Deer in the headlights

S&P 500 is slowly getting under pressure, which is likely to culminate on weak non-farm payrolls tomorrow if Wednesday was any guide. Credit markets are pushing for higher yields as inflation data keep surprising those policymakers who had been already surprised throughout 2021. Commodities though aren‘t freezing as a proverbial deer in the headlights, and once the scare of the Fed‘s short tightening cycle gets done away with, precious metals would join. In the meantime, look for silver to act on copper‘s cue, and for gold to do relatively better in risk-off settings.

As for stocks, my gentle selling bias while on the lookout to enter short towards the session‘s end, hasn‘t changed since yesterday, and the new position is already profitable:

(…) the low volume behind the upswing coupled with credit market reversal shows that the push towards 4,600 is next – but it would be fraught with internal vulnerability. It‘s that value has welcomed the risk-on turn while tech barely prevented lower values – the bond reprieve won‘t last, and is providing more fuel behind the commodities push higher, and precious metals recovery.

The Kashkari effect and good ISM Manufacturing PMIs have worked fine, but the services data awaits. And I‘m looking at it to throw a spanner in the works, a modest one. For now, controlling the overall risk is key – fresh portfolio highs were achieved yesterday as new S&P 500 long profits were taken off the table – and commodities with precious metals are likely to do well in this extended (sticking out like a sore thumb) rally off oversold levels (in tech). The other key thought expressed in the linked tweet is that S&P 500 hasn‘t entered a bear market, that it hasn‘t rolled over to the downside for good. It‘s that I expect the return of the bears in the not too distant future, and a smoother sailing in 2H 2022.

Let‘s move right into the charts.

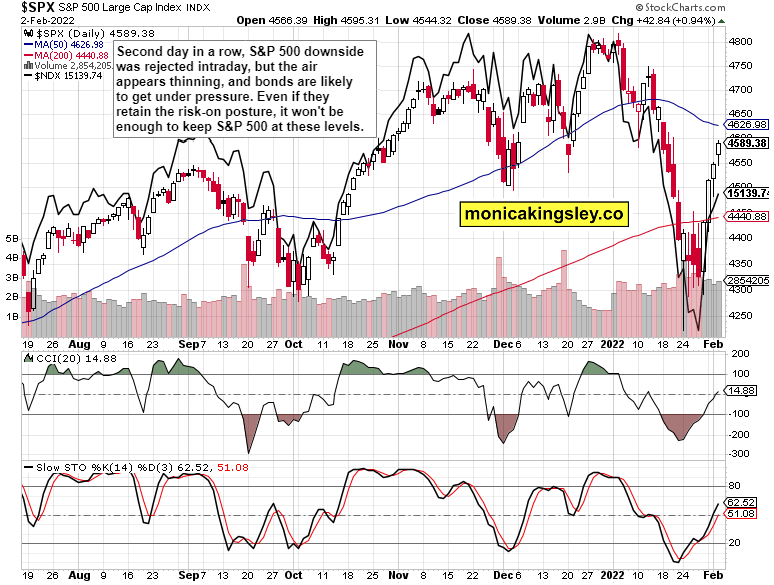

S&P 500 and Nasdaq outlook

S&P 500 bulls prevailed yesterday, but would get under pressure relatively soon. The ominous lower knots say a consolidation is knocking on the door.

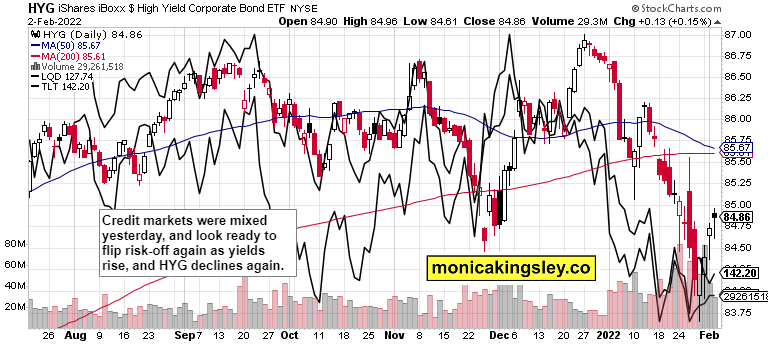

Credit markets

HYG repelled selling pressure, but that won‘t last – I‘m looking for lower values across the bond spectrum, coinciding with (temporary) dollar upswing. Risk-off.

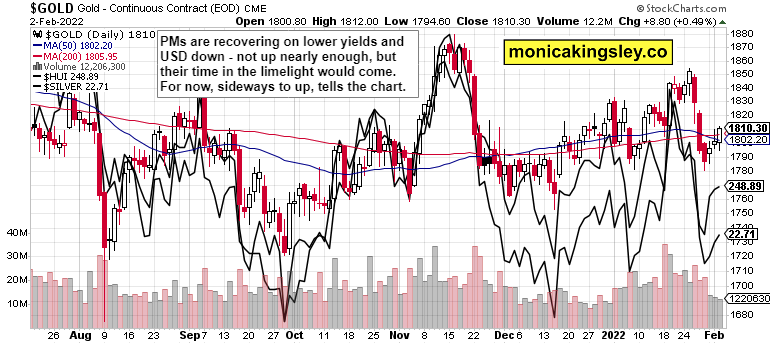

Gold, silver and miners

All this risk-off already in and still to come, is failing to press gold and silver really down – and that tells you the true direction is up, just waiting for a (Fed, inflation, stagflation) catalyst.

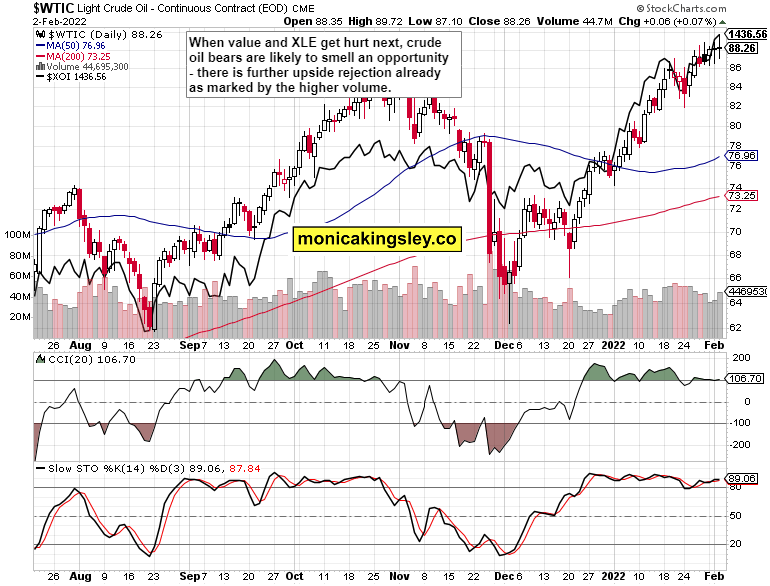

Crude oil

Crude oil bulls aren‘t yet wavering, but remain perched pretty high – I‘m looking for sideways to down consolidation as the bears get emboldened by the rising volume. Trying their luck soon.

Copper

Copper is back to the middle of its recent range, still positioned for an upside breakout. Commodities are pointing in the right direction – note the absence of sellers yesterday. How far would the USD upswing compress the red metal today? Not much, not lastingly.

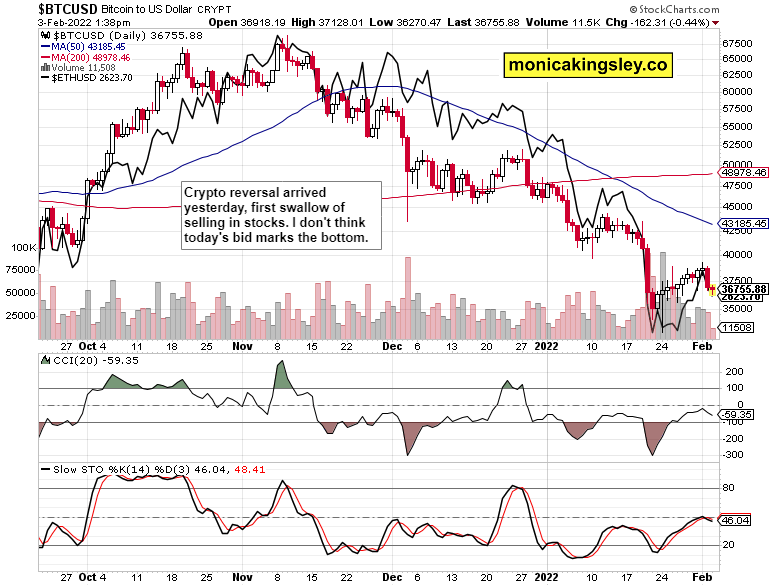

Bitcoin and Ethereum

The narrow crypto trading range is over, and the bears are on the move – look for them to take some time before they get going towards BTC $35K.

Summary

S&P 500 bulls are about to meet the bears again, and higher yields won‘t save value stocks, let alone spawn a rush to tech safety. The pressure in stocks to probe lower values, is building up, and 4,450 may not be enough to stop it. For all the pause in Fed hawkish jawboning, the tightening cycle is merely getting started, and stocks will feel it. Unlike precious metals, which would reverse prior hesitation once the rate raising starts in earnest, and start going up. And commodities? These aren‘t waiting for anyone‘s greenlight. And neither should you in life – what I would like to bring to your attention, is that volatility is rising, and it thus makes sense to pare back the overall portfolio exposure and position sizing while taking only the strongest of opportunities.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.