Dollar gains on higher yields as focus turns to Brexit

Market Overview

The sharp move higher on Treasury yields came a couple of weeks ago as traders looked at the employment components of upside surprises in the ADP report and ISM Non-Manufacturing, taken together with a hawkish sounding Fed chair Powell to conclude that a tight jobs market would lead to higher wages and higher inflation down the road. The first part of the equation continues to build, with another labor market indicator, the JOLTS jobs openings accelerating to record levels and way above estimates to over 7 million. The hard inflation data is still restricted on the other side of the equation and bond markets will now try to figure out whether to pre-empt higher price levels. Yields will remain a key market read-through. Yields have edged higher tentatively and this has pulled a mild dollar rally with it overnight. Perhaps yields would be higher were Donald Trump to stop his unconventional verbal attacks on Fed tightening. In Europe today there is another focus though. Aside from the inflation data for the UK and Eurozone (see below), Brexit negotiations hit another crucial juncture at the EU Summit today. Can Theresa May, who is seemingly entering a sword fight with two hands tied behind her back, come out of another battle with her EU counterparts and secure a deal on a Withdrawal Agreement? The issue of the border in Northern Ireland is the megalithic stumbling block. They need to prevent a hard border between Northern Ireland and Ireland, something that neither side wants. But if the negotiations over a technical solution fail, what is the position of last resort? The EU wants an indefinite open border and keeping Northern Ireland at least in a customs union, but the UK sees that as effectively creating a border within the UK (in the Irish Sea) and is unacceptable. There is the potential for another emergency summit in November to solve the issue, but time is ticking and hopes of an agreement today are thin on the ground.

Wall Street rallied sharply last night as strong earnings from Morgan Stanley, Goldman Sachs and Johnson & Johnson drove expectation that earnings season may be more encouraging than previously thought. The S&P 500 closed 2.1% higher at 2810 and futures are a tick higher (Netflix is certainly helping this) and Asian markets were broadly positive overnight (Nikkei +1.3%, Shanghai Composite +0.5%). European markets are also gaining in early moves as the prospects of recovery spread. In forex there is a hint of dollar strength after the greenback reined in some losses late in yesterday’s session, however there is little real direction of note. In commodities there is a consolidation too on gold and silver, whilst oil is again just edging higher.

The Fed minutes will get a large degree of the focus for the economic calendar today, but in the European morning there is inflation on the agenda. First up is UK CPI inflation at 0930BST which is expected to slip back a touch on headline CPI to +2.6% (from +2.7% in August) whilst core CPI is expected to drop back to +2.0% (from +2.1% a month ago). The PPI Input Price are also worth keeping an eye on after last month dropping back to 8.7%. They are expected to increase back higher to +9.2% and they are seen as a gauge of how sterling strength plays into inflation. The final Eurozone inflation reading for September is then at 1000BST and is expected to be confirmed at +2.1% on the headline inflation and +0.9% on core. US Building Permits are at 1330BST and are expected to tick marginally higher to 1.28m (from 1.25m) with Housing Starts expected to drop back to 1.21m (from 1.28m). The EIA oil inventories are at 1530BST with crude oil stocks expected to build by +2.5m barrels (+6.0m last week), with distillates in drawdown by -1.5m barrels (-2.7m last week) and gasoline in drawdown by -1.5m (+1.0m last week). The FOMC minutes for the September meeting are at 1900BST. There may be little real surprises given the press conference and projection materials already released, but the market will be looking for hints over not only the next rate hike (expected December) but also into 2019, whilst removal of the word “accommodative” will also get some interest.

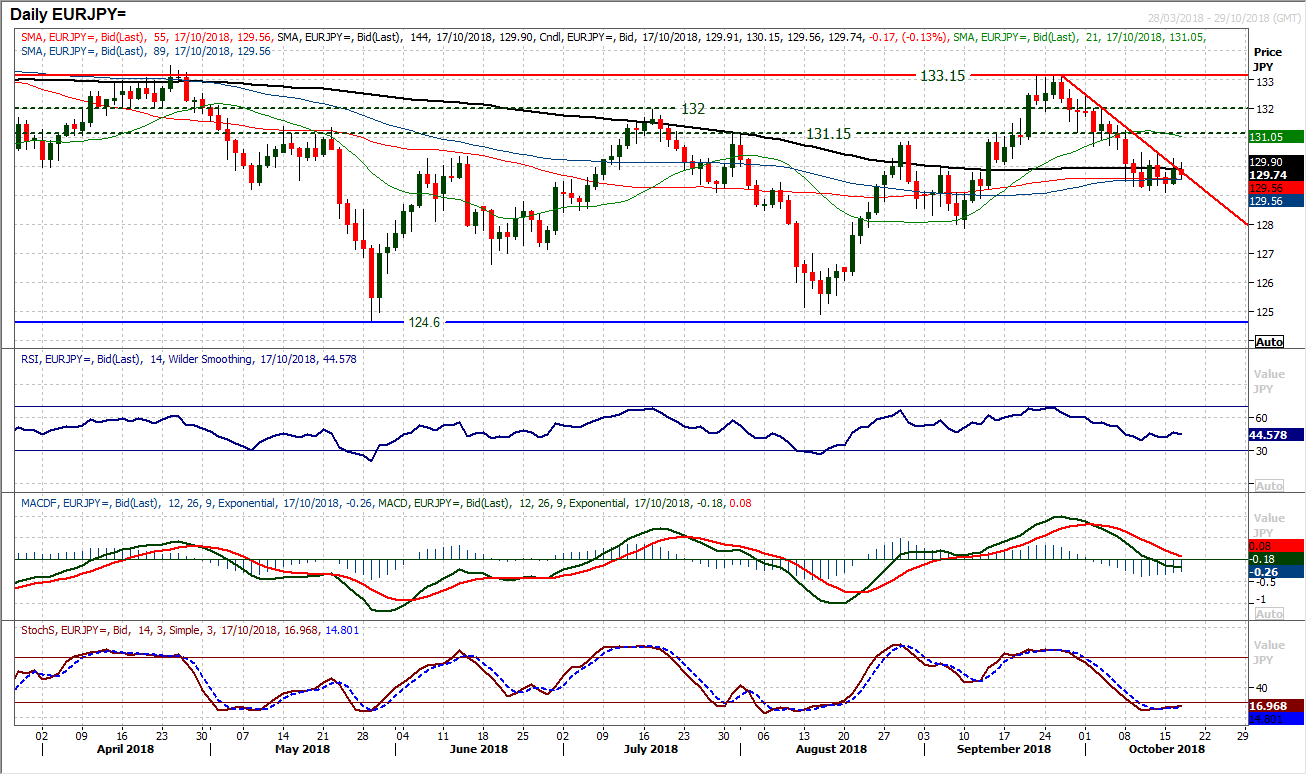

Chart of the Day – EUR/JPY

With market sentiment stabilising there has been a slowing of the selling pressure through Euro/Yen. However, the three week trend is still lower and although it is being seriously tested on an intraday basis, nothing has yet been confirmed. The market has now though effectively been trading sideways for the past week and there is a settling of the corrective momentum. This is coming as the RSI has unwound to settle around 40 and the MACD lines have unwound to neutral. If the support at 129.10/129.20 continues to hold then the bulls will be looking at the prospect of a renewed recovery. The breaching of a downtrend would not necessarily mean that the market will be going higher either, as there needs to be a closing break above 130.50 which has capped the upside over the past week. This would then form a small base pattern but more importantly signal a turnaround in sentiment. This would open a return to the resistance over head at 131.15/132.00. The hourly chart shows momentum is no longer negatively configured, but there needs to be a move to continue a push higher over the last couple of sessions that is forming higher lows and more positive momentum. A decisive intraday move below 129.55 would be a disappointment for the bulls now.

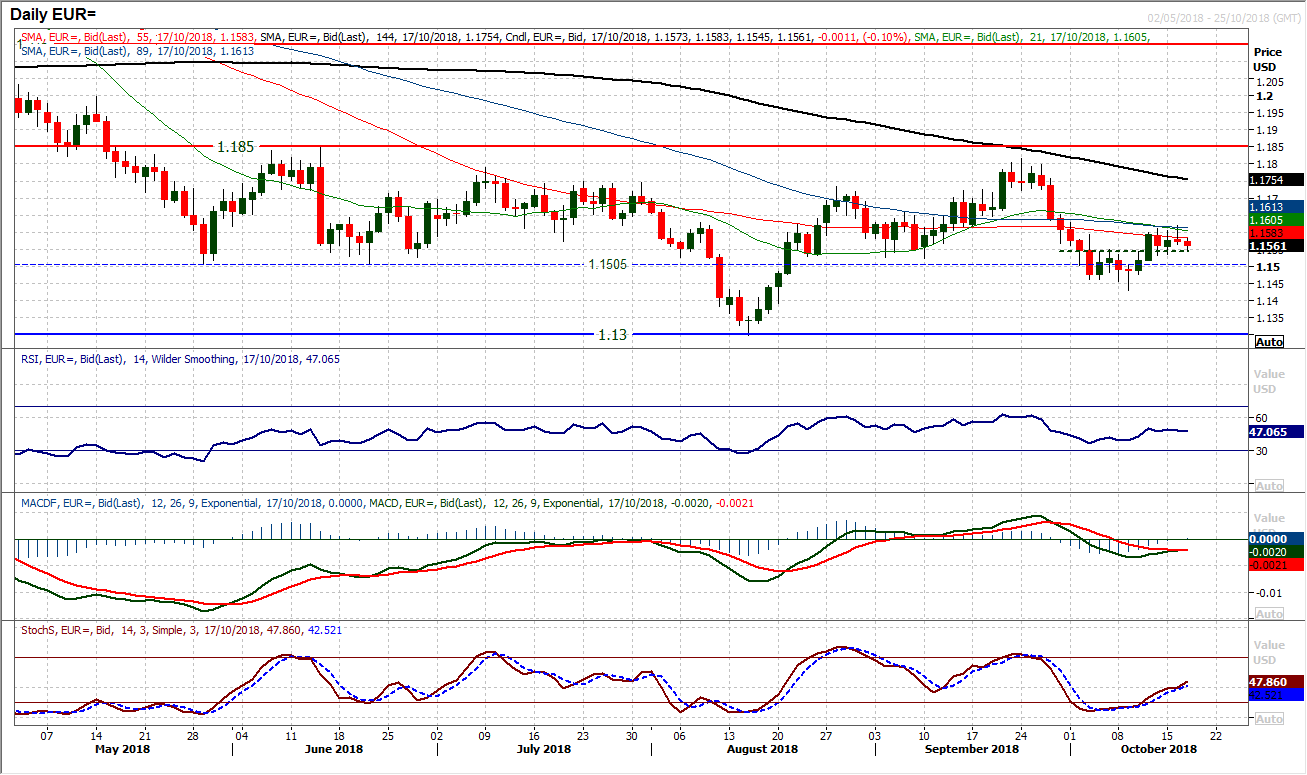

EUR/USD

A near term consolidation continues, but there has been a mild increase in the negative pressure in the past 12 hours which is threatening to turn the near term rebound sour again. There has been a very tight range over the past four sessions which has meant that the bulls have lost the momentum of a rally from the middle of last week. This is reflected in the momentum indicators which are losing their recovery again, worryingly around neutral. The support to watch is in a band $1.1500/$1.1500 as this is a 50 pip band of the old key floor at $1.1500 and the recent neckline of the mini base pattern at 1.1550. This week’s lows are at $1.1535 are an initial level to watch too. A close below $1.1500 would be a disappointment now and re-open $1.1420 key near term low. Resistance continues to strengthen at $1.1610.

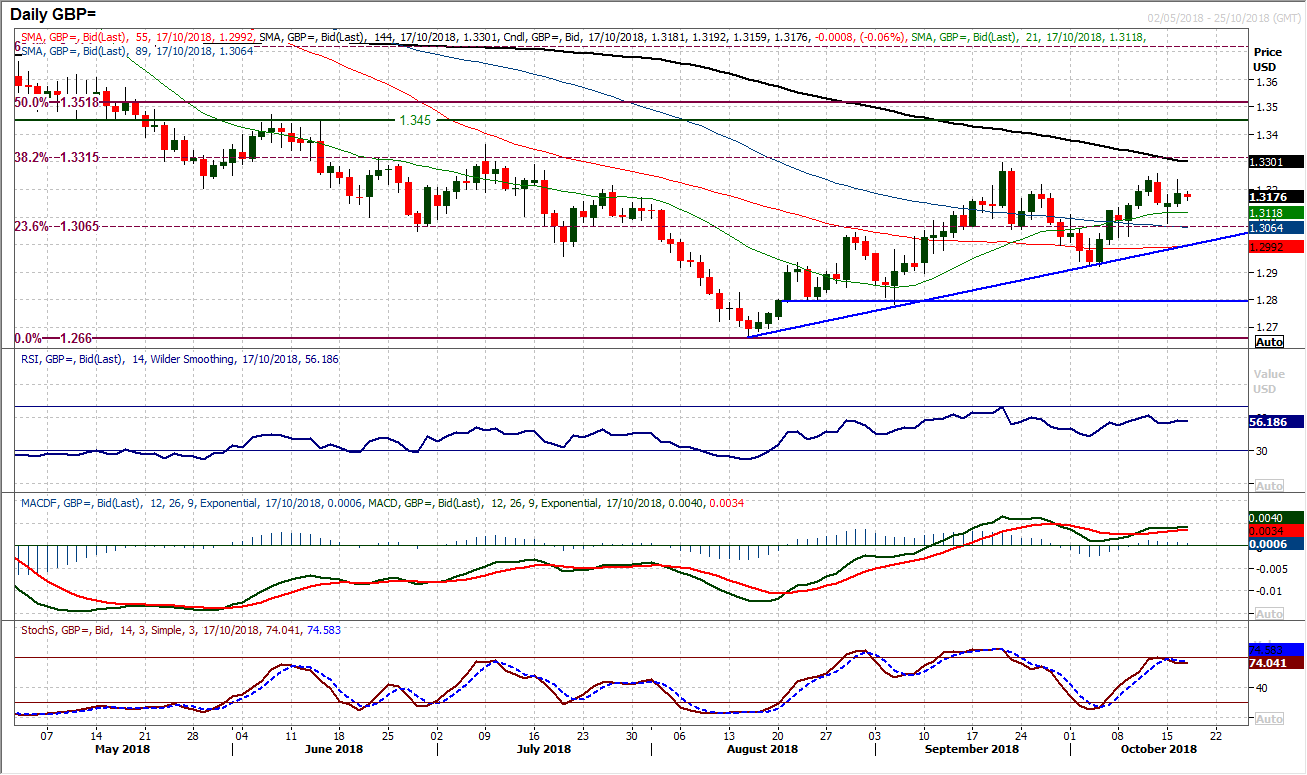

GBP/USD

The dollar seems to be just seeing a swing back into positive traction today and this is pulling Cable back lower again. There is still a significant degree of uncertainty over the outlook of Brexit and in 24 hours from now, this chart is likely to look somewhat different. The technical outlook has just rolled over again, from yesterday’s high at $1.3235 under $1.3260 which is the October high. Momentum indicators reflect the positive bias that arises from the uptrend of the past nine weeks. Support initially comes in at $1.3075 but anything that helps to sustain the uptrend (today at $1.2995) will be a positive. Brexit negotiations remain a key driving factor for Cable. Below $1.2820 is a key breakdown.

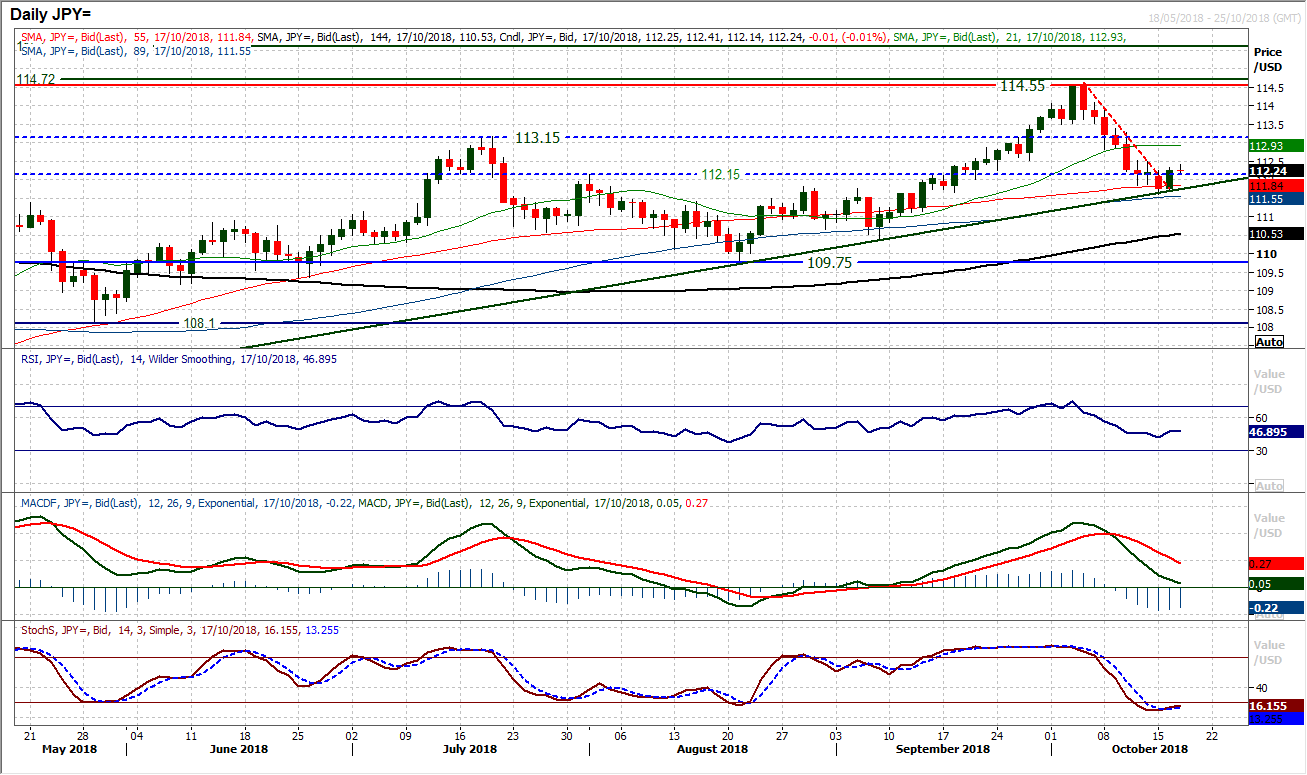

USD/JPY

A decisive bull candle has ended a sequence of bear candles over the previous eight sessions, to break a downtrend but importantly also maintain the support of a six and a half month uptrend. Is this the opportunity to buy? The momentum indicators are all aligning to suggest that this is just another unwinding move within the uptrend, with the RSI bottoming at 40 and the MACD line shallowing out just above neutral. There still needs to be a Stochastics cross to perhaps kick start what could be a renewed rally. Today’s solid open is holding on to yesterday’s 50 pip rebound, but the hourly chart shows resistance at 112.55 needs to be overcome to build momentum in a move higher. Support at 111.60 is growing in importance now.

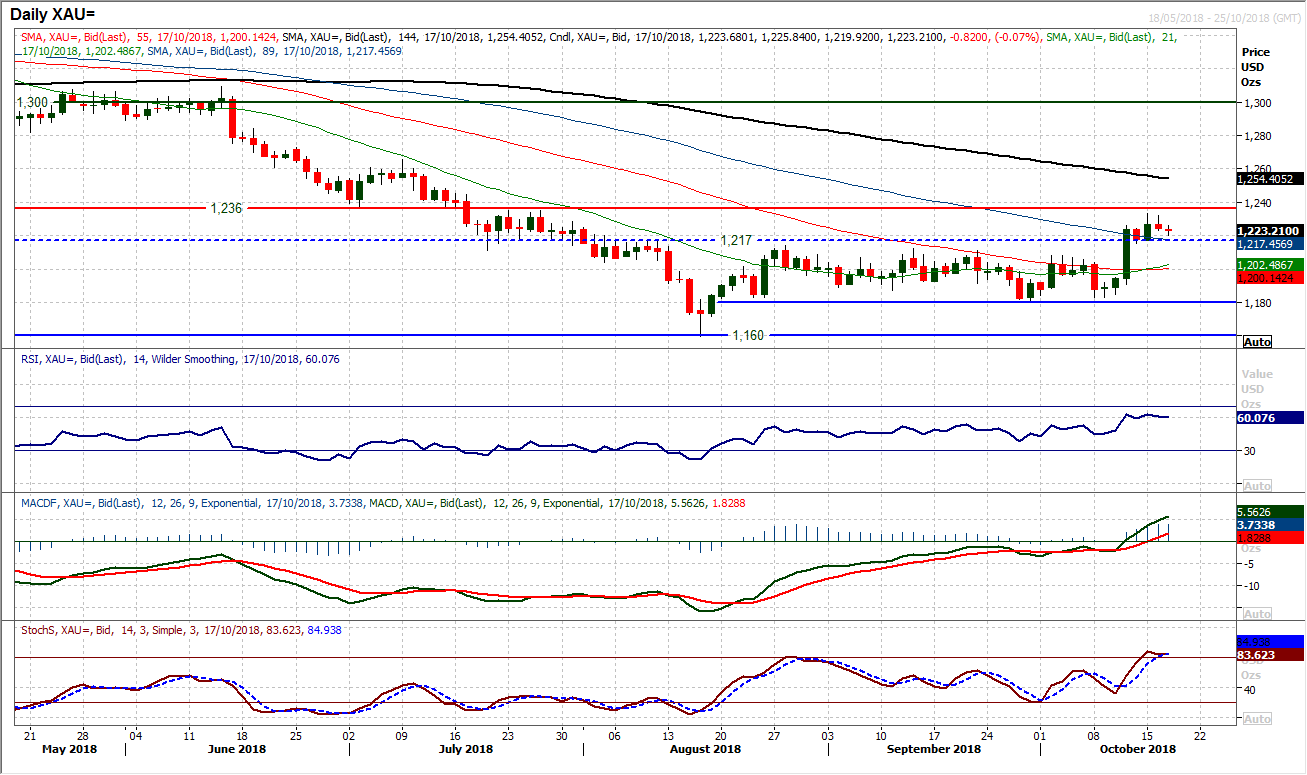

Gold

With the dollar regaining some lost ground, there has been a shade of correction on gold beginning to creep in. The market failed to best Monday’s $1233 high and a mildly weaker candle yesterday is being followed up by a similar move today. The question is now whether the breakout highs can be maintained. The old highs of the range that came in between $1208/$1214 are now a source of underlying demand, whilst the breakout of the old pivot at $1217 is also supportive. It would be disappointing now for the prospects of a recovery if the bulls were unable to hold on to $1208. Momentum is positively configured but has just tailed off. This is an important test of the credentials of a recovery now and if the bulls can build successfully from the support of the breakout then a more considerable and decisive move higher could be in the offing.

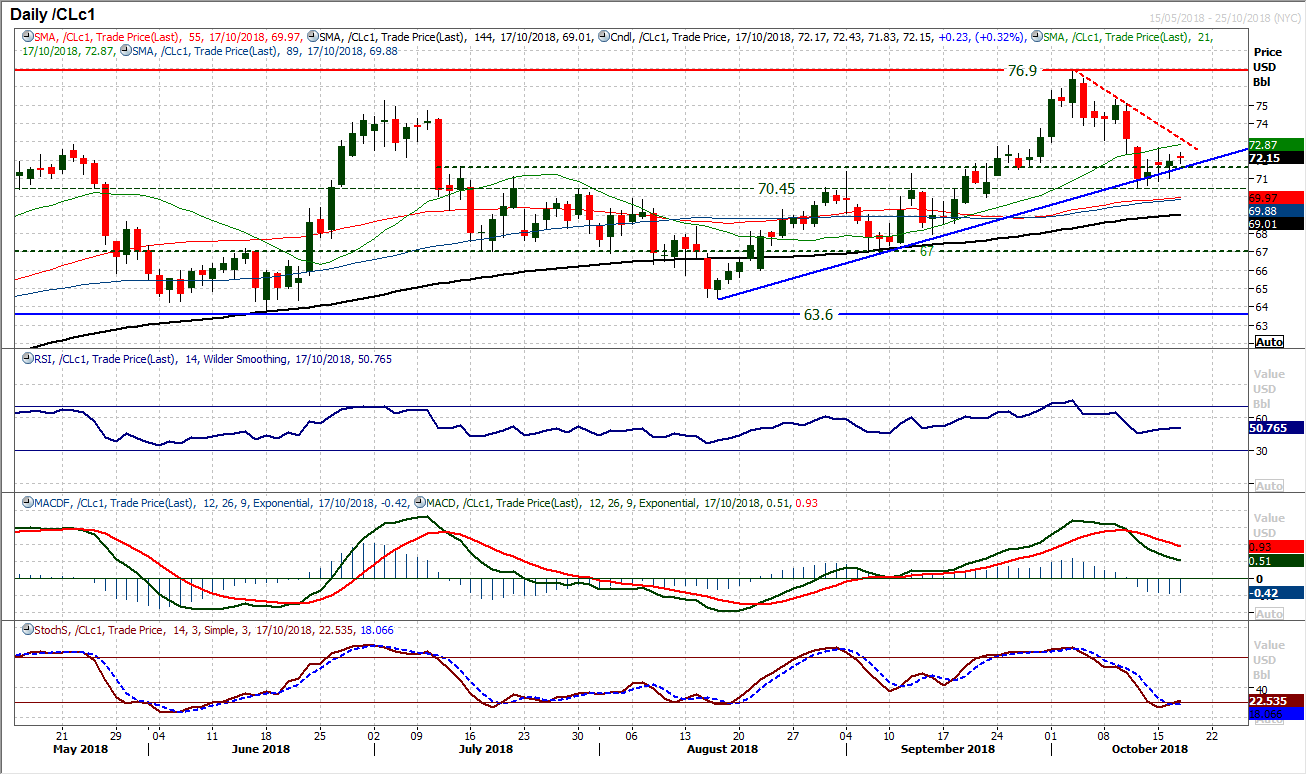

WTI Oil

The consolidation on WTI continues to hold above the recent low at $70.50 but again the bulls seem unable to sustain intraday momentum to be able to drive a recovery. Three candlesticks in a row have had very tight daily bodies within their ranges, whilst yesterday’s range was below Monday’s resistance at $72.70. The market also continues to test the support of the seven month uptrend, so it is almost as though the market remains stuck at this crossroads. There seems to be an appetite to bite for a rally but the bulls just cannot quite take the bait. Momentum indicators have unwound recently and look positively set up on a medium term basis still with a sense that the correction has been another chance to buy. A close above $72.70 would open the way. Support at $70.50 continues to take on added importance, with yesterday’s higher low at $71.00 being a third consecutive daily higher low.

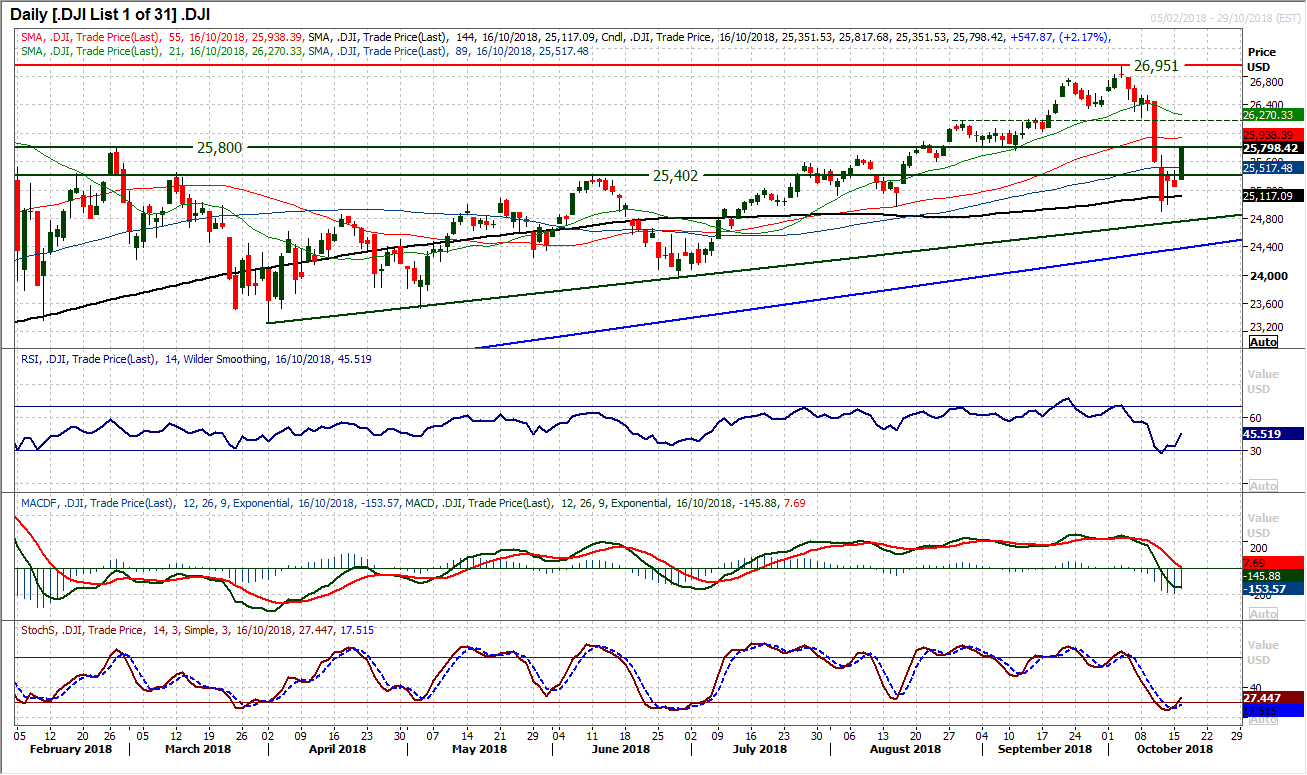

Dow Jones Industrial Average

After a questionable recovery from the low at 24,900 the market (inspired by strong corporate earnings) has taken off again. This looks to be a move enough to at least solidify the support at 24,900 as a key low and now could be set to shift sentiment positively once more. Look at the momentum indicators which have turned a corner now. Focusing especially on the more sensitive indicators such as the Stochastics (crossover buy signal) and RSI (picking up decisively) the move has unwound back to test an old pivot level 25,750/25,800. A decisive move above here would really help to improve the outlook, leaving another old pivot at 25,400 as a basis of support and then re-opening subsequent resistance around 26,165/26,200. The hourly chart shows a big run of bull candles being put together and momentum that is still in this rebound that looks solid to be backed still. The hourly chart shows a mini breakout at 25,500 is also now supportive.

Author

Richard Perry

Independent Analyst