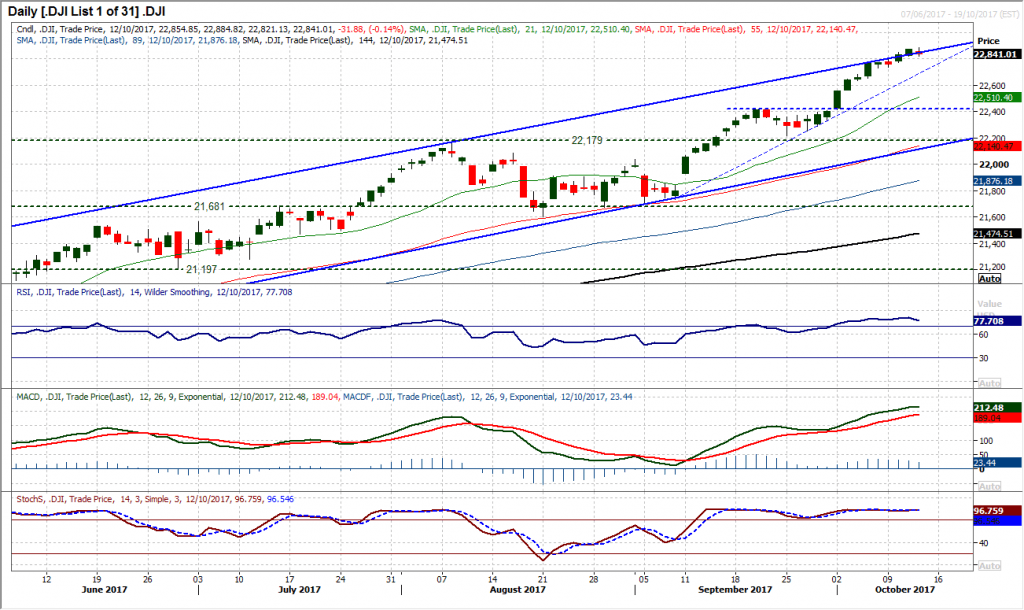

Dow Jones Industrial Average

With the trend so strong there is little reason not to view corrections as a chance to buy. Yesterday’s rather mild dip back should be nothing more than a brief consolidation in the trend higher. The uptrend channel continues to be hugged higher as the upper Bollinger Band has been in recent weeks. With momentum indicators strongly configured look to use weakness as a chance to buy. The Parabolic SARs (a profit-taking trend indicator) which have been shadowing the run higher for the past seven weeks come in around 22,750 today and are a good gauge of running support. The hourly chart also remains strongly configured and initial support is in place at 22,770/22,803. Yesterday’s intraday all-time high at 22,885 is now resistance.

Author

Richard Perry

Independent Analyst