Dollar bouncing with sterling focus on inflation

Market Overview

What seemed to have been a phase of correction on the US dollar is now being turned on its head again. US Treasury yields have rebounded on the suggestion that President Trump could be favouring an economist from Stanford, John Taylor, as the replacement for FOMC chair Yellen when her term comes to an end in February. Taylor is considered to be more hawkish than Yellen and also other potential candidates such as Jerome Powell who is also in the running. Along with further strong survey data out from the New York Fed yesterday, has helped to drive 2 year Treasury yields to their highest level since October 2008, and the US 10 year also rebounding. Coming at a time in which the German 10 year Bund yield has dropped to a five week low, this shift in yield differentials is dragging on EUR/USD. The dollar is bouncing but sterling and euro traders will be looking at inflation which is in focus today as both the Eurozone and UK announce what is likely to be some of the most market moving data of the week. Today’s reading on UK CPI could have a significant impact on the Bank of England’s decision whether to remarkably hike interest rates at the next monetary policy meeting. With the relative weakness of sterling since Brexit, the UK is one country where inflation is much higher than desired and the BoE may need to move to curb the impact.

Wall Street closed strongly again last night as earnings season is supporting gains. The S&P 500 closed +0.2% higher at 2557 and should again be buoyed by strong results from Netflix after hours. Asian markets were broadly positive with the Nikkei +0.4%. European markets are marginally positive in early moves. In forex the recovery in the US dollar is showing across the forex majors with the dollar performing well. Notable exceptions are the yen which is holding up well amidst the renew threat to geopolitical stability posed from North Korea, and sterling. In commodities, the renewed dollar strength has dragged gold back below $1300 again, with oil just slipping slightly after another good session yesterday.

Inflation is key for European traders today with both the UK and Eurozone announcing their CPI for September. UK CPI is released at 0930BST and is expected to tick higher to 3.0% on a headline basis which would be the highest since 2012 and also prompt a letter to be written by Governor Carney to Chancellor Hammond. Core CPI is expected to remain at +2.7%, however if either of these numbers see an upside surprise the pressure would grow further on the Bank of England for a rate hike. Also watch for an expected rise in the PPI Input Prices to 8.2% (from 7.6%) which would again reflect the issue of increased prices into the factory gate from the decline in the value of sterling. Eurozone final CPI for September is at 1100BST and is expected to confirm the flash readings of +1.5% for the headline CPI (in line with last month) and +1.1% for the core CPI which would be a drop back from +1.3% last month. German ZEW Economic Sentiment is at 1000BST and is expected to improve to +20.0 from +17.0 and would be the highest reading since May and would be euro supportive. US Industrial Production is at 1415BST and is expected to be +0.3% for the month of September (having dropped -0.9% last month). The Capacity Utilization is expected to improve marginally to 76.2% from 76.1%.

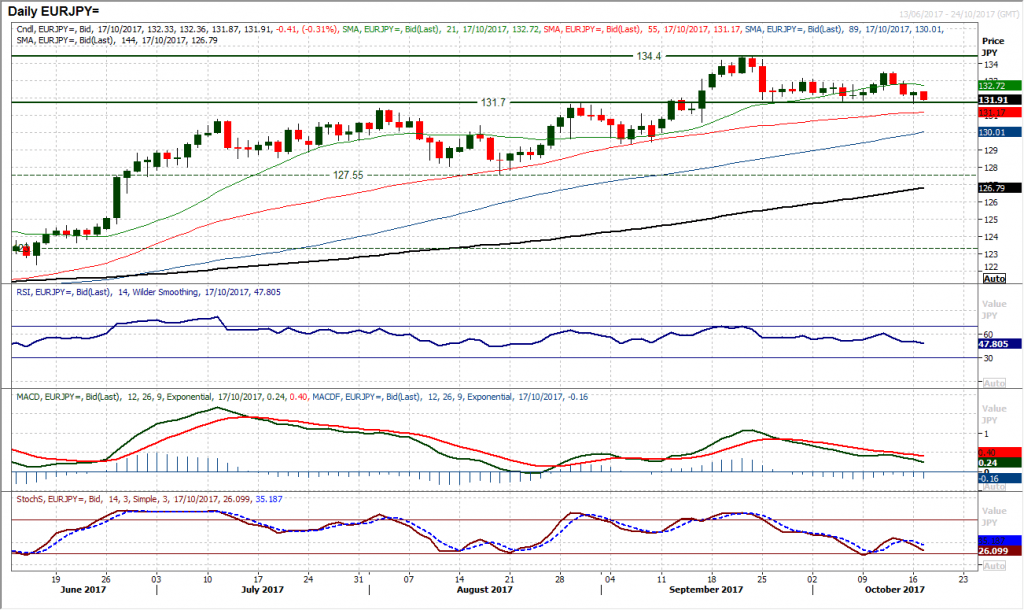

Chart of the Day – EUR/JPY

The euro is coming under pressure as the Euro/Yen pair has dropped back to again put pressure on the key breakout support at 131.70. This has implications for a general reduction in risk appetite but a close below 131.70 would complete a top pattern and imply 180 pips of downside in the coming weeks. The momentum indicators are reflective of this pressure for a breakdown with the RSI below 50 for the first time since mid-September, the MACD lines turning back lower in a correction along with a negative cross on the Stochastics. The completion of a break would open a move would be back towards 130.00 whilst the old September lows at 129.35 could come under pressure if the bearish momentum really took hold near term. The hourly chart show negative configuration and a series of lower highs/lower lows in the past few sessions. There is initial resistance around 132.00 which is a near term pivot and then yesterday’s high at 132.35.

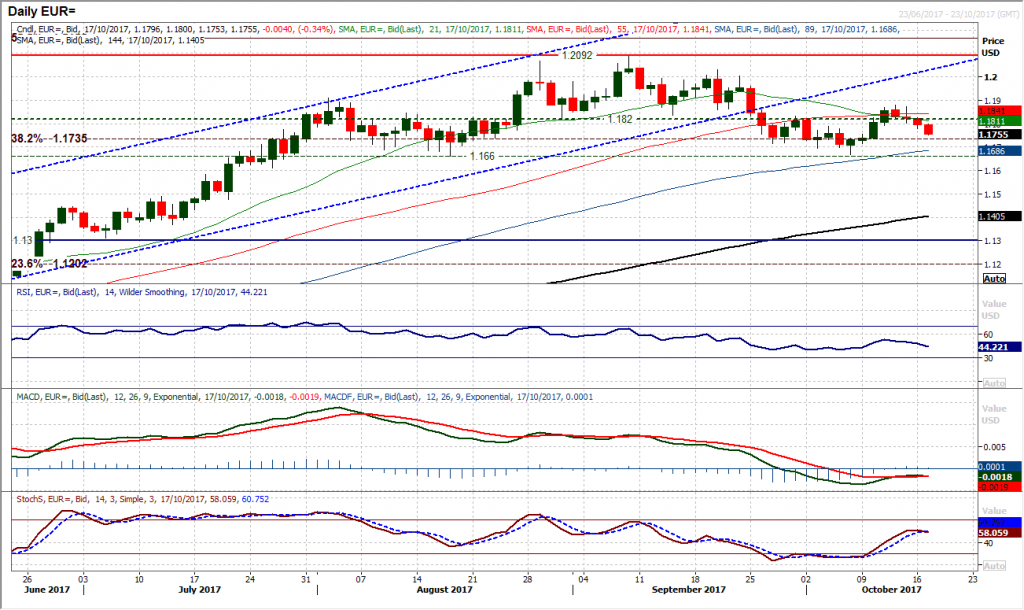

EUR/USD

Gradually over the past couple of sessions there seems to have been a change in outlook as the dollar has begun to strengthen once more. Coming as the euro has also been weakening this has dragged EUR/USD back below $1.1820 again and which seems to have ended the minor recovery that had come over the early part of last week. This is still a chart with very benign moves but the next real support is now until the low at $1.1667 (just above the key August low of $1.1660). Suddenly we see intraday rallies being sold into, something shown well on the hourly chart with the negative near term configuration of the hourly momentum with the hourly RSI failing around 50. The old neckline has also become a basis of resistance once more around $1.1820. Resistance at $1.1880 is growing in importance. There is a minor pivot at $1.1760 and then support at $1.1715 to watch.

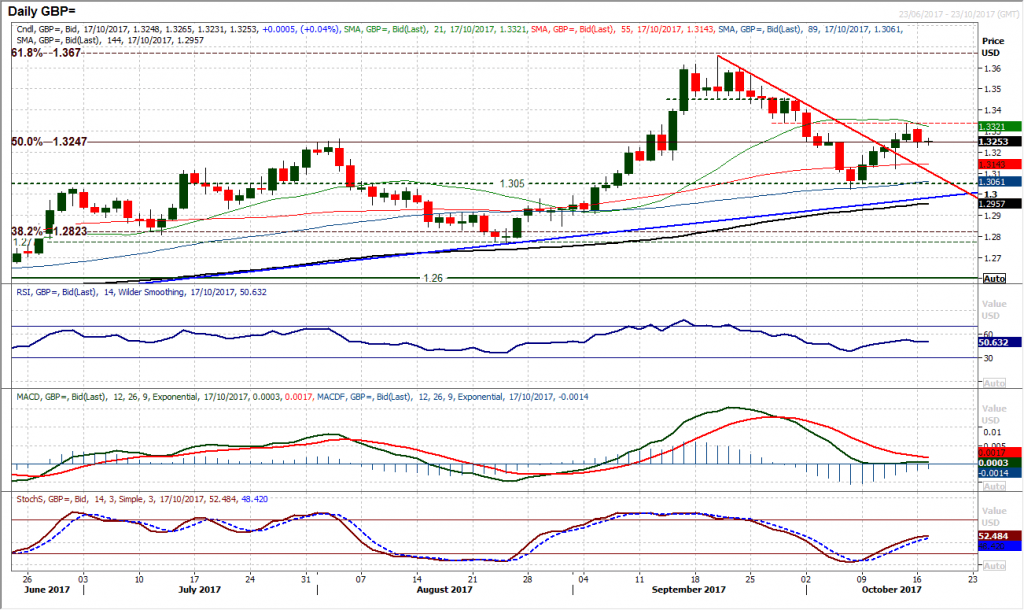

GBP/USD

With the rally stalling around the resistance at $1.3340 on Friday and yesterday’s subsequent bearish one day candlestick, the recovery on Cable is being questioned. This is the first time in six sessions we see a negative session and it will be interesting to see how the buyers react today. The move has dragged the market back to the band of support around the 50% Fibonacci retracement of the Brexit sell-off at $1.3247, whilst the old August high is $1.3265. With momentum indicators almost entirely neutrally configured (RSI and Stochastics around 50, MACD lines flattening around neutral), the next move could be key. With the hourly chart technical indicators also settling around neutral, the market seems to be set up today for UK inflation which is a key risk event for Cable. Another bear candle with a decisive negative close (likely on a weak inflation read) will begin to see downside traction developing and re-open $1.3120 again.

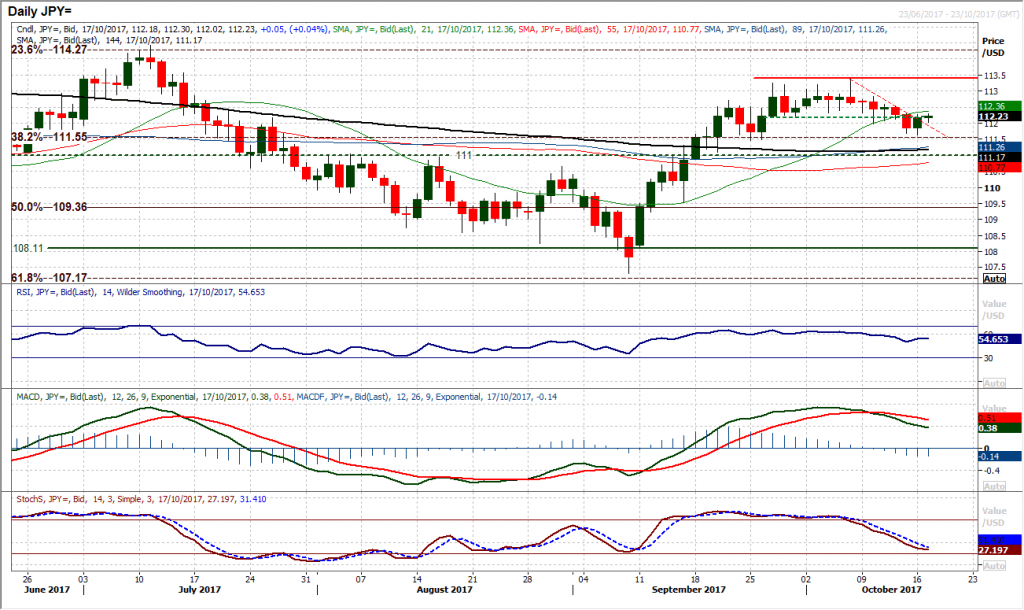

USD/JPY

A dollar recovery shows that the bulls are looking to fight back, but there is technical resistance overhead that needs to be overcome before a sustainable turnaround can be confirmed. The old support at 112.20 has become a basis of resistance in the past few sessions and needs to be decisively cleared for the bulls to feel happier again. The rebound has broken the little seven day downtrend but the move has yet to confirm anything. There has been a broad deterioration in momentum which is still a factor, and the hourly chart shows a series of overhead resistance levels between 112.20/112.60 which are a barrier to recovery. Despite this though there has been an improvement in near term momentum with the hourly RSI and MACD lines move positively configured than at any time for over a week. Support is now initially at 111.65 above 111.45. A close back above 112.20 would help to build on the improving picture today but for now rallies into the resistance are favoured as a chance to sell.

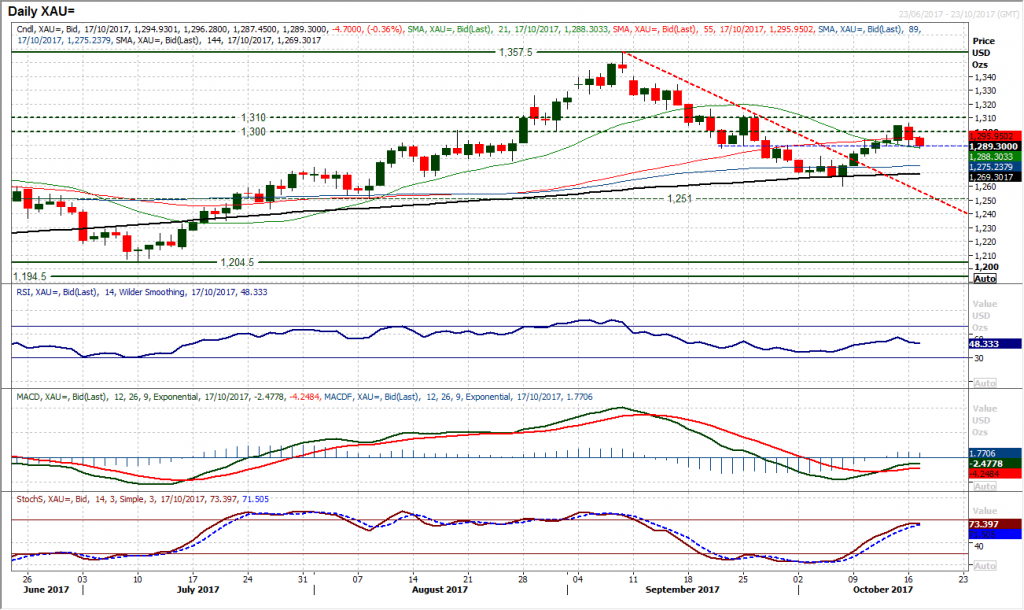

Gold

The long term pivot band is $1300/$1310 and so with the market peaking at $1306 yesterday before dropping away there will be concerns for the bulls that this barrier has once more provided a key turning point. Yesterday’s negative candle was the first such candle in six sessions and is being followed by an early dip again today. With momentum indicators now beginning to roll over again the market is turning increasingly corrective. The hourly chart shows how a key near term support around $1290 is being tested and a breach would complete a breakdown. The run of higher lows would have been broken and put pressure on the next support at $1284. The hourly MACD lines have already made the breakdown, whilst the hourly RSI is now back at a level where the bulls need to respond this morning to prevent the outlook turning decisively corrective again. The concern is that $1300 now becomes a basis of resistance again with an initial $1296 forming a barrier overnight. The bulls seem to be close to losing control of this one again.

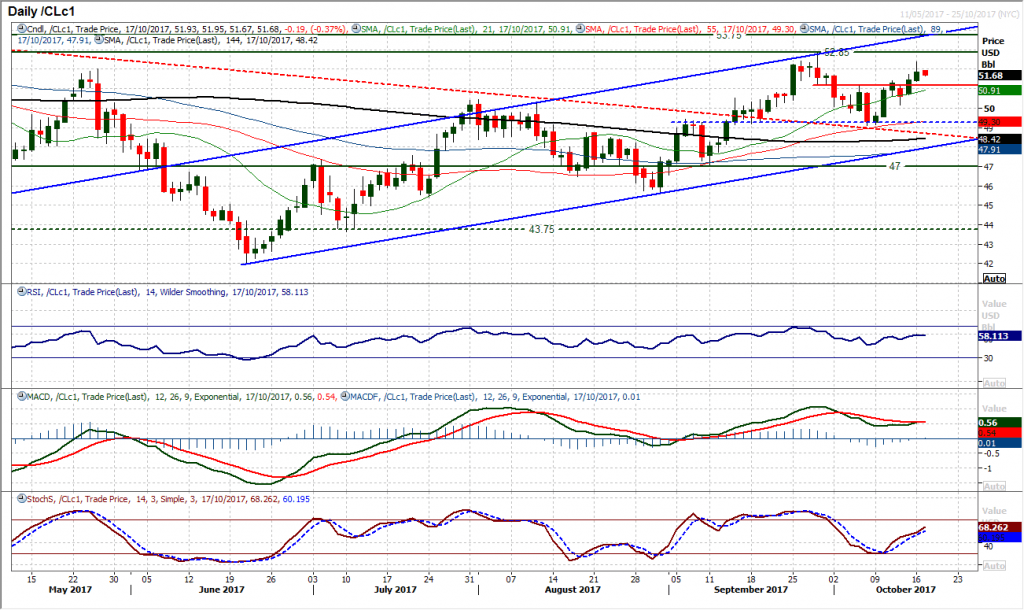

WTI Oil

The bulls have bounced back strongly in the past couple of sessions and are now in control of a run that looks set to push back higher towards the key September high at $52.85. The momentum indicators are confirming the improvement as the RSI tracks higher towards 60, Stochastics rise above neutral and MACD lines are on the brink of a bull cross above neutral. The hourly chart shows positive configuration with corrections being bought into. There is now a near term band of support $51.20/$51.40, whilst yesterday’s intraday high at $52.35 is initial resistance.

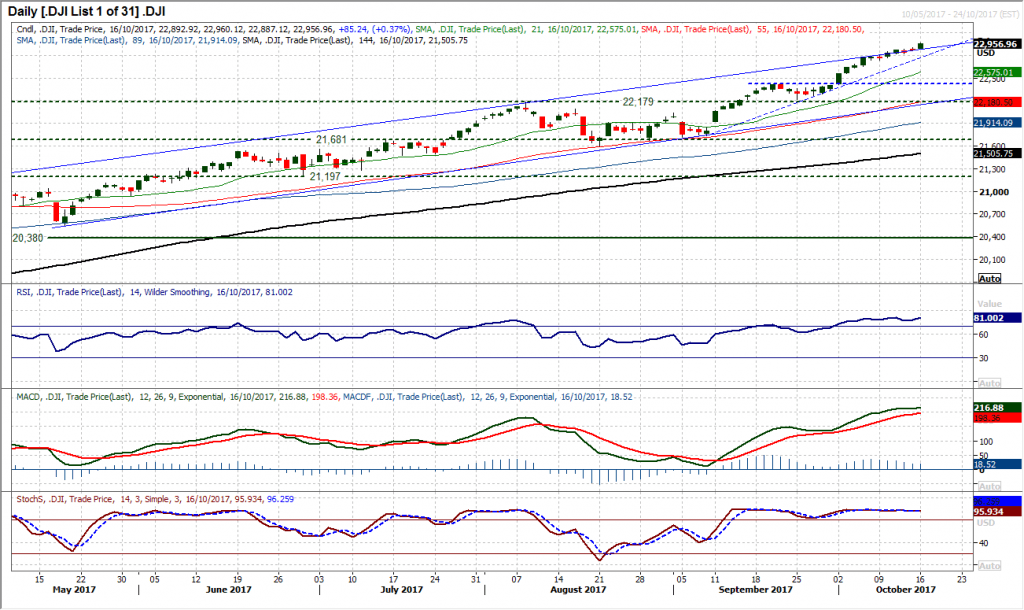

Dow Jones Industrial Average

The candles continue to grind higher as the market pushes ever further into new all-time highs. There is a drifting sense of bullishness that continues to leave a strong of higher daily traded lows and maintains the sense of positive momentum. Daily RSI, Stochastics and MACD lines may not be storming higher now, however remain positively configured and mean that backing the rally remains a decent strategy. The next 1000 tick barrier is coming ever closer now with 23,000 just under 50 ticks from yesterday’s intraday all time high of 22,960. Even though the Average True Range has fallen back over the past month from around 140 ticks, the current 84 tick ATR means that a test of 23,000 should be seen today. If last Thursday’s low at 22,281 is taken as the same tick low as Wednesday, then a run of higher lows is now into its 13th completed session, making initial support at 22,887.

Author

Richard Perry

Independent Analyst